The American hospitality market is on fire right now. But the heat is moving away from crowded cities. Investors are looking at quiet towns and rural gems. Big cities face high costs and low growth. Rural areas offer a fresh start. Travelers want new experiences. They want boutique stays and local charm. This shift creates a massive chance for you to grow. If you want to build or buy in these areas, you need the right money. That is where USDA hotel financing comes in.

This program is the secret weapon for savvy investors in 2026. It offers terms that banks usually keep for their best clients. It helps you build when others say no. At HotelLoans.Net, we have 30 years of underwriting experience. We know how to navigate these government rules. We offer 75 different loan options. But for rural projects, this one stands out. It can turn a small dream into a 4-star reality.

You might think the USDA only helps farmers. That is a mistake. The USDA Business and Industry (B&I) program helps many types of businesses. It helps motels, hotels, and bed-and-breakfasts. So, what exactly is USDA Rural Development hotel financing?

It is a government guarantee. A private bank gives you the loan. Then, the USDA promises to pay back a big part of it if you fail. Because of this promise, the bank feels safe. They give you lower rates and longer terms. In 2026, the USDA increased the guarantee to 85% for loans under $5 million. This is a huge win for smaller projects. It means you can get better deals even if you are starting.

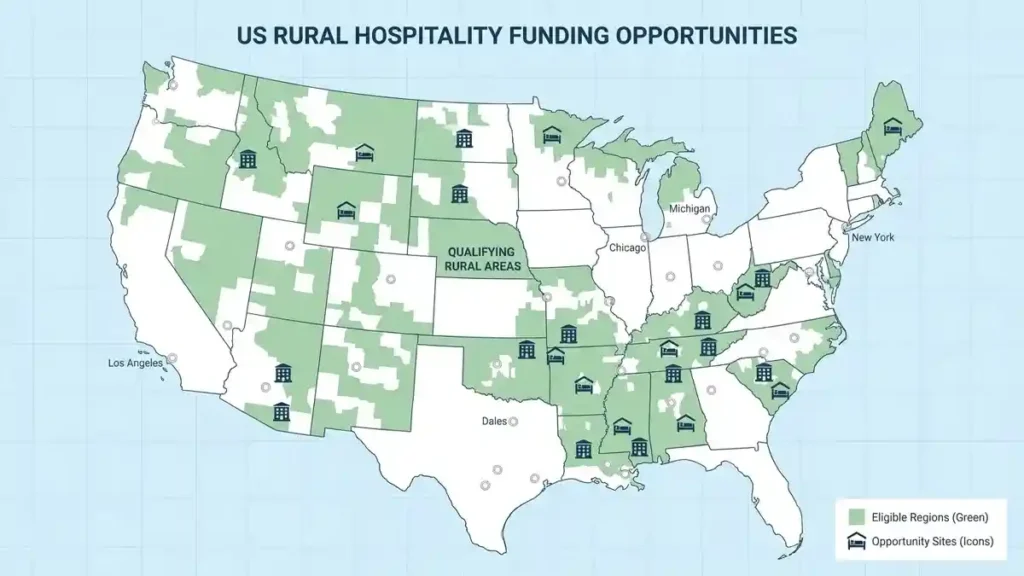

This program works in 97% of the United States. You need to be in an area with fewer than 50,000 people. This covers more land than you might think. It is not just about farms. It includes beach towns, mountain resorts, and historic stops along the highway.

Feature

2026 USDA B&I Detail

Max Loan Amount

$25 million (up to $40M with approval)

Repayment Term

Up to 30 years for real estate

Guarantee % (<$5M)

85%

Population Limit

Under 50,000 people

Equity Required

10% for existing / 20% for startups

Is USDA Hotel Financing the Best Choice for You?

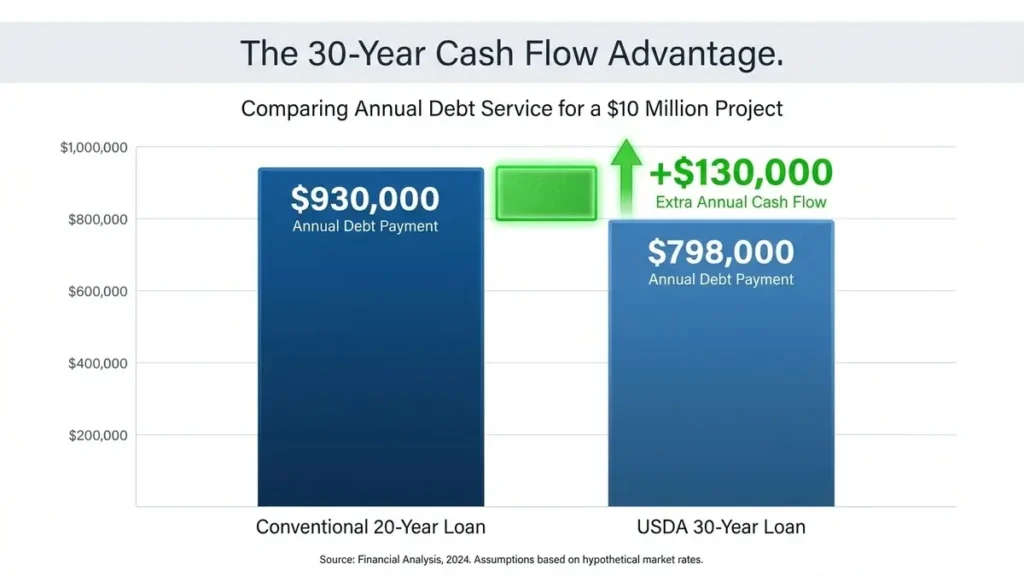

Choosing the right debt is vital. You want to keep your cash flow healthy. Traditional bank loans often have short terms. They make you pay it back in 15 or 20 years. They also have “balloon payments.” This means you must pay a huge chunk all at once at the end. That is a big risk.

The Advantages of USDA hotel development loans are clear. You get a 30-year term. There are no balloon payments. This lowers your monthly bill. You keep more cash in your pocket every month. You can use that cash to hire better staff or fix up your rooms. Also, these loans usually have no prepayment penalties. You can sell the property or refinance if rates drop later.

USDA loan for rural hotel purchase

Buying an existing property is a smart move. Many older hotels need a new vision. You can use a USDA loan to purchase a rural hotel, including the building and land. You can even include the cost of repairs in the loan. This is perfect for “fix and rent” or “fix and hold” strategies.

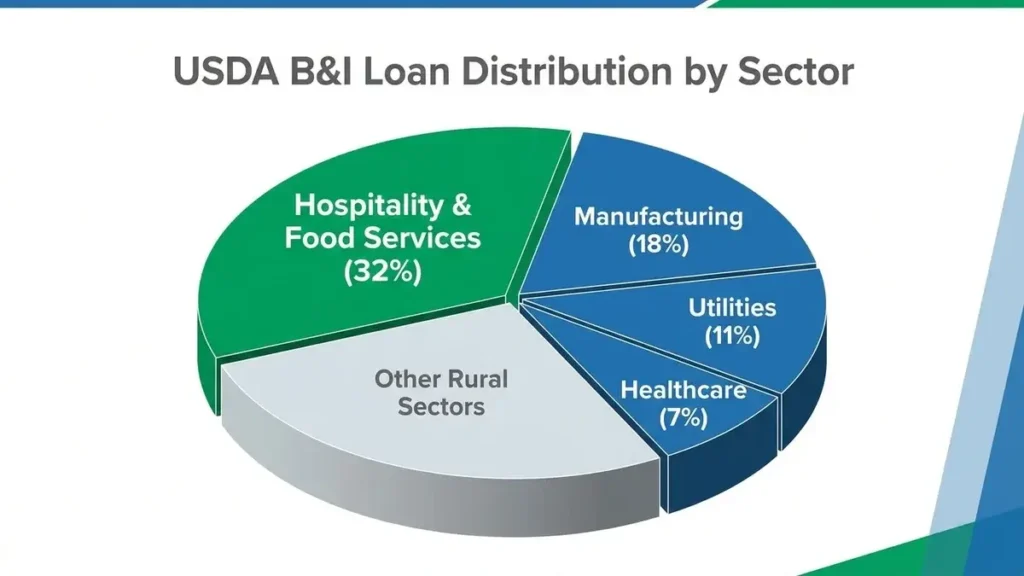

The USDA wants to see you save jobs. If you buy a struggling hotel and keep the staff, you score high points. In 2024, the hospitality sector got over 32% of all B&I funds. That is over $570 million. Investors are using this to grab assets in secondary markets before the big players arrive.

USDA guaranteed loans for motel construction

Building from the ground up is hard. Material and labor costs are rising. But USDA guaranteed loans for motel construction offer a special feature. It is called “construction-to-permanent” financing. You get one loan that covers the build and the long-term debt. You don’t have to go through the stress of a second closing once the motel opens.

This is a game-changer. It protects you from rising rates during the build. You also get interest-only payments for up to 36 months while you build and open. This gives you a “ramp-up” period. It lets you focus on getting guests in the door without worrying about full debt payments on day one.

Eligibility for USDA B&B financing

The program is very flexible. It is not just for big flags like Marriott or Hilton. There is clear eligibility for USDA B&B financing, too. Boutique stays and small inns are very popular now. Many travelers want a local feel. They want to stay in a historic home or a cozy lodge.

If your B&B is in a rural zone, you can qualify. You need to show that it will be a real business. It cannot just be a hobby. You need a business plan and a market study. This proves people will actually stay there. At HotelLoans.Net, we help you put these papers together. We make sure the USDA sees the value in your small stay.

How to qualify for USDA hotel loan in 2026?

The rules are strict but fair. You need to follow them exactly. If you miss one step, they will say no. So, how to qualify for USDA hotel loan applications? You need several key things ready.

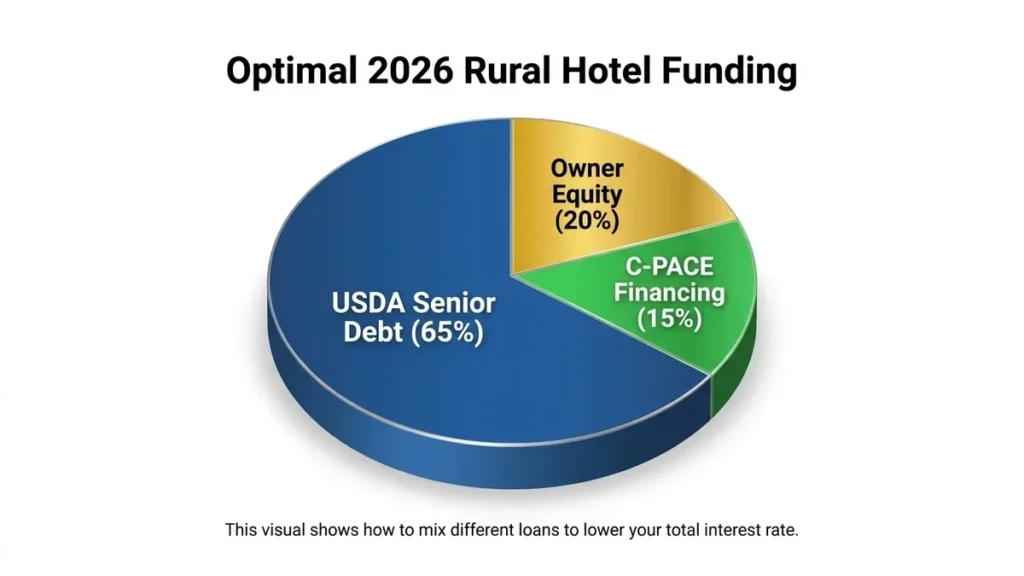

First, check the map. Your property must be in a rural area. You can find this on the USDA website. Then, look at your equity. For a new business, you need 20% of your own money in the deal. If you already own the business and want to grow, you might only need 10%. This must be real money or land value. You cannot use “sweat equity.”

You also need to show a “priority score.” The USDA gives points for different things. They like projects that create jobs. They like projects in poor counties. They also like “green” buildings that save energy. In 2026, you generally need a score of 20 points to get a guarantee.

USDA financing requirements for boutique hotels

Boutique hotels have special needs. They often cost more to design. They need high-end furniture and fixtures. The USDA financing requirements for boutique hotels allow you to include these costs. You can finance the “FF&E” (Furniture, Fixtures, and Equipment) as part of the total project.

You will need a feasibility study. This is a report by an expert. It shows that your boutique hotel can charge high rates. It shows that guests want to stay in that specific town. The USDA wants to know that your project is “viable”. They want to see that you will make enough money to pay the loan and stay in business for a long time.

Steps to apply for a USDA hotel loan

Don’t let the paperwork scare you. It takes time, but it is worth it. Here are the steps to apply for a USDA hotel loan:

Check the location: Use the USDA map to confirm your town qualifies.

Find a lender: You need a bank that knows the USDA program. Not all banks do.

Get a pre-check: Have a specialist like HotelLoans.Net look at your numbers.

Order reports: You need an appraisal and a feasibility study.

Submit the file: The lender sends the pack to the local USDA office.

Wait for the promise: the USDA will issue a “Conditional Commitment.”

This process can take 3 to 6 months. It is slower than a conventional loan. But the lower payments save you thousands of dollars every year.

USDA hotel loan approval process

The USDA hotel loan approval process has two layers. First, your bank underwrites the loan. They look at your credit and your experience. Then, they send it to the USDA state office. A government official reviews it. They check if it meets the job goals and rural rules.

If you are a seasoned hotelier, it is easier. They like to see that you have run hotels before. But new investors can win too. You need a strong team. You might need a professional management company to help you handle day-to-day operations.

Comparing the Options: USDA vs. SBA

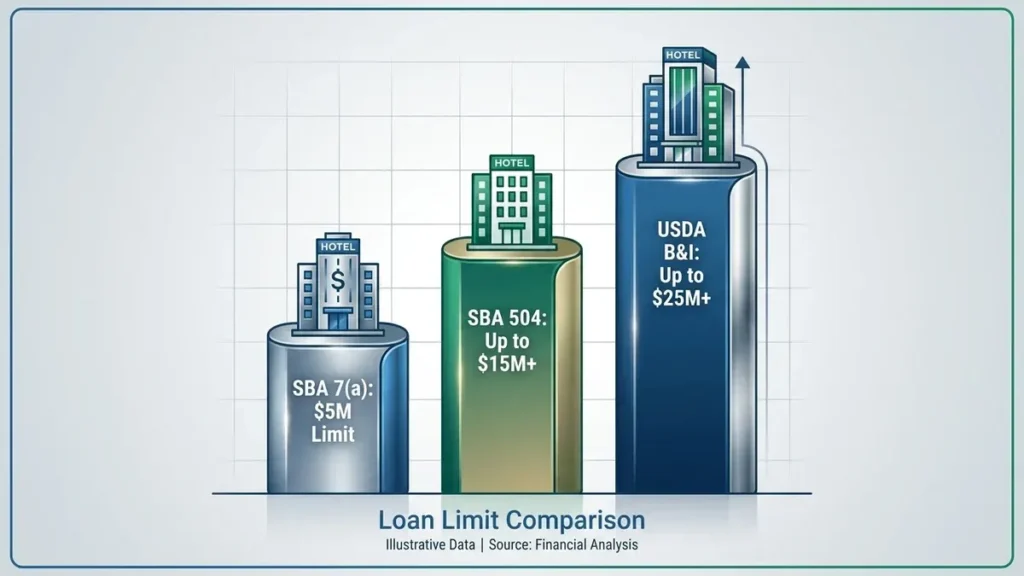

You might have heard of SBA loans. They are the most common small business loans. But rural hotels have limits. When you compare USDA vs SBA hotel loans, you see a big difference in size.

The SBA 7(a) loan is capped at $5 million. That is not enough for most modern hotels. Building a new 80-room hotel costs much more than that. The SBA 504 can go higher, maybe up to $15 million or $20 million. But it is very rigid. You cannot use it for working capital or marketing.

The USDA B&I program is capped at $25 million. It also allows you to include working capital. This is the money you need to pay bills while you wait for guests to arrive. If you have a large project in a small town, the USDA is usually the winner.

Loan Feature

USDA B&I

SBA 7(a)

SBA 504

Max Loan Size

$25 Million

$5 Million

$15 Million+

Max Term

30 Years

25 Years

25 Years

Population Limit

Under 50,000

None

None

Working Capital

Allowed

Allowed

Not Allowed

Interest Rate

Negotiated (Market)

Variable (Prime+)

Fixed Portion

What are the Interest rates on USDA hotel financing?

Everyone wants the lowest rate. In May 2026, rates are still a top concern. But remember, the rate is only half the story. The 30-year term is what really helps your cash flow.

The government does not set interest rates on USDA hotel financing. You negotiate them with your lender. They can be fixed or variable. Most lenders charge “WSJ Prime + 1% to 3%”. As of May 2026, the average rate for a USDA purchase is around 5.70%.

May 2026 Rate Type

Average Rate

APR

USDA Purchase (30-Yr Fixed)

5.70%

5.85%

USDA Refinance (30-Yr Fixed)

5.64%

5.79%

Direct Ownership (FSA)

5.75%

N/A

These rates are much better than “hard money” or bridge loans. Bridge loans often start at 10% or higher. If you use a bridge loan to build, you should look for a USDA “take-out” loan as soon as you open the loan.

Expanding and Refinancing Your Portfolio

The USDA program is not just for one project. You can grow a whole brand this way. Some investors have over $100 million in USDA debt. They just set up each hotel in a separate LLC and on a separate piece of land.

USDA hotel refinance options

Maybe you already own a hotel. Perhaps you have a high-interest loan that is about to expire. You can use USDA hotel refinance options to get a better deal. To do this, you must show a “substantial benefit.” This usually means your monthly payment drops by at least 10%.

You can also refinance to save jobs. If your current debt is so high that you might have to close, the USDA can step in. They can give you a 30-year term to lower your costs. This keeps the hotel open and keeps people working in the town.

USDA loan programs for existing hotels

Existing owners can also use the program to expand. You can use USDA loan programs for existing hotels to add a new wing or a pool. You can even buy the lot next door and build a restaurant.

If your brand requires a “Property Improvement Plan” (PIP), the USDA can help. These renovations are expensive. But they increase your value. You can bundle the cost of these repairs into a new USDA loan. This lets you modernize without draining all your savings.

USDA loan limits for hotel properties

The standard USDA loan limits for hotel properties are $25 million per project. This is a lot of money for a rural area. It can build a very nice select-service hotel. If your project is even bigger, like a massive resort, you can ask for more. With special approval, the limit can be raised to $40 million.

This limit applies to the “guaranteed” portion. Since the bank is lending the money, the total project cost can be even higher. You have to bring more equity to the table. This makes the USDA program perfect for mid-market developers who have outgrown SBA loans.

Why HotelLoans.Net is Your Best Partner?

Navigating the government can be a headache. You need an expert who has been there before. HotelLoans.Net is a “correspondent and table lender.” This means we are not just middlemen. We have 30 years of underwriting experience. We know what the USDA wants to see.

We have a vast network of private lenders and investors. We offer 75 different loan options. If the USDA is not a fit, we have bridge loans, DSCR loans, and SBA options. We provide the financial advice you need to win. We don’t run your hotel, but we make sure you have the money to build it.

We also have a great referral program. If you are a real estate broker, we want to work with you. We help your clients get the cash they need to close the deal. Whether you are new to the industry or a veteran, our team is here to support you.

The Final Verdict on USDA Hotel Financing

The world is changing. Rural America is the new frontier for hospitality. The competition is lower, and the potential is higher. But you cannot win without the right capital.

USDA hotel financing is the most stable debt in the market. It offers the longest terms and the best cash flow protection. It lets you build boutique dreams and renovate historic motels. It gives you the power to compete with the big guys in the city.

Don’t let high rates stop your next project. Think about the 30-year play. Think about the job creation in a town that needs it. If you have a project in mind, let’s talk. Check your location on the map today. Then, call the experts at HotelLoans.Net. We will help you turn your vision into a reality. Let’s build something great together.

FAQs

Can I use funds for golf courses?

No. The USDA specifically bans using these loan funds for golf courses or their infrastructure. You also cannot use the money for gambling facilities or racetracks. Focus your project on lodging or dining services to stay eligible.

Are environmental studies required for approval?

Yes. Every project must pass a federal environmental review before it gets final approval. This check ensures your build does not harm local nature or historic sites. You will likely need a Phase I report to proceed.

Does USDA offer revolving lines of credit?

No. This program provides term loans only for specific project costs, such as buying land or equipment. It does not support revolving credit lines. If you need short-term cash, look at other private lending programs for help.

Is a secondary market available for lenders?

Yes. Lenders can sell the guaranteed portion of your loan on the secondary market. This helps banks manage their risk and keep lending to other rural businesses. You continue working with your original lender for all monthly services.

Can a management company run my hotel?

Yes. You can hire a professional firm to manage your property operations. The USDA often likes this for new investors. It shows that experts handle the day-to-day work, which lowers the risk to your loan.

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Facebook Twitter Pinterest LinkedIn Your hotel project is stuck. You have a half-finished building and a lender who stopped calling you back. This is the

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.