The clock is ticking for commercial real estate owners, especially those in the hospitality sector, as they face the formidable wall of CMBS loan maturities. According to the U.S. Federal Reserve, the outstanding amount of commercial mortgage-backed securities (CMBS) debt is significant, and a substantial portion is scheduled to mature in the next two years.

The Big Question: Is your hotel’s CMBS debt maturity date approaching, leaving you scrambling for options to refinance maturing CMBS debt in this volatile interest rate environment? The typical outcome a painful sale or even default is a scenario you can and should avoid.

This isn’t just a market problem; it’s a direct threat to your equity and the legacy you’ve built. The confluence of rising rates and tighter conventional lending standards means that traditional refinancing is often impossible or financially devastating.

The Strategic Solution: Private Bridge Loan for Maturing CMBS Debt

A private bridge loan for maturing CMBS debt is not just an option it’s a strategic, flexible lifeline designed for this exact scenario. It acts as a temporary, capital-injected buffer that immediately stops the maturity clock and gives you the crucial time needed to stabilize operations, execute property improvements, and position the asset for a successful, long-term exit or permanent refinancing when market conditions improve.

At HotelLoans.Net, we serve as both a correspondent and table lender, specializing in hospitality real estate finance. Our deep industry knowledge and 30 years of underwriting experience enable us to rapidly structure and deploy the capital you need to navigate this critical transition.

The CMBS Maturity Cliff: Why Traditional Refinancing Fails for Hotel Owners

Hotel owners today are staring down a CMBS maturity cliff a perfect storm in which large, non-amortizing balloon payments are due in a highly unfavorable lending environment. For example, according to the Mortgage Bankers Association (MBA), hotel/motel loans account for a significant portion of the total commercial mortgages scheduled to mature, underscoring the acute risk for the hospitality sector.

The problem centers on the balloon payment, a feature of most CMBS loans. These loans were often structured with a long-term amortization schedule but a much shorter five-, seven-, or ten-year term. The borrower pays only a fraction of the principal (or no principal during initial interest-only periods) until the final maturity date, when the entire outstanding principal the balloon is due.

The Refinancing Headache

Understanding CMBS Special Servicing and Its Impact

When a borrower faces an imminent CMBS loan maturity they can’t meet, the loan is often transferred from the Master Servicer to a Special Servicer. This is a red flag for any potential new lender.

Adversarial Relationship: The Special Servicer’s primary role is to maximize recovery for the bondholders, not necessarily to work in the borrower’s best interest. This creates an inherently adversarial environment.

Time and Cost: Engaging with a Special Servicer negotiating a loan modification, extension, or workout is notoriously slow, costly, and unpredictable. This delay is fatal for a traditional refinance, as permanent lenders demand a clean, timely payoff.

Increased Risk: A loan in special servicing presents an elevated risk profile, making it nearly impossible to secure new, low-cost capital from conventional sources.

DSCR and LTV: The New Hurdles

The current economic landscape has erected two significant financial barriers to traditional refinancing:

Debt-Service Coverage Ratio (DSCR): This ratio compares your property’s Net Operating Income (NOI) to its debt service payments. Permanent lenders typically require a DSCR of 1.25x or higher.

DSCR = Net Operating Income / Total Debt Service

With rising interest rates, the debt service payment required for a new loan has increased dramatically. Simultaneously, post-pandemic challenges and rising operating expenses (labor, insurance, utilities) have often reduced the hotel’s NOI. The result is a depressed DSCR that falls short of the new lender’s underwriting threshold.

Loan-to-Value (LTV): This ratio compares the new loan amount to the property’s current appraised value.

Tighter credit standards and property valuation issues especially if the property has underperformed or requires significant capital expenditure mean the permanent lender’s required LTV (often 65% or less) will not cover the full amount needed to pay off the existing balloon plus closing costs.

This gap, created by a low DSCR and LTV, is why traditional banks and CMBS lenders are unable to provide the full financing necessary, pushing the owner toward default or a distressed sale.

The Private Bridge Loan for Maturing CMBS Debt Solution

Private bridge financing for CMBS loan maturity is the necessary tool to circumvent this crisis. This loan is a short-term (12-36 months), higher-leverage, and faster-closing solution specifically designed to stop the maturity clock and provide the borrower with capital to execute a value-add strategy.

It allows you to:

Pay Off the CMBS Balloon: Immediately extinguishing the high-stakes threat of a maturity default and removing the loan from special servicing.

Execute a Stabilizing Plan: Fund necessary Property Improvement Plans (PIPs) or strategic operational shifts to increase the hotel’s Net Operating Income (NOI).

Boost Valuation and DSCR: By increasing NOI and waiting for potential interest rate stabilization, the property’s financial metrics (DSCR and LTV) improve, ultimately positioning the asset for a successful and less costly permanent refinancing when the bridge term expires.

Choosing to navigate maturing CMBS without bridge financing significantly increases the risks, including the risk of foreclosure and equity loss. A CMBS loan default private bridge loan solution is the fastest path to stability and long-term financial health.

Securing Your Future: What is a Private Bridge Loan for Maturing CMBS Debt?

The private bridge loan for maturing CMBS debt is more than just a financing tool; it is a specialized instrument of capital preservation and value creation, specifically tailored to counter the immediate threat posed by a CMBS maturity default.

This urgency is underscored by the current market distress. For instance, CMBS loans totaling $2.3 billion were newly added to the distress rate in March 2025, with 53.4% of that volume comprising imminent or actual maturity default, according to KBRA data. This highlights the prevalence of CMBS maturity default risk for commercial real estate owners, particularly in sectors such as lodging.

Defining the Private Edge: Speed, Flexibility, and Certainty

A private bridge loan for CMBS maturity is a short-term (typically 6 to 36 months), high-leverage financing option provided by private capital (non-bank specialty funds, debt funds, and family offices), rather than traditional deposit-holding banks. This distinction gives it the unique characteristics needed to solve the CMBS crisis:

The Need for Speed

In a CMBS maturity scenario, time is the single most critical factor. Once the maturity date passes, the loan is transferred to the Special Servicer, triggering a costly, equity-eroding process.

Quick Close Private Bridge Loan CMBS: Private lenders operate outside the bureaucratic constraints of conventional banks, allowing them to underwrite and close deals in a matter of weeks, not months. This speed is essential for meeting the tight CMBS maturity deadline, enabling the borrower to pay off the balloon principal and avoid default.

Customization and Flexibility

Conventional lenders are restricted by rigid underwriting criteria (DSCR, LTV, and credit history). Private lenders, however, focus intensely on the asset’s true potential and the borrower’s credible exit strategy.

Asset-Focused Underwriting: If your hotel’s Net Operating Income (NOI) is temporarily depressed due to rising expenses or necessary renovations, a private bridge lender can often look past this short-term dip. They underwrite based on the property’s “stabilized value” the estimated value after the borrower executes their improvement plan.

Business Plan Support: This financing is ideally suited for “fix and flip” or “fix and hold” strategies in hospitality, providing the immediate capital required to stabilize the property and execute the business plan that conventional banks wouldn’t fund.

The Strategic Use Case: Bridge to Value Maximization

The actual value of a private bridge loan for maturing CMBS debt lies in its ability to buy time for strategic execution, thereby maximizing the asset’s financial metrics for a permanent financing exit.

Key Strategy

Bridge Loan Function

Value-Add Outcome

Bridge to Stabilization

Provides 12-24 months of runway with interest reserves.

Allows time to increase occupancy, raise Average Daily Rate (ADR), and boost NOI to meet future, higher DSCR requirements.

Bridge to Permanent Exit

Pays off the immediate CMBS threat, cleaning up the title.

Provides the runway for a future long-term financing solution (e.g., Fannie Mae/Freddie Mac loans for stabilized assets or a favorable new CMBS exit).

Bridge to Renovation (PIP)

Can include financing for the Property Improvement Plan (PIP) or strategic CapEx.

Completing brand-mandated renovations makes the asset more competitive, increases revenue, boosts its appraisal value, and thus facilitates the final permanent refinancing. (This relates closely to construction for hospitality property financing elements).

In essence, the bridge loan serves as a highly leveraged, temporary construction/stabilization loan that pivots the asset from a distressed state (low DSCR, poor valuation) to a desirable, bankable asset.

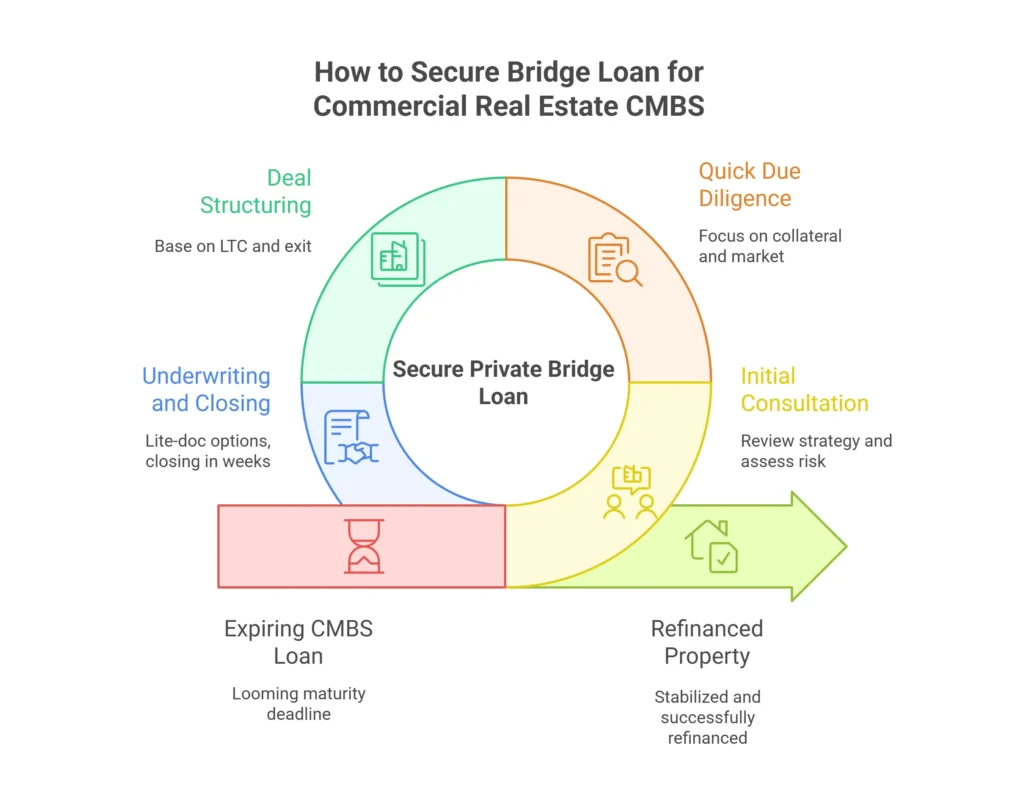

The Application Process: How to Secure Private Bridge Loan for Commercial Real Estate CMBS

The private bridge loan process for CMBS maturity is streamlined to maximize speed and efficiency.

Initial Consultation & Strategy Review: The borrower presents the expiring CMBS loan information, the hotel’s current operational status, and the detailed exit strategy (the plan to secure permanent financing within the bridge term). The lender assesses the immediate risk and the plan’s viability.

Quick Close Private Bridge Loan CMBS Due Diligence: Due diligence is rapid and primarily focused on the collateral (the hotel property), the market, and the borrower’s experience. The lender will immediately order a third-party appraisal to determine the current and stabilized property value.

Structuring the Deal: Focus on LTV and Exit Strategy: The lender structures the loan based on the Loan-to-Cost (LTC) for the entire project (payoff + PIP/CapEx) and the strength of the exit plan. The structure may include an interest reserve to cover payments until the property stabilizes, reducing the immediate cash flow burden on the owner.

Underwriting and Closing: Once the appraisal and environmental reports are satisfactory, the loan is underwritten and closed. Private lenders often offer “lite-doc” or “no-doc” options, meaning less reliance on extensive personal financial histories and more focus on the property’s cash flow potential. Closing occurs within 2-4 weeks critical for meeting the CMBS maturity deadline.

Understanding your private bridge loan eligibility CMBS largely hinges on having a clear, actionable plan to stabilize the hotel and refinance successfully before the bridge loan’s term ends.

Comparing Options: Bridge vs. Permanent Financing

A fundamental understanding of the difference between bridge loan and permanent financing CMBS highlights why a bridge loan is the only viable financing for maturing CMBS debt alternative in a distressed maturity scenario.

Feature

Private Bridge Loan (The Solution)

Permanent Financing (The Goal)

Term

Short (6–36 months)

Long (5–10 years, up to 30-year amortization)

Speed

Very Fast (2–4 Weeks)

Slower (2–4 Months)

CMBS Maturity

Ideal for Immediate Need (Rapid payoff)

Requires Stabilization (NOI, DSCR, LTV must meet rigid requirements)

Flexibility

High (Underwritten based on future value/business plan)

Lower (Underwritten strictly on current DSCR/LTV)

Cost

Higher (Rate/Fees)

Lower (Rate/Fees)

The bridge loan is designed to be temporary, absorbing higher short-term costs for the immense value of equity preservation and time. It is the vital link between a financially unstable present and a profitable, stable future.

The Financials: Private Bridge Loan Providers Specializing in CMBS

When seeking a private bridge loan for CMBS, the typical terms reflect the increased risk and specialization involved:

Interest Rates: These are generally higher than permanent rates, are usually priced over a base index (like SOFR), and may range from 8.0% to 12.0% or higher, depending on asset risk, leverage, and the lender.

Fees (Points): Lenders charge origination fees, typically 1% to 3% of the loan amount.

Interest Reserves: As noted, many deals are structured with an Interest Reserve a portion of the loan proceeds is held back to pay the debt service during the stabilization period, ensuring the borrower doesn’t have an immediate cash flow strain.

While the upfront cost for the best private bridge loan rates for CMBS is higher than traditional financing, this cost must be weighed against the alternative: the opportunity cost of a default. Defaulting on a CMBS loan can lead to:

Loss of control to the Special Servicer.

Costly fees and penalties that often exceed the bridge loan’s interest.

The eventual forced sale of the asset at a distressed price results in a total loss of equity.

Private bridge loan providers specializing in CMBS understand the complexities of the pooling and servicing agreements (PSAs). They can navigate the process of paying off the CMBS note and obtaining the necessary release in a time-sensitive, professional manner, safeguarding your investment.

Beyond the Bridge: Your Full-Service Partner in Hospitality Real Estate Finance

Successfully navigating a CMBS loan maturity requires more than just money; it requires a strategic partner who specializes in the complex world of hospitality finance. At HotelLoans.Net, we go beyond simply funding a private bridge loan for maturing CMBS debt. We position ourselves as your comprehensive financial and consulting arm, guiding your hotel asset from distressed maturity to long-term stability and maximized value.

Why HotelLoans.Net is the Premier Choice for Your Maturing CMBS Debt

Our authority in the hospitality real estate space is built on a foundation of unique competence and a robust lending platform, offering a clear path out of the CMBS maturity crisis.

Underwriting Expertise: We are not transactional brokers. Our team provides 30-year underwriting capability, meaning we evaluate the hotel asset with the same long-term diligence as permanent lenders. We understand hotel markets, property cycles, brand requirements, and operational nuances. This deep knowledge allows us to structure a bridge loan that is not just a stopgap, but a viable, underwritten step toward your ultimate permanent financing goal.

Vast Private Capital Network: Dealing with a maturing CMBS requires immediate, specialized capital. We connect you to an extensive network of over 1,000 private lenders, debt funds, and institutional investors who actively deploy private capital to extend and pay off CMBS debt. This network ensures we find the most competitive, flexible terms available, often bypassing the lengthy processes of conventional banks.

Product Breadth: The CMBS crisis is rarely a one-size-fits-all problem. Our comprehensive suite of financing options ensures your successful exit from the bridge loan:

Bridge Loans (The immediate solution).

Hard Money Loans (For highly distressed or rapid renovation scenarios).

CMBS Loans (For your stabilized, future exit at a competitive rate).

Economic Consulting and Strategy: We serve as your economic consultant, providing strategic guidance for your hotel, motel, and related hospitality properties. Our focus is on the business plan how to increase Average Daily Rate (ADR), execute Property Improvement Plans (PIPs), and ultimately boost the NOI to satisfy future permanent DSCR requirements.

HotelLoans.Net Value Proposition (AIDA Action): We transform a looming threat (CMBS maturity) into a strategic opportunity (increased property value). We provide the time and capital necessary to reposition your asset, ensuring you retain your equity and control, rather than ceding it to a special servicer.

We Speak Your Language: Financing for All Your Hospitality Needs

Our expertise extends across the entire spectrum of hospitality real estate activities. We understand that your capital needs change as your hotel asset matures, stabilizes, or undergoes transition.

“Whether you need funds for a renovation (fix and flip) to reposition your asset, or a short-term solution to avoid default on your hospitality investment property, we have the loan and the expertise.”

We structure financing solutions tailored to your specific hotel class and needs:

Permanent Agency Financing: Expertise in FHA hospitality loans and long-term, non-recourse financing for stabilized assets.

Rural Development: Utilization of USDA B&I loans for properties in eligible rural areas, offering favorable terms for essential community businesses.

Cash Flow & Non-QM Solutions: Access to State Income Loans and specialized debt products for related real estate activities, such as associated retail pads or fractional ownership structures.

Ground-Up and Heavy Renovation: Strategic financing for comprehensive property overhauls, linking the initial construction for hospitality property financing to the bridge-to-permanent loan structure.

Ready for a Consultation? Your Next Step to Financial Security

The CMBS maturity clock waits for no one. The moment your loan transfers to special servicing, your options shrink, and the costs skyrocket. Don’t wait for special servicing.

Your next step to securing your hotel’s financial future is a simple, direct action:

Contact HotelLoans.Net today for a free, no-obligation “CMBS Maturity Strategy Session.”

During this session, we will:

Review your current CMBS loan documents and maturity date.

Analyze your property’s current and stabilized financial metrics (NOI, DSCR, LTV).

Outline a customized private bridge loan for maturing CMBS debt solution, complete with a clear, underwritten exit strategy.

Partnering with HotelLoans.Net means securing:

Certainty: A clear, swift path to paying off the CMBS balloon.

Expertise: Guidance from a correspondent lender with 30 years of hospitality underwriting experience.

Control: The ability to execute your business plan and increase property value, rather than being forced into a distressed sale.

Take control of your debt and preserve your equity. Let’s build your path to permanent financing today.

Conclusion: Leverage Private Capital to Secure Maximum Hotel Value

The threat of a looming balloon payment from a maturing CMBS loan is the most urgent challenge facing many hotel owners today. However, this moment of crisis is also an opportunity for strategic realignment.

A private bridge loan for maturing CMBS debt is the decisive mechanism that gives you control. It is the capital injection that buys you the critical time (12-36 months) needed to execute a value-add plan be it a mandatory PIP, NOI stabilization, or strategic repositioning to ensure your hotel asset meets the stringent DSCR and LTV requirements of permanent financing. Don’t allow a bureaucratic special servicer to dictate the fate of your investment.

Secure Your Strategy Today: Ready to transition from vulnerability to financial security?

FAQs

How does a CMBS maturity default affect the hotel owner’s personal financial standing or credit?

A CMBS loan is typically non-recourse, meaning the borrower is generally not personally liable for the debt, minimizing the direct impact on their personal credit score if the loan defaults due to maturity. However, most CMBS loans contain “bad boy” carve-outs. Suppose the maturity default is triggered by actions considered to be in bad faith (such as fraud, misapplication of funds, or voluntary bankruptcy). In that case, the non-recourse protection can be invalidated, making the borrower personally liable and severely damaging their business and personal credit. Utilizing a private bridge loan quickly avoids this entire risk.

Are there prepayment penalties on a private bridge loan, especially if I secure permanent financing faster than expected?

While many residential or simple bridge loans offer flexible, no-penalty prepayment, private bridge loans for large commercial real estate (CRE) CMBS maturity payoffs often include a prepayment structure to ensure the private lender earns a minimum yield. This might take the form of:

Minimum Interest Requirement: You must pay at least six or twelve months of interest, regardless of how quickly you repay the loan.

Minor Step-Down Penalty: For example, a 3% fee in year one, 2% in year two, and none thereafter.

It’s crucial to negotiate the prepayment terms before closing, as paying a minor penalty is still better than paying higher bridge loan interest for an unnecessary period.

What are the key alternatives to a bridge loan for maturing CMBS hotel debt, other than refinancing or a sale?

Beyond a full refinance or sale, hotel owners facing CMBS maturity have limited alternatives, but two viable options include:

Loan Modification/Extension: Negotiating a short-term extension with the Special Servicer. This is often costly (high fees, increased interest rate, additional reserves) and non-guaranteed, but it can buy a few months.

Mezzanine Financing or Preferred Equity: Bringing in a new capital partner or mezzanine lender who sits behind the existing CMBS loan (if allowed by the PSA) or the new bridge loan. This equity injection cures the short-fall required for the refinance or maturity payoff without requiring a complete ownership change.

Can a private bridge loan include funding for a brand-mandated Property Improvement Plan (PIP)?

Yes, a significant advantage of the private bridge loan for hospitality assets is its ability to fund the Property Improvement Plan (PIP) or other necessary capital expenditures. The loan size is often structured based on the total Loan-to-Cost (LTC), including the CMBS payoff, closing costs, and the budgeted PIP funds. The bridge lender views the PIP as a critical component of the exit strategy, as the renovation increases the hotel’s future NOI and stabilizes the value needed for the permanent refinance.

What documentation or specific eligibility requirement is most critical for securing a private bridge loan for CMBS maturity?

The most critical requirement for private bridge loan eligibility CMBS is a clearly defined and credible Exit Strategy, which is often more important than the property’s current low DSCR. The lender needs to see a comprehensive, underwritten plan detailing how and when the hotel will be stabilized (e.g., through renovation/PIP, new management, increased occupancy/ADR) and which permanent financing source (e.g., CMBS, Fannie Mae, Life Company) will repay the bridge loan before its term expires.

Facebook Twitter Pinterest LinkedIn The 2026 hospitality real estate market is a study in contrasts. While the global industry is projected to reach a staggering

Facebook Twitter Pinterest LinkedIn The hospitality real estate landscape in 2026 is moving at a velocity that traditional investors find dizzying. We are currently navigating

Facebook Twitter Pinterest LinkedIn The hospitality sector in 2026 is witnessing a powerful shift. Individual investors and hospitality brokers are moving away from the rigid,

Facebook Twitter Pinterest LinkedIn The hospitality real estate market in 2026 is a landscape of “two-speed” performance. While the broader economy continues to grow steadily,

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.