Right now, other commercial real estate buyers are snapping up cash-flowing roadside properties across the country while you wait on the sidelines. According to the World Travel & Tourism Council and Oxford Economics, the global travel sector just hit an all-time high of $11.6 trillion, representing nearly 10% of global GDP. Road trips are back. Middle-class travelers are choosing driving vacations over expensive flights, creating a massive surge in demand for rooms. If you do not buy that local motel this year, another buyer will take those keys and those daily cash revenues. To get in the game, you need the right debt. That is why getting an SBA loan to buy a motel is the single fastest way to build real wealth in hospitality today.

At HotelLoans.Net, we serve as a specialized correspondent lender, table lender, and super broker. We have thirty years of underwriting experience. We maintain an extensive network of private lenders and institutional investors, offering 75 distinct loan options. Our platform focuses entirely on real estate debt origination. We provide financial consulting services to help you acquire these assets, but we do not run your hospitality business. We are here to get your deal funded.

Is government money really better? Comparing conventional vs. SBA loan for motel purchase

Selecting the right mortgage determines your monthly cash flow. Many buyers struggle to compare conventional vs. SBA loans for a motel purchase. Conventional bank loans require a large down payment. Usually, a bank wants you to put down 25% to 40% of the purchase price. That ties up too much cash. You will have no money left to upgrade the rooms.

SBA loans require far less cash up front. You can get into a property with 10% to 15% down. Also, conventional bank loans often come with balloon payments after 5 or 10 years. This forces you to refinance under stress. SBA loans offer fully amortized terms up to 25 years. You never have to worry about a sudden balloon payment.

Financial Parameter

Conventional Commercial Loan

SBA 7(a) Loan Program

SBA 504 Loan Program

Max Loan-to-Value (LTV)

Up to 75%

Up to 90%

Up to 90%

Sponsor Down Payment

25% to 40%

10% to 15%

15% to 20%

Amortization Period

15 to 30 years

Up to 25 years

Up to 25 years

Typical Repayment Term

3 to 15 years

10 to 25 years

10, 20, or 25 years

Balloon Payment Rule

Common after 5 to 10 years

No balloon payments allowed

No balloon payments allowed

Recourse Structure

Fully recourse or non-recourse

Fully recourse personal guaranty

Fully recourse personal guaranty

Another key factor is property classification. Most commercial lenders treat motels as passive real estate investments. Yet, the government has a different view. Under SBA underwriting rules, motels are considered owner-occupied properties. This means the government looks at the actual business cash flow rather than just the real estate value. It allows us to help you secure much higher leverage.

What does it actually take to get approved? Evaluating the sba 7a loan requirements for motel purchase

The SBA 7(a) program is the most common vehicle for buying motels. It is highly flexible. You can use it to buy real estate, secure working capital, and purchase new furniture. But first, you must meet the SBA 7 (a) loan requirements for a motel purchase. These rules ensure your target property qualifies as a viable small business.

First, the motel must operate for profit. It must be located within the United States. It must also meet the SBA size standards. For motels, this means your average annual receipts cannot exceed $7.5 million. You must show that you cannot get a conventional loan on reasonable terms elsewhere.

Lenders will study your debt service coverage ratio. This is a simple math formula that looks like this:

SBA guidelines state the minimum DSCR is 1.15x. In the real world, most active lenders look for a DSCR of 1.25x or higher for motels. This gives the business a safety cushion.

Keep in mind that recent policy changes are strict. Small businesses with immigrant or mixed-status ownership no longer qualify for SBA loans. This rule applies to both the 7(a) and 504 programs. If you fall into this category, we can help you find alternative private debt.

Leveraging the SBA 504 loan for motel construction and purchase

If you want to build a new property or buy an older motel that needs a massive overhaul, the 7(a) program might not be enough. That is where the SBA 504 loan for motel construction and purchase comes into play. This program is built for fixed assets and real estate expansion.

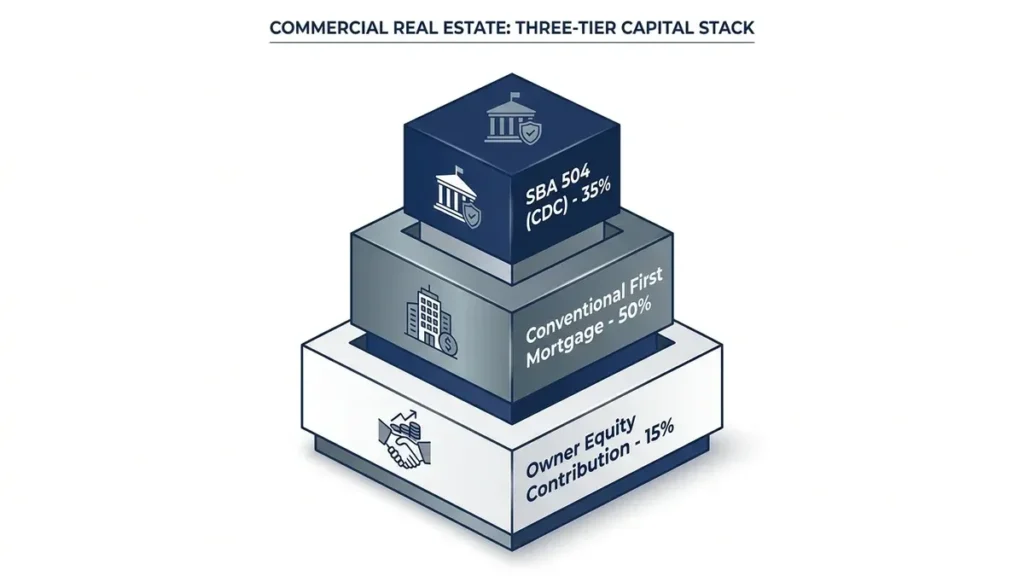

The 504 loan uses a three-tier capital structure:

A first mortgage from a conventional lender covers 50% of the project cost.

A second mortgage from a Certified Development Company (CDC) covers 35%.

Your equity contribution covers the remaining 15%.

Normally, the 504 down payment is 10%. But the SBA classifies motels as special-purpose properties. This classification raises the required down payment to 15%. If the motel is also a brand-new business, the down payment rises to 20%.

You can also use the 504 program to go green. If you add energy-efficient HVAC systems, solar panels, or thick insulation, you can qualify for the SBA Green Energy Program. This program allows you to get up to $5.5 million per CDC loan. It is a smart way to lower your utility bills and get more funding.

What are the hidden traps? Analyzing the pros and cons of an SBA loan for a motel purchase

No loan is perfect. Before you sign the paperwork, you must weigh the pros and cons of an SBA loan for a motel purchase. Government-backed loans offer significant benefits, but they also come with strict rules.

The Pros

Low down payments: You can buy a motel with as little as 10%-15% down. Conventional commercial loans require 25% to 40% down payment.

Longer terms: You get a full 25-year repayment schedule. There are no balloon payments or refinancing pressures.

Total financing package: You can bundle the property purchase, your room renovations, and your working capital into a single loan.

No extra collateral: If the motel appraises for the full loan amount, the lender will not require you to pledge your personal home.

The Cons

Personal guarantees: Anyone who owns 20% or more of the business must sign an unlimited personal guarantee. If the business fails, your personal assets are on the line.

Slow closing times: It takes 60 to 90 days to close an SBA loan. Conventional loans can sometimes close faster.

Variable rate risk: Most SBA 7(a) loans have variable rates. If the Federal Reserve raises rates, your monthly payment will go up.

Strict legal rules: You must meet all federal citizenship and legal residency standards to qualify.

Why the SBA Loan to Buy a Motel is Your Best Bet

This program exists to help everyday people own profitable businesses. Motels are cash-flowing assets. People will always need a clean, affordable place to sleep. By using an SBA loan to buy a motel, you can acquire a million-dollar property for a fraction of the cost.

You do not need a massive corporate balance sheet. You just need a solid property, a clean credit history, and a good plan. Our team at HotelLoans.Net is ready to look at your deal. We can help you pick the right program from our 75 different options.

Decoding SBA loan interest rates for motel financing

Interest rates dictate your monthly overhead. You must understand how SBA loan interest rates for motel financing are set. Lenders calculate these rates using a base index plus a personal risk spread.

For SBA 7(a) loans, the base index is the Prime Rate. As of mid-2026, Prime is high, resulting in overall variable rates ranging from 9.75% to 14.75%. This variable structure can be scary. If national interest rates rise, your monthly debt payment will increase.

SBA 504 loans are different. The CDC portion is tied to US Treasury sales. This means you get a fixed interest rate locked in for 25 years. Currently, 504 effective rates hover between 5.61% and 5.99%. This is one of the lowest fixed rates available for commercial real estate. It gives you stable, predictable monthly payments.

What credit score is needed for an SBA motel loan approval?

Your personal credit history is the first thing underwriters check. They want to see that you handle your personal bills on time. Many buyers ask: What credit score is needed for an SBA motel loan approval?

Most SBA lenders want to see a personal credit score of 680 or higher. If your score is 720 or above, you will get faster approvals and better interest rates. But do not lose hope if your score is lower. Some lenders will approve you with a score as low as 640.

If your score is on the lower side, you must offer compensating factors. These factors include a higher cash down payment, significant cash reserves remaining after closing, or five years of successful hotel management experience. Lenders will also run a global cash flow analysis. They combine your personal income, the motel’s net income, and any other business debts to make sure you have plenty of cash to cover all payments.

Is it real? Buying a motel with an SBA loan no money down

You have probably seen advertisements online claiming you can buy a business with zero cash. Let’s look at the reality of buying a motel with an SBA loan, no money down. The short answer is: you cannot get 100% financing from a bank without some form of equity.

The SBA mandates a minimum 10% equity injection for business purchases. Because motels are special-purpose properties, that requirement rises to 15%. If you are a new owner, it can go up to 20%.

Yet, there is a legal workaround. You can structure a zero-cash down payment by using cross-collateralization. If you already own another commercial property, you can pledge the equity in that building as your down payment. The lender will place a lien on your existing property. This satisfies the 15% equity injection rule, allowing you to close the deal with no physical cash out of pocket.

Pre-Approval Strategy: How to qualify for an SBA loan to buy a motel

Before you start looking at properties, you need a pre-approval letter. This document shows sellers that you are a serious buyer. You must learn how to qualify for an SBA loan to buy a motel before you make an offer.

First, compile your financial records. You will need three years of personal and business tax returns. Next, pull your personal credit reports. Pay off any past-due debts, credit card balances, or small collections. If you have any past bankruptcies, they must be fully discharged.

You must also demonstrate the management skills to run a lodging business. Underwriters do not want to fund a buyer who has never worked in customer service or hospitality. If you do not have hospitality experience, you can partner with an experienced manager who will own a small slice of the business.

Writing a winning business plan for an SBA motel loan application

Every lender will demand a formal business plan. This document must convince the bank that your property will make money. You must create a detailed business plan for an SBA motel loan application submission.

Your business plan must include several core elements:

Executive Summary: A clear explanation of the motel, its location, and why you want to buy it.

Management Bios: Detailed resumes showing your hospitality background and operational experience.

Local Market Analysis: Hard data on local travel demand, major highways, and nearby tourist attractions.

Competitor Audit: A list of direct competitors, their room rates, and their occupancy levels.

Financial Projections: Three years of monthly pro forma statements showing your expected room revenues and operational expenses.

Your projections must be realistic. Do not just guess your numbers. Base them on actual historical data from the property and local tourism reports.

Preparing for the SBA loan down payment for buying a motel

Saving up for your down payment takes time and planning. You must know how to structure your SBA loan down payment for buying a motel. The source of your down payment funds will be heavily scrutinized.

Underwriters will require consecutive bank statements to trace your money. They want to make sure the cash is yours. You cannot use another personal loan to cover your down payment.

Pledged equity in other real estate, cash from your savings accounts, and retirement funds are all acceptable sources. You can also use gift funds from family members. If you use gift funds, the donor must sign a formal gift letter. This letter must state that the money is a gift and does not need to be paid back. Keep in mind that you must still contribute at least 5% of the total project cost from your own pocket.

Down Payment = {Purchase Price} +{PIP Costs})* 0.15

Lenders also require post-closing liquidity. This means you must have extra cash left in your bank account after the deal closes. Most lenders want to see enough cash to cover 3 to 6 months of debt payments. This protects your business during seasonal low months.

The Step-by-Step sba loan application process for buying a motel

The path from your initial application to getting the keys takes time. Navigating the SBA loan application process for buying a motel requires patience and organization.

Step 1: Prequalification. You submit your tax returns, credit reports, and the motel’s historical financial statements to the lender.

Step 2: The Term Sheet. The lender issues an initial proposal outlining the interest rate, down payment, and loan terms.

Step 3: Underwriting. The bank digs deep into your records, orders third-party reports, and verifies your cash assets.

Step 4: SBA Submission. The lender packages the loan and sends it to the SBA for final federal approval.

Step 5: Closing and Funding. The final legal documents are signed, your down payment is wired, and the lender releases the funds.

This entire process takes 60 to 90 days. Working with an experienced lender who knows the hospitality sector can speed things up.

Doing your homework: Due diligence before buying a motel with an SBA loan

You must never buy a property blindly. Conducting thorough due diligence before buying a motel with an SBA loan is the only way to avoid buying a money pit.

First, you must order a Smith Travel Research (STR) report. This report shows the historical performance of your target motel and its competitors. It tracks three key indices: the Market Penetration Index (MPI), the Average Rate Index (ARI), and the Revenue Per Available Room Index (RGI).

Let’s look at the formulas:

MPI = {Target Property Occupancy}\{Competitive Set Average Occupancy}} *100

ARI = {Target Property ADR}\{Competitive Set Average ADR}}* 100

RGI = {Target Property RevPAR}\{Competitive Set Average RevPAR}}*100

An RGI of 100 means your motel is performing at the same level as its competitors. An RGI below 90 indicates the property is underperforming, which could signal poor management or aging facilities.

Next, hire a professional commercial inspector. They will check the roof, the HVAC units, and the plumbing. Older motels often have massive deferred maintenance issues. You must also check for brand-mandated Property Improvement Plans (PIPs). If the motel is part of a franchise, the brand will require you to upgrade the lobby, guestrooms, and exterior sign within 3 years. These PIP costs can easily exceed $200,000, and you must include them in your initial loan request.

SBA loan closing costs when buying a motel

Many buyers forget to budget for transaction fees. You must prepare for SBA loan closing costs when buying a motel. These fees can add up to a significant amount of money at the closing table.

Some of the most common closing costs include:

SBA Guaranty Fee: This fee is charged by the government to back the loan. It can range from 2% to 3.75% of the guaranteed loan amount.

Commercial Appraisal Fee: Lenders require a professional commercial appraisal to verify the property’s market value. This costs $3,000 to $6,000.

Phase I Environmental Report: The bank will require a Phase I Environmental Site Assessment (ESA) to assess for soil contamination or the presence of old fuel tanks.

Lender Fees: These include loan packaging, legal review, and underwriting fees.

Franchise Transfer Fees: If you are buying a branded motel, the parent brand charges a transfer fee to issue a new franchise agreement in your name.

Who should you trust? Finding the best SBA lenders for motel acquisition

Not all banks are good at hotel lending. Motels are high-risk assets, and many local credit unions do not understand the industry. To succeed, you must partner with the best SBA lenders for motel acquisition.

Live Oak Bank: Live Oak is the largest SBA lender in the nation. They approved $2.85 billion in 7(a) loans in FY2025 and have a dedicated hospitality division.

Celtic Bank: Celtic is a top-ten national lender that specializes in mid-market acquisitions and hotel construction financing.

People’s Bank: This bank specializes in flagged hotels. Their underwriting team works directly with major brands like Wyndham and Choice Hotels to streamline franchise transfers.

TMC Financing: TMC is a leading Certified Development Company. They specialize in 25-year fixed-rate SBA 504 loans for large hospitality deals.

Bridge Marketplace: This online platform connects you with a vast network of preferred lenders. You submit a single application, and multiple banks compete to fund your deal.

How to scale from an SBA loan for a first-time motel owner to a portfolio empire

Starting out can feel overwhelming. Landing your first deal as an SBA loan for a first-time motel owner is a major milestone. But once you stabilize the property and build equity, you do not have to stop there.

You can use your first motel to build a regional portfolio. Once your property is performing well, you can cash out or refinance up to 90% of the appraised value under the SBA 504 Debt Refi program. You can use that cash as the down payment on your next acquisition.

At HotelLoans.Net, we are built to support your growth. If you outgrow standard SBA limits, we offer alternative financing products. We can help you secure bridge loans, hard money, DSCR loans, USDA B&I loans, CMBS debt, and FHA commercial property investment loans.

We also run referral programs for real estate brokers. If you are an experienced broker or new to the industry, our exclusive and non-exclusive referral programs are open to you. We provide expert advice to help your clients secure financing for land purchases, construction, and value-add fix-and-flip strategies.

What happens if things go wrong? Defaults and debt modifications

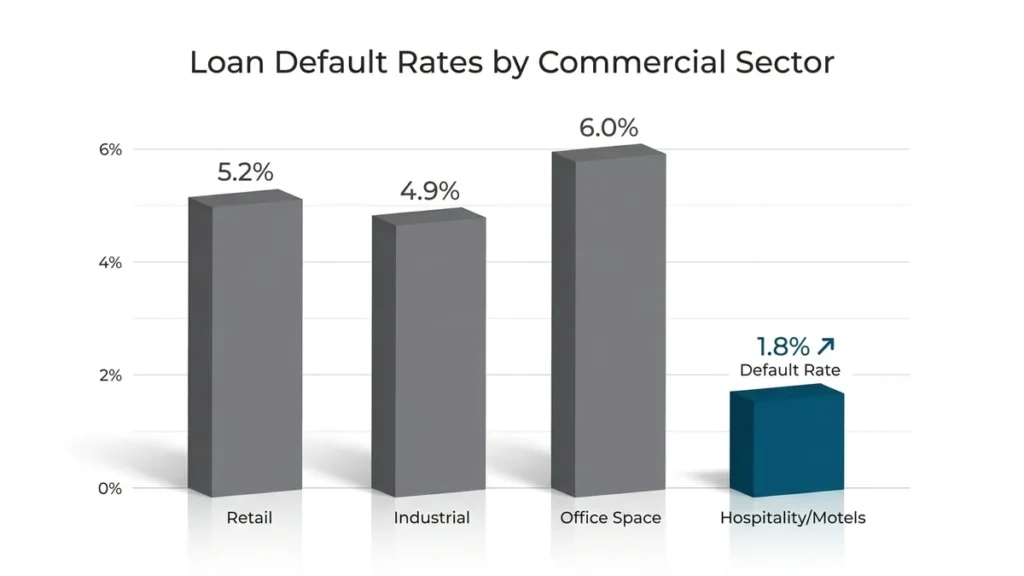

Running a lodging business comes with risk. In 2022 and 2024, the Federal Reserve hiked interest rates, driving the Prime Rate up to 8.50%. This rate shock caused standard variable SBA monthly payments to jump by 50% or more, triggering a wave of defaults across the small-business sector.

Surprisingly, motels and hotels have maintained a low default rate of just 1.8% compared to other sectors. But if you find your property struggling, you must act fast.

Temporary Deferment

If your business experiences a short-term slump, you can ask your lender for a temporary deferment. If approved, the bank can suspend your principal and interest payments for 3, 6, 9, or 12 months. You must submit detailed pro forma statements showing that a turnaround is imminent.

Loan Modification

If your property value drops significantly, you can request a formal loan modification. This process allows you to adjust your interest rate or extend your amortization schedule to lower your monthly payments. You will need to submit a formal proposal and provide updated financial disclosures.

SBA Offer in Compromise (OIC)

If the motel must close, the bank will liquidate the business assets. If a deficiency balance remains, your personal assets are at risk due to the personal guarantee you signed. You can resolve this debt through the SBA Offer in Compromise (OIC) program.

The OIC allows you to settle the remaining debt for a smaller lump-sum payment. To qualify, you must submit full financial disclosures, including SBA Form 1150 and Form 770. You must act within 60 days of receiving your official deficiency notice. If you wait too long, the debt is sent to the Department of the Treasury. Once there, the government adds massive 32% collection fees, making a settlement nearly impossible.

When you use an SBA loan to buy a motel, you are taking a proven path to long-term commercial real estate success. You get high leverage, low rates, and a stable capital structure. At HotelLoans.Net, we have thirty years of underwriting experience to guide you through the process. Reach out to our team today to get your deal pre-approved and funded.

FAQs

Can SBA 504 refinance existing SBA loans?

No. You cannot use the SBA 504 program to refinance an existing SBA loan or other federal debt. This financing option only permits you to refinance conventional commercial mortgages that do not already carry any government guarantees.

Does an SBA 504 loan limit the total project size?

No. There is no maximum project cost limit for SBA 504 loans. While the SBA debenture portion caps at five and a half million dollars, the conventional first mortgage can be scaled as large as needed to fund your purchase.

Can you buy unflagged independent motels?

Yes. You can use SBA loans to buy unflagged independent motels. While many lenders prefer branded franchises due to lower operational risk, several specialized lenders in our network actively approve unbranded hospitality properties with strong historical cash flows.

Can you buy passive motel investments?

No. SBA rules require you to operate the motel directly. You cannot use these federal loans for passive real estate investments. Even if you hire a management company, you must still maintain active daily oversight of the lodging business.

Can you refinance conventional motel loans?

Yes. You can refinance conventional motel debt using SBA programs. This is an excellent strategy for exiting expensive variable-rate bridge loans or maturing balloon notes, allowing you to lock in stable interest rates and longer amortization terms.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.