The global hospitality real estate market is hitting a massive $5.12 trillion mark in 2026. This is a time of high energy and big deals. You see it in the urban skylines and the coastal resorts. Investors are moving fast to grab a piece of the action. But behind the bright lights, the money side of things is getting more complex. If you want to grow, you need to master hotel financing.

At HotelLoans.Net, we see this every day. We are not just a middleman. We are a “super broker” and a correspondent lender. We have 30 years of underwriting skills. We know what lenders want to see before you even ask. We offer 75 different loan options. We help people buy land, build hotels, or fix up old motels. We do not run your hotel, but we make sure you have the money to own it.

The market is shifting. We are moving from a quick recovery to a steady, normal state. Experts at Forbes and The Economist say that operating facts now drive value more than just hype. You have to look at the numbers. In 2026, those numbers tell a story of big risks and even bigger rewards.

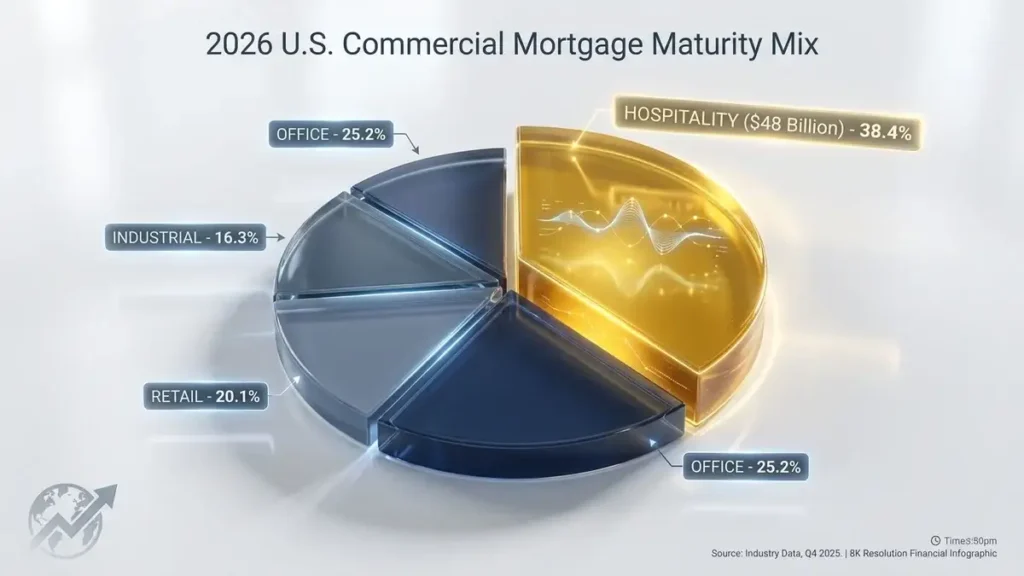

Is the $48 Billion Refinancing Wall About to Collapse?

The biggest story in hotel financing today is the “refinancing wall.” About $48 billion in hotel debt is coming due right now. Most of this debt was signed back when rates were 3% or 4.5%. Now, those same owners are looking at rates between 6.25% and 7.5%. This is a 40% jump in cost.

Many owners cannot handle these new costs. Their properties are not making enough cash to cover the new payments. This is causing a spike in debt trouble. By late 2025, hotel delinquency hit 7.29%. This creates a huge opportunity. We are seeing more hotel financing for distressed properties than ever before. If you have the cash, you can buy these assets at a discount. You need the right lender to bridge the gap.

Many people ask us, “What is a hotel’s CMBS loan?” CMBS stands for Commercial Mortgage-Backed Securities. These are loans that get bundled together and sold to big investors. They are popular because they offer fixed rates and no personal risk to the owner.

But there is a catch in 2026. Lenders are now looking at “debt yield” instead of just property value. They want to see that your hotel generates enough profit to pay the debt, even if travel slows. Most CMBS lenders now want a debt yield of at least 10%. If your hotel only makes 8%, they will cut your loan amount.

This is why many owners are stuck. They have a $10 million loan ending, but the bank will only give them $8 million for the new one. They have to find $2 million in fresh cash to keep the property. This is the “refinancing wall” in action.

Why are Small Hotel Loan Requirements Getting Harder?

If you are a first-time buyer or looking at a smaller property, you might face a wall of your own. Small hotel loan requirements are getting much tighter. Banks are worried about inflation and high labor costs. They want to see a history of success.

To get a loan for a small hotel in 2026, you generally need:

A personal credit score of 680 or higher.

A “Global DSCR” of 1.25x. This means your total income across all your businesses must be 25% higher than your total debts.

Cash reserves equal to 12 months of loan payments after you pay the down payment.

Direct experience running a hotel or a contract with a professional management firm.

If you don’t meet these rules, don’t worry. We work with private lenders who offer Bridge loans options. These focus on the property’s income rather than your personal tax returns. They close fast—often in 2-4 weeks—but they cost more.

SBA Loans for Hotel Purchases: The Best Deal for 2026?

For most of our clients, the Small Business Administration (SBA) is the way to go. SBA loans for hotel purchases offer the lowest down payments. While a typical bank might require 30% down, an SBA loan can be as low as 10% or 15%.

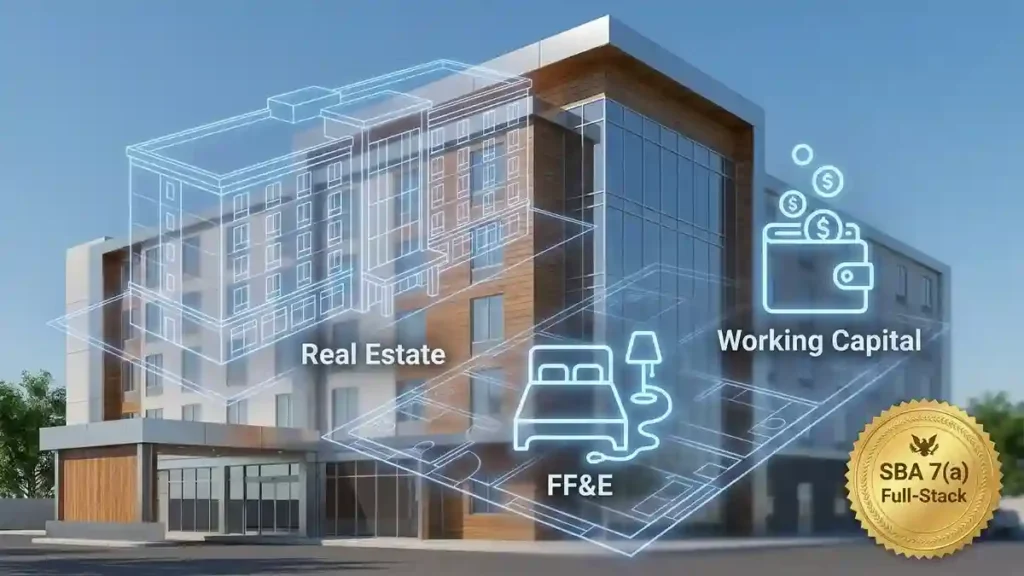

There are two main types. The SBA 7(a) is the “all-in-one” loan. It goes up to $5 million. It covers the building, the furniture, and even working capital. It is great for buying an existing hotel and renovating it. The SBA 504 is for bigger deals, sometimes up to $20 million or more. It gives you a fixed interest rate for 25 years. In January 2026, the 504 rate was around 5.85%. That is a great deal compared to other rates over 7%.

At HotelLoans.Net, we help you pick the right one. We look for the best lenders for hotel acquisition loans in our network of 75 options. We make sure you get the best terms for your specific project.

Can You Really Build a New Hotel in This Market?

Construction is the hardest part of the industry right now. Understanding hotel construction financing rates is vital. Most lenders are scared of new builds because labor and wood costs are so high. The number of new rooms being built is at a five-year low.

But less supply is good for you. It means if you build now, you will have less competition in 2028. Hotel financing options for new builds usually involve a “construction-to-permanent” loan. You pay only interest while you build. Then it becomes a standard mortgage once the hotel opens. You can expect to pay a rate of SOFR plus 3.5% to 5.0% during the build phase.

Are Government Grants for Hotel Development Just a Myth?

You might hear about “free money” for hotels. While it is not exactly free, there are government grants for hotel development and low-cost funds. Most of these come from state and local levels.

For example, states like Utah and Illinois have tourism grants. They want to help you build attractions that bring in visitors. Some grants support “impact mitigation” if your hotel benefits the local community. There is also the USDA B&I loan program. If your hotel is in a rural town with fewer than 50,000 people, the USDA will guarantee your loan. This can get you a 30-year loan term, which makes your monthly payments very low.

Source

Program Name

Typical Purpose

Federal (USDA)

B&I Loan Program

Rural Hotels (Pop. < 50,000)

State (Illinois)

Tourism Attractions Grant

Improving local landmarks

State (Georgia)

Hotel/Motel Vouchers

Homeless prevention support

Local (Utah)

Rural County Grant

Economic planning for hotels

Financing the “Stuff” Inside Your Hotel

When you buy a hotel, you aren’t just buying a building. You are buying beds, TVs, and carpets. This is where hotel FF&E financing solutions come in. FF&E stands for Furniture, Fixtures, and Equipment.

Franchise brands like Hilton or Marriott require you to update these things every few years. These are called Property Improvement Plans (PIPs). A PIP can cost $7,500 to $15,000 per room for a mid-scale hotel. If you don’t have $1 million sitting in the bank, you need a specialized loan for this. We work with lenders like Stonehill, who specialize in PIP financing. They know exactly what the brands want and how to fund it.

How to Win the Interest Rate Game

Everyone wants the lowest rate. When comparing hotel financing interest rates, you have to look at the “base” and the “spread.” Most loans are tied to the Prime Rate or the 10-Year Treasury.

Prime Rate: 6.75% (used for SBA and small bank loans).

10-Year Treasury: 4.40% (used for CMBS and big institutional deals).

30-Day SOFR: 3.66% (used for bridge and construction loans).

A “spread” is what the bank adds on top. If the bank adds 3% to the Prime Rate, your total rate is 9.75%. Our job at HotelLoans.Net is to find the lender with the smallest spread for your risk level. We search our network to find the most affordable path for you.

The Smart Way to Refinance in 2026

If you already own a hotel, your focus is likely on refinancing a hotel mortgage in 2026. You want to avoid the high rates of the “refinancing wall.” One strategy is to use an SBA 504 loan to pay off a high-interest bridge loan. This lets you lock in a low rate for 25 years.

Another option is to do a “cash-in” refinance. This means you pay down some of the principal to make the bank feel safer. It is painful, but it can save you from losing the property. Securing debt financing for hospitality projects today requires being proactive. Don’t wait until 30 days before your loan ends. Start talking to us six months early.

Why You Need a Super Broker

The world of hotel money is too big to handle alone. One bank might say “no,” while another might say “yes” to the same deal. We know which lenders are hungry for deals in 2026. We help you package your deal so it looks perfect. We review your STR reports, P&Ls, and resume. We make sure you are “investor-ready.”

Whether you are doing a “fix and flip” on a boutique motel or building a luxury resort from the ground up, we have the tools to help. We also offer both exclusive and non-exclusive referral programs for brokers. If you find a great piece of land, call us. We will handle the money.

Conclusion

The year 2026 is a year of big moves. The global market is growing, but the old way of getting money is gone. You cannot just walk into a local bank and expect a great deal. You need to understand debt yields, the CMBS market, and the power of SBA programs.

By focusing on the right hotel financing strategy, you can turn a risky market into a gold mine. Don’t let the “refinancing wall” stop you. Use it as a chance to find distressed deals and grow your portfolio. At HotelLoans.Net, we have been doing this for 30 years. We have 75 loan options and the best network in the business. Let’s build your hospitality empire together. Contact us today to find the loan that fits your future.

FAQs

Can foreign investors get hotel loans?

Yes. Foreign investors can use DSCR loans to buy hotels without verifying personal income. These loans focus on the property’s cash flow. They work for LLCs and corporations, too. It helps you scale your portfolio quickly and easily.

Does the USDA require job creation?

Yes. You must show that your hotel project creates or saves jobs for rural residents. This is a key rule for USDA B&I loans. These loans help small towns grow. They provide up to $25 million for your business.

Can I finance earnest money deposits?

Yes. Specialty lenders offer soft-deposit financing for your earnest money. This lets you move fast on a deal without tying up your own cash. You can get approval in 24 hours. It helps you win against other bidders.

Are FHA hotel loans non-recourse options?

Yes. FHA and HUD loans for residential care or senior living are non-recourse. This means the lender cannot go after your personal assets if you fail. It protects your balance sheet. These loans offer 35-year fixed rates at low interest rates.

Is equity needed for partner buyouts?

Yes. You can use an SBA 7(a) loan to buy out a partner partially. You can also fund an employee buy-in this way. The business must meet small-sized standards. It is a great way to grow your ownership.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.