The hospitality landscape of 2026 is defined by a paradox: record-breaking global travel demand set against some of the tightest lending standards in decades. As the global hospitality market is projected to grow to approximately $5.82 trillion this year, developers are finding that traditional “Hotel Financing” has shifted from a commodity to a strategic asset.

For the modern developer, securing “hotel construction loans” is no longer just about filling a capital gap. It is about navigating a “flight to quality” where lenders prioritize assets with high operational efficiency, sustainable footprints, and clear paths to stabilization. At HotelLoans.Net, we serve as a correspondent and table lender, leveraging our 30-year underwriting expertise and a platform of 200+ private lenders to bridge the gap between ambitious concepts and completed keys.

Why Is the 2026 Market Demanding a “Flight to Quality”?

The current economic cycle has created a K-shaped recovery in the hospitality sector. While the luxury and ultra-luxury segments are seeing Revenue Per Available Room (RevPAR) growth that far outpaces inflation, the economy segment faces significant pressure from rising labor and operational costs.

Institutional data from JLL indicates that global hotel investment volumes are rebounding, up 22% from the 2023 trough, yet capital is becoming increasingly selective. This selectivity is driven by:

The World Cup Catalyst: The 2026 FIFA World Cup is projected to generate nearly $900 million in incremental hotel room revenue across U.S. host cities.

Supply Constraints: Slower supply growth in major U.S. markets, where construction pipelines are often below 2% of existing supply, is creating outsized value for new developments that can actually break ground.

Macro-Volatility: With the Federal Reserve maintaining a “wait-and-see” approach on interest rates, currently sitting in the 3.5% to 3.75% range, developers must prioritize “Hotel Financing” structures that offer long-term stability.

How to Get Hotel Construction Loans in a Selective Market

Understanding “how to get hotel construction loans” in 2026 requires a shift in mindset from simple leverage to “semantic fitness”—the ability to prove to a lender that your project solves a specific market need. Lenders have largely moved away from traditional Loan-to-Value (LTV) limits, focusing instead on Debt Yield and Global Cash Flow.

Modern lenders typically require a minimum debt yield of 10.5% to $12% for the strongest deals. In contrast, bridge-to-construction scenarios may require 14.5% or higher to secure the lowest rates.

Debt Yield = {{Net Operating Income (NOI)}/{Total Loan Amount}}

To qualify, developers must demonstrate:

Management Track Record: Lenders favor “proven operators” with multi-cycle experience.

Post-Closing Liquidity: Many lenders now target a borrower’s net worth greater than the loan amount and liquidity of at least 10% of the loan amount.

Flag Affiliation: Top-tier brands like Hilton, Marriott, Hyatt, and IHG remain the “gold standard” for securing favorable terms.

What Are the Real Hotel Construction Loan Requirements for 2026?

A primary reason for loan denial in today’s market is under-capitalization or inadequate documentation. “Hotel construction loan requirements” have evolved; “back of the napkin” math is a relic of the past.

Essential Documentation Checklist

Firm Fixed-Price Contracts: Lenders now mandate detailed, line-item bids to mitigate the risk of cost overruns, which currently affect 9 out of 10 hotel projects.

Market Feasibility Studies: A deep-dive analysis of local travel trends and competitor performance is mandatory.

STR Reports: These reports serve as the benchmark for revenue sustainability, helping lenders determine whether a property will capture its “fair share” of the market.

Underwriting Metric

2026 Target Range

Impact

DSCR

1.25x – 1.50x

Ensures income covers debt

Loan-to-Cost

55% – 70%

Higher for top-tier flags

Recourse

Typically Full

May shift to non-recourse at $5M+

Amortization

20 – 30 Years

Provides cash flow breathing room

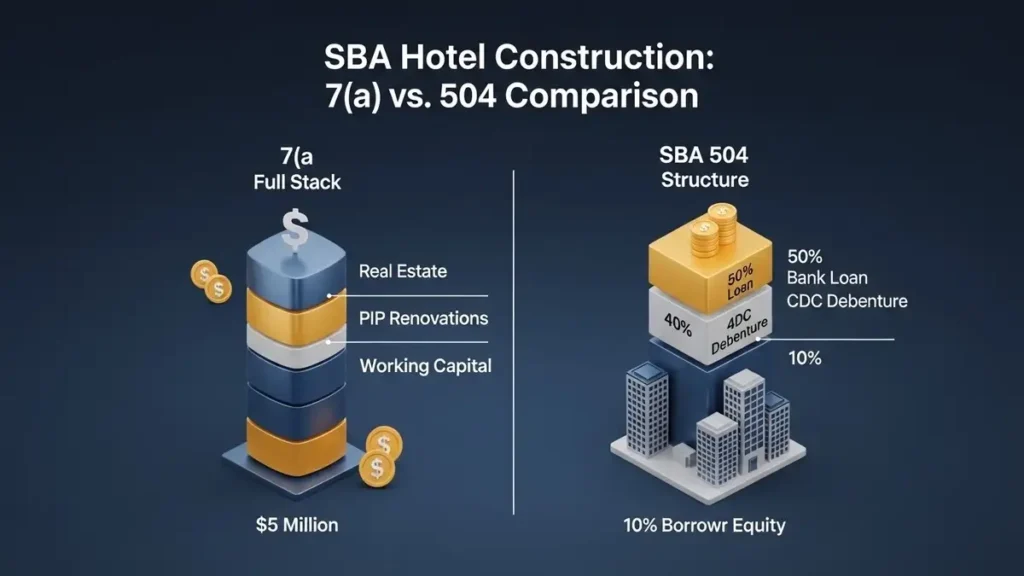

Guide to Hotel Construction Financing: SBA 7(a) vs. 504

For many entrepreneurs, “SBA hotel construction loans” are the most strategic path to ownership, offering lower down payments and longer terms than conventional bank loans.

SBA 7(a) Loans: The “Full Stack” Solution

The SBA 7(a) program is “best for small hotel construction loans” or turnarounds under $6.25 million. It is unique because it can finance the “full stack”—land, construction, brand-mandated Property Improvement Plans (PIPs), and essential working capital—in a single transaction.

Maximum Amount: $5 million.

Down Payment: Typically 10% to 15% for experienced operators.

SBA 504 Loans: Long-Term Rate Stability

For “financing for boutique hotel construction” or larger projects ranging from $7 million to $20 million, the SBA 504 program is superior. It offers a 25-year fixed rate lock on the 40% CDC portion, providing a critical hedge against inflation.

Maximum SBA Portion: $5.5 million.

Structure: 50% bank loan, 40% CDC debenture, 10%-20% borrower equity.

Is Your Project Ready? Typical Down Payment for a Hotel Construction Loan

When “comparing hotel construction loan providers,” the “typical down payment for a hotel construction loan” remains the biggest hurdle for new developers. In 2026, the equity injection ranges from 10% to 30%, depending on the “software” (management) and “hardware” (real estate).

10% Down: Reserved for “construction-to-permanent” loans where the borrower has a 700+ credit score and a lender-approved builder.

20% – 25% Down: The standard for ground-up construction in most markets due to the inherent volatility of labor and material costs.

30%+ Down: Often required for independent hotels outside of top coastal markets or for developers with limited hospitality experience.

Expert Tip: If you already own the land, its appraised value can often be used as land equity, significantly reducing the cash-on-hand requirement for your down payment.

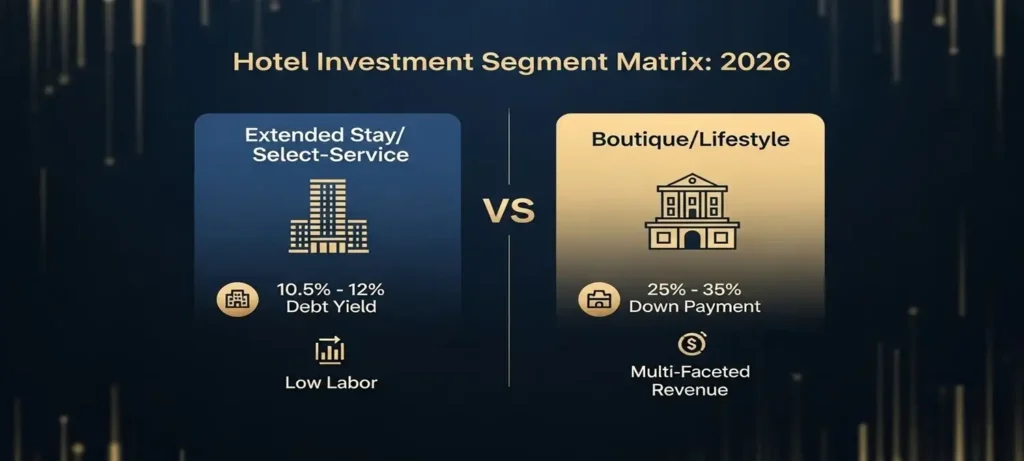

Segment Spotlight: Boutique vs. Extended Stay

The 2026 market shows a clear bifurcation in property type performance. “Construction loans for extended stay hotels” are among the easiest to secure because these assets offer lean operations and predictable income from remote workers and long-term relocations.

Conversely, “financing for boutique hotel construction” requires a more nuanced business plan. Lenders view boutique properties as “multi-faceted revenue engines” that capitalize on F&B and events. Still, they demand higher equity (25% to 35%) due to the higher labor costs associated with a 24/7 “high-touch” experience.

The “Resort Core” Trend

Boutique and lifestyle hotels are increasingly migrating to coastlines and islands, a trend termed “Resort core”. Harvard Business Review highlights that “experience-led” assets are commanding significant premiums, as 65% of travelers now prioritize authenticity and unique experiences over traditional luxury.

Bridge Loans for Hotel Construction Projects: The Path to Stabilization

“Bridge loans for hotel construction projects” are essential for developers who need speed or are repositioning an asset (e.g., converting a non-flagged motel into a branded boutique).

Speed of Funding: Can be funded in days to weeks rather than months.

Cost: Higher interest rates (SOFR +350 to 600 basis points).

Exit Strategy: Typically 12 to 36 months, to refinance into permanent debt once the hotel reaches a 9% to 12% debt yield.

How Can Rural Developers Leverage USDA B&I Loans for Maximum Success?

The USDA Business & Industry (B&I) loan program is a powerhouse for “recreation investment property” and “vacation investment property” in towns with populations under $50,000.

30-Year Terms: Longer than SBA 7(a) or conventional bank loans.

High Leverage: Up to 80% LTV for commercial real estate.

Maximum Loan: Up to $25 million for eligible projects that create jobs in rural economies.

Existing businesses must demonstrate 10% tangible balance sheet equity, while new startups must provide at least 20%. This program is ideal for developers looking to avoid the saturated primary markets and tap into the 95% of U.S. land that qualifies as rural.

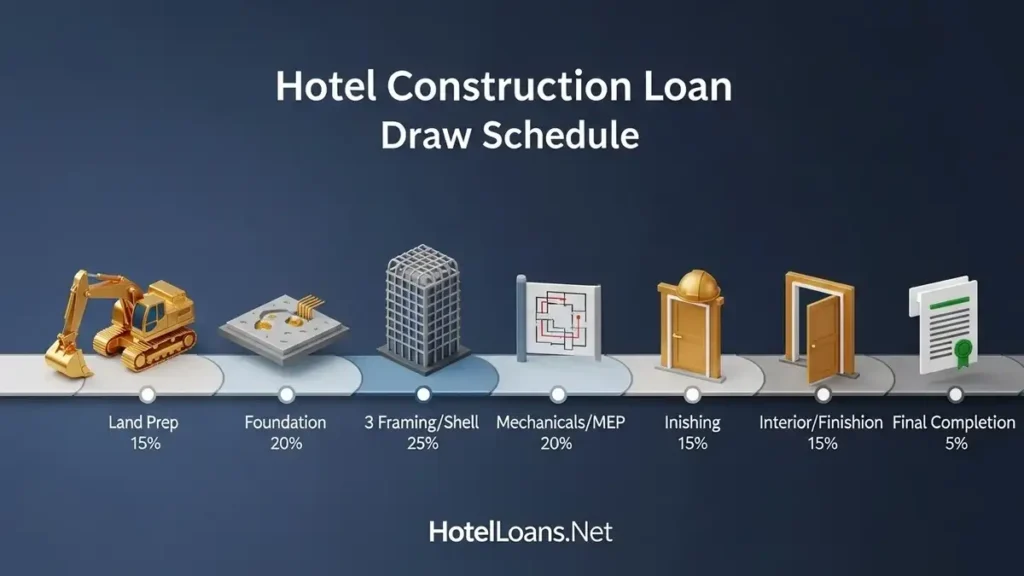

Competitive Strategy: Comparing Hotel Construction Loan Providers

When “comparing hotel construction loan providers,” it is vital to look beyond the interest rate. “New hotel construction loan rates” currently range from 6% to 10%. Still, the structure of the draw schedule is what determines project survival.

Phase

Draw %

Focus

Land & Prep

10% – 15%

Utilities and Site Work

Foundation

15% – 20%

Slab and Waterproofing

Framing/Shell

20% – 25%

Structural Integrity

Mechanicals

15% – 20%

HVAC, MEP trades

Finishes

15% – 20%

FF&E and Interior

HotelLoans.Net manages this process through automated draw workflows, ensuring that funds are disbursed quickly to keep contractors on-site and on-schedule.

The Referral Program: Success for Brokers and Consultants

HotelLoans.Net offers exclusive and non-exclusive referral programs for hospitality real estate brokers. In 2026, the best referral networks have shifted from transactional to relational.

Exclusive Programs: Offer higher splits (25% to 50%) and integrated underwriting support.

Non-Exclusive Programs: Provide flexibility for brokers managing high lead volumes across multiple markets.

We provide “financial advice” for those entering the sector, from fix-and-flip motel projects to massive resort developments. By partnering with a “correspondent and table lender,” brokers can offer their clients 30-year underwriting and access to a diversified capital stack, including CMBS, FHA, and private debt funds.

Conclusion: Securing Your Construction Success

The “guide to hotel construction financing” in 2026 boils down to preparation and partnership. Whether you are building an upscale extended-stay property in Texas or a boutique luxury resort in the Carolinas, your success depends on your ability to meet the market’s “flight to quality” standards.

At HotelLoans.Net, we don’t just provide a loan; we provide a blueprint for growth. By leveraging our 200+ private lenders and investors network and deep expertise in everything from SBA to USDA B&I loans, we help you navigate the complexities of “how to qualify for hotel development loans” so you can focus on building the next iconic guest experience.

Ready to break ground? Contact our hospitality specialists today to secure the capital your vision deserves.

FAQs

Can I use sweat equity for down payments?

No. SBA and conventional lenders typically require actual cash or land equity rather than “sweat equity” for the down payment. Lenders prioritize verifiable capital to ensure the borrower is fully invested financially and capable of covering unexpected project overruns.

Is C-PACE financing available for hotel construction?

Yes. C-PACE is an innovative tool that provides long-term financing for energy-efficient upgrades during hotel construction. It often covers 100% of costs for HVAC, lighting, and solar, allowing developers to preserve liquidity while reducing overall operational expenses for years.

Do hotel construction loans allow interest-only payments?

Yes. Most construction loans are structured with interest-only payments during the build phase to maximize cash flow. Once the property opens and stabilizes, the debt typically transitions into a traditional amortizing loan, often referred to as a mini-perm financing structure.

Can I finance a motel to hotel conversion?

Yes. Financing for conversion or rehabilitation projects is widely available through our platform. These loans cover land purchase, structural renovations, and brand-mandated interior fittings. Conversions are often viewed favorably when they involve reputable flags that provide immediate market recognition and support.

Are hard money loans suitable for quick projects?

Yes. Hard money loans offer rapid access to capital based on property equity rather than credit history. While more expensive than SBA loans, they are ideal for time-sensitive acquisitions or repositions where speed of funding is critical to securing the deal.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.