The hospitality landscape of 2026 is a study in contrasts. While guest spending is projected to reach nearly $805 billion this year—a 1.7% increase over 2025—developers face a “K-shaped” economy in which luxury and high-end select-service assets flourish, while others struggle with structural labor costs. Securing hotel construction financing in this environment is no longer just about finding a lender; it is about architecting a capital stack that survives high interest rates and longer build times.

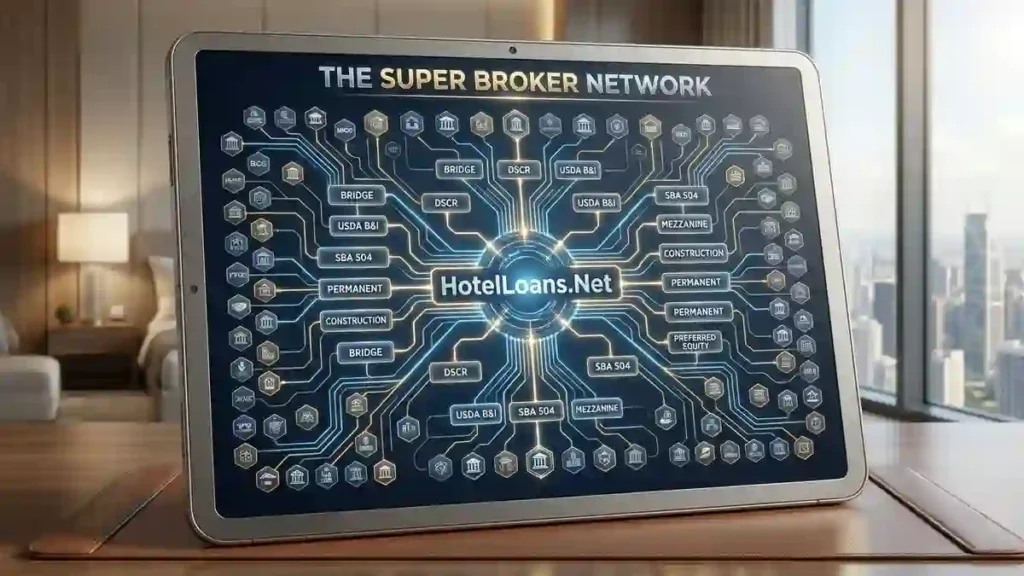

At HotelLoans.Net, we bring 30 years of underwriting expertise to the table. As a correspondent and table lender, we act as your strategic partner, connecting you to 200 private lenders and 75 distinct loan options. We specialize exclusively in real estate investment properties. We don’t run your business; we fund your vision.

Is Hotel Construction Financing the Riskiest Bet in 2026?

Many traditional banks have retreated from the hospitality sector, citing “market volatility” and “operational risk.” However, the data tells a different story. While residential building has faced headwinds, the non-residential building footprint area is expanding by 3.0% in 2026. The recovery is real, but it is selective.

Lenders are no longer funding “commodity” hotels that compete only on price. They are chasing “discipline and certainty”. The risk isn’t in the asset class; it’s in a weak financial strategy. To succeed, you must move beyond the “spray and pray” approach to loan applications and instead leverage targeted hotel construction financing requirements that meet 2026 underwriting benchmarks.

Financing Metric

2026 Industry Benchmark

HotelLoans.Net Advantage

Max Loan-to-Cost (LTC)

55% – 65% (Traditional)

Up to 85% (Select Lenders)

Average Build Time

23+ Months

Fast-track Underwriting

Interest Rates

6.75% – 10%+

75+ Custom Loan Types

Debt Yield Requirement

10.5% – 12%

Flexible Risk Assessments

How to Get Hotel Construction Loan Approval Fast

The guide to hotel construction loan application has changed. Modern underwriting evaluates two distinct components: the “Hardware” (the physical real estate) and the “Software” (the management team and brand power).

To get approved quickly, your application must front-load value. Lenders want to see a clean budget, verified bids, and a clear path to delivery. At HotelLoans.Net, our 30-year underwriting ability allows us to pre-vet your deal before it ever hits a committee, significantly reducing the “time-to-close”.

Step 1: Define Your Investment Criteria

Identify if you are building a “new boutique hotel” or a “limited-service” property. Lenders currently favor upper-midscale and upscale hotels, which lead the pipeline with over 3,600 projects nationwide.

Step 2: Conduct Market Research

You need a detailed “STR Report” to validate your competitive set. In 2026, “Performance is no longer market-driven alone”. You must prove your asset will capture its “fair share” of the local market.

Step 3: Secure the “Capital Stack”

Don’t rely on a single loan. A successful project often involves senior debt, mezzanine layers, and even C-PACE for sustainable infrastructure.

Can You Actually Secure a Hotel Construction Loan Without a Flag?

This is a common question from independent developers. The short answer is: it’s difficult but possible. Branded hotel chains account for 70% of the room share in the USA, and lenders view them as a “sure bet”. However, boutique and lifestyle properties are gaining momentum as travelers seek unique experiences.

If you are going independent, your risk assessment in hotel construction financing must be flawless. Lenders will require:

Higher equity injections (often 20% or more).

A management team with a proven track record.

A location in a “Top 25 Market” like New York or Miami.

SBA Loans for Hotel Construction Projects: 7(a) vs. 504

For many owner-operators, the Small Business Administration remains the best lenders for hotel development financing. SBA loans offer lower down payments and longer amortization periods than traditional commercial loans.

Comparing Hotel Construction Loan Options (SBA)

Feature

SBA 7(a) Loan

SBA 504 Loan

Best For

Working capital & FF&E

Ground-up construction

Max Loan Amount

$5 Million

$15 Million+ (Total Project)

Down Payment

10% – 15%

15% – 20%

Rate Type

Variable (Prime + Spread)

Fixed (25-year Rate Lock)

Equity Injection

Lower requirements

Higher for special-purpose

The SBA 504 loan is particularly powerful for new construction because the 40% CDC portion offers a fixed interest rate for the life of the loan, providing a hedge against inflation. It supports mid-scale and upper-mid-scale national flags without a “hard cap” on total project size.

Why Are Traditional Banks Rejecting Your Hotel Project?

If you’ve been turned down by your local bank, you aren’t alone. Banks selectively lend to developers with existing relationships and prefer lower-leverage deals (≤65% LTC).

The “Super Broker” advantage at HotelLoans.Net is that we bridge this gap. We connect you to debt funds and private credit lenders willing to take on construction risk for higher spreads (SOFR + 500-800 bps). These alternative sources often offer “stretch-senior” structures that reach up to 80% LTC for experienced sponsors.

Extended-stay brands are the “safe haven” of 2026. They account for 40% of all projects in the U.S. construction pipeline. Why? Because they have “lean operations” and “predictable income” that appeal to risk-averse lenders.

Small hotel construction loans interest rates for extended-stay properties are often more competitive because their operating margins (45%-55%) are significantly higher than full-service hotels. At HotelLoans.Net, we offer specialized programs for Marriott’s StudioRes, Hilton’s LivSmart, and other leading extended-stay flags.

The Cost to Finance a New Boutique Hotel

Developing a boutique hotel is a “multi-faceted revenue engine,” but it comes with a high price tag. The average cost to finance a new boutique hotel room in a 4-star category is approximately $318,200.

Unlike extended-stay models, boutique hotels are labor-intensive. Payroll can consume 30-40% of revenue, leaving margins tight. Lenders will look for:

High ancillary income from Food & Beverage (F&B).

A strong “Social Proof” factor (niche appeal).

Advanced technology integration to offset labor costs.

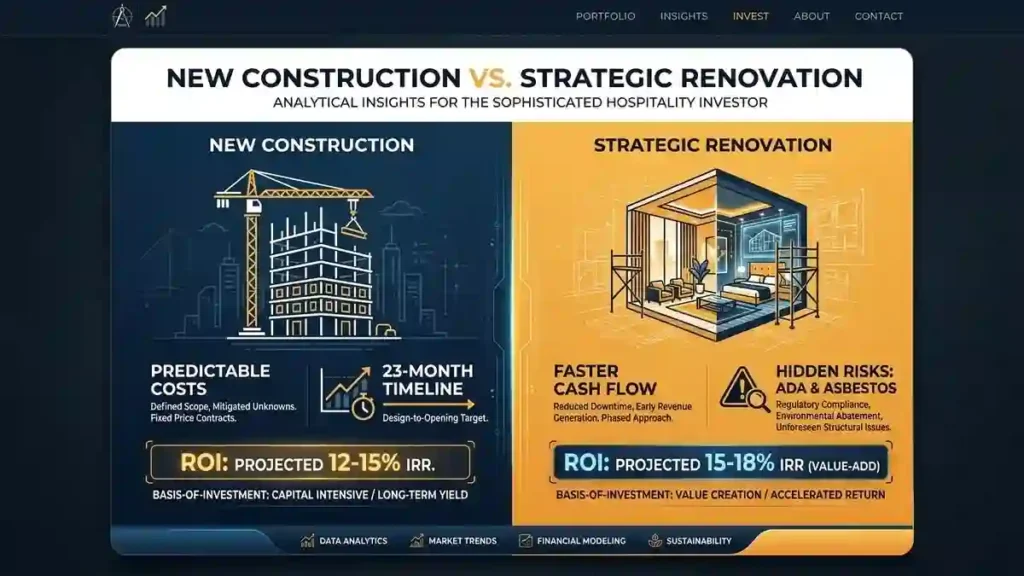

Hotel Renovation Financing vs. New Construction

Should you build new or renovate? In 2026, “brand conversions” have hit record highs, with 1,497 projects in the pipeline. Renovations (including “fix and flip” or “fix and rent”) offer a faster path to cash flow than the 23-month ground-up build time.

However, renovations often hide expensive surprises, such as ADA compliance gaps or asbestos. This is known as the “Cost Paradox.” At HotelLoans.Net, we provide “economic consulting services” to help you analyze the basis of your investment. If the “stressed case” model of a renovation doesn’t work, we’ll help you pivot to a new build strategy.

DSCR and No-Doc Loans: The Investor’s Secret Weapon

For investors looking for hospitality investment property, Debt Service Coverage Ratio (DSCR) loans are the preferred choice. These loans focus on the property’s ability to generate cash flow rather than your personal income.

In 2026, lenders typically require a Global DSCR of 1.25x or greater.

DSCR = {Net Operating Income (NOI)}/{Annual Debt Service}

If your “motel investment property” or “vacation investment property” meets this threshold, you can secure “lite-doc” or “no-doc” financing, allowing for rapid portfolio scaling.

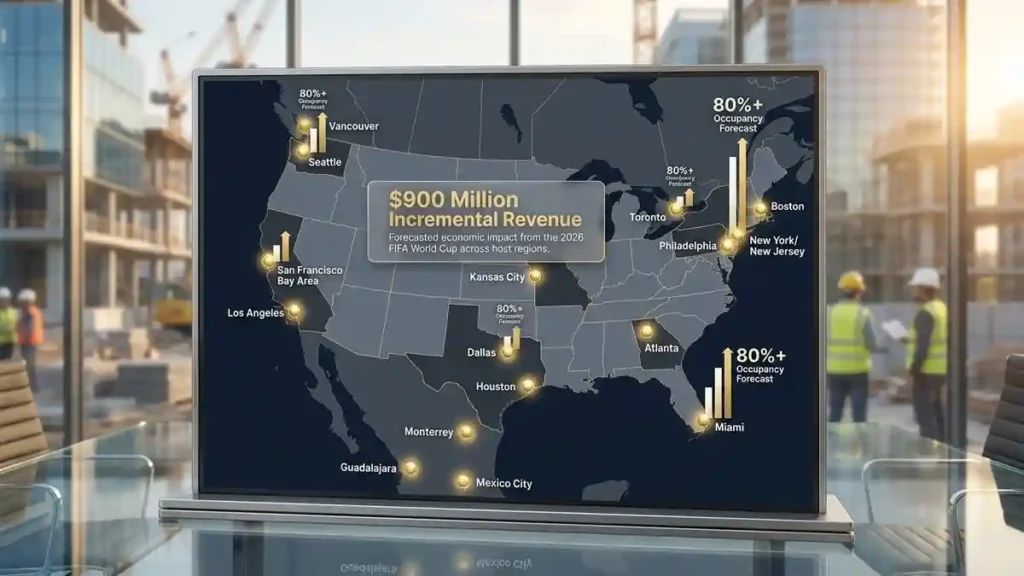

Will the 2026 World Cup Save Your ROI?

One major “push factor” for hotel investment in the USA is the 2026 FIFA World Cup. This event is expected to generate nearly $900 million in incremental hotel revenue.

In host cities like New York, Seattle, and Los Angeles, June 2026 occupancy is expected to top 80%, leading to “sharply elevated ADR”. Lenders are currently prioritizing “construction-to-permanent loans” in these markets to capture this one-time revenue surge and the subsequent long-term demand growth.

While direct government grants for hotel construction are rare, several federal programs function similarly:

USDA OneRD B&I Loans: Provides government guarantees of up to 80% for hotels in rural areas (populations under 50,000).

Historic Tax Credits (HTCs): Can be combined with bridge loans to renovate landmark properties.

C-PACE Financing: Offers low-cost, long-term funding for energy-efficient upgrades, which is now considered a “must-have” by 2026 lenders.

The Psychology of Property Investment: Managing “Pain and Pleasure”

Successful investing requires a balance of pragmatism and emotion. Many investors suffer from “Social Proof” (herd behavior), flocking to oversupplied markets like Nashville or Austin.

The Pain: Rising labor costs (up 22% since 2019) and stricter underwriting.

The Pleasure: Record-high ADRs and the ability to “build through the trough” to meet the 2027-2028 rebound.

At HotelLoans.Net, we help you navigate these psychological triggers. We view real estate investment as a marathon, not a sprint.

Exclusive Referral Programs for Hospitality Real Estate Brokers

We don’t just work with investors; we empower “hospitality real estate brokers.” Whether you are experienced or “new to the industry,” our platform provides a “super broker” back-end to handle your complex deals.

Exclusive Program: Dedicated white-label consulting for high-volume brokers.

Non-Exclusive Program: Perfect for general brokers who encounter occasional “restaurant investment property” or “recreation investment property” deals.

Broker Advice: We provide the financial data you need to close more deals, including how to read an STR report and calculate a “RevPAR Index”.

Why Do Experienced Brokers Choose Table Lending?

Table lending allows for a seamless, single-point-of-contact experience. We provide the initial funding at the closing table using our own capital or pre-arranged credit lines. This reduces “closing friction” and ensures your clients get their keys faster. In a market where “uncertainty is what kills deals,” the ability to “table fund” is a massive competitive advantage.

The 2026 macroeconomic environment is defined by “improving confidence despite continuing cost and labor pressures”. While non-residential buildings will see a 2.0% decline before returning to growth, the “flight to quality” means the best-positioned assets will always find capital.

Oxford Economics and Harvard researchers emphasize that productivity is the primary margin lever for 2026. Developers who integrate automation and “invisible concierge” technology will be the most attractive to conservative commercial lenders.

Conclusion: Partnering with HotelLoans.Net for Success

The journey of hotel construction financing is complex, but you don’t have to walk it alone. With 30 years of experience, a network of 200 private lenders, and 75 loan options, HotelLoans.Net is the definitive capital partner for hospitality real estate.

Whether you are seeking an “SBA 504 loan” for an extended-stay hotel, a “bridge loan” for a luxury renovation, or “USDA financing” for a rural resort, we have the tools to unlock your success. As the industry moves toward the 2027 recovery, the winners will be those who bring “Discipline and Certainty” to the table today.

Contact HotelLoans.Net today to start your underwriting process.

FAQs

Is a high credit score always required?

Yes, most lenders require a personal score of at least 680. However, HotelLoans.Net can often facilitate approvals for scores as low as 640 if your property demonstrates a strong debt service coverage ratio and significant post-closing liquidity reserves.

Can passive investors obtain SBA construction loans?

No, SBA financing is strictly intended for owner-operators who actively manage the business. Passive real estate investment structures do not qualify; however, our private lender network offers 75 alternative loan options specifically designed for non-operating hospitality real estate investors.

Can I finance land and construction together?

Yes, our platform provides comprehensive construction-to-permanent loans that cover land acquisition, permitting, and hard build costs in a single closing. This hybrid solution eliminates future refinancing risks and allows you to lock in competitive fixed rates before groundbreaking.

Does C-PACE fund energy-efficient hotel upgrades?

Yes, Commercial Property Assessed Clean Energy provides low-cost, long-term financing for sustainable infrastructure, such as HVAC and solar. This non-recourse capital is an excellent addition to your capital stack, improving property margins and meeting the strict 2026 environmental mandates.

Can a bridge loan close within one week?

Yes, bridge loans can close in as little as five days when time is critical. This speed is absolutely essential for securing “fix and flip” opportunities or preventing the loss of earnest money when traditional bank funding timelines fail.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.