The hospitality sector in 2026 is witnessing a remarkable resurgence, even as the global economy navigates a “K-shaped” recovery. For the modern investor, the quest how to get a loan to buy a hotel has become more than a simple transaction; it is a high-stakes chess match involving sophisticated capital stacks and evolving market dynamics. According to the American Hotel & Lodging Association (AHLA), hotel guest spending in the United States is projected to reach nearly $805 billion in 2026, a 1.7% increase over the previous year.

Despite this massive influx of guest capital, securing commercial real estate loans for hospitality properties remains a complex hurdle. Traditional banks have tightened their belts, leaving a void that agile, private-market platforms like HotelLoans.Net are now filling. With 30 years of underwriting experience and a network of over 200 private lenders, we provide the expertise needed to navigate 75 different loan options. Whether you are looking to purchase land, fund a ground-up construction, or execute a “fix and rent” strategy, understanding the nuances of the 2026 lending environment is your first step toward a successful acquisition.

The 2026 Hospitality Landscape: Opportunity Amidst Bifurcation

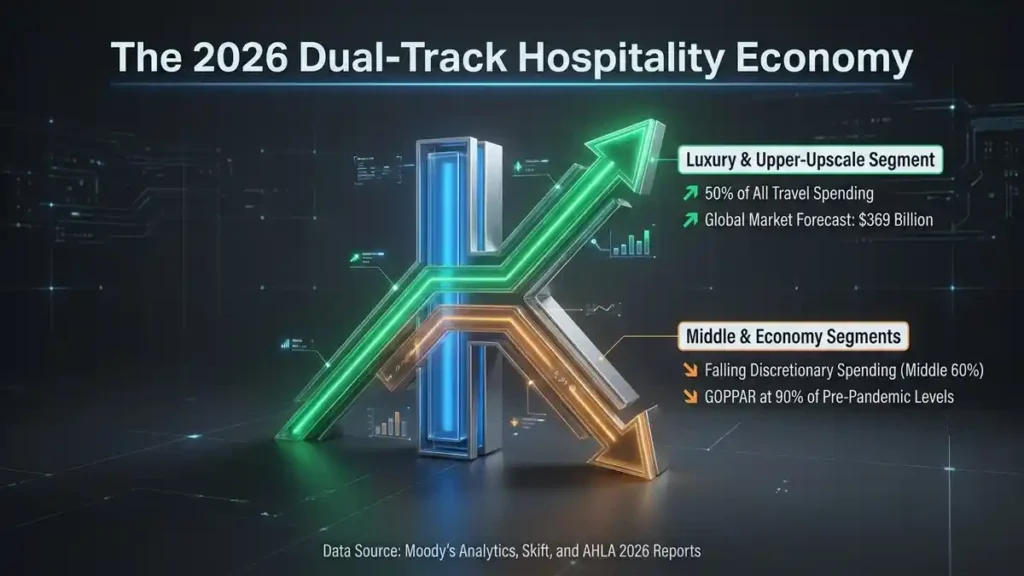

As we move through 2026, the travel industry is increasingly defined by economic bifurcation. Research from Moody’s Analytics indicates that the top 10% of earners now account for nearly 50% of all travel spending. This has created a surge in demand for luxury and upper-upscale segments. At the same time, middle-market properties must fight harder for discretionary spending. For investors, this means the “story” behind the property—its location, RevPAR Index, and target demographic—is more important than ever to underwriters.

Key Performance Statistics for 2026 Hospitality Investments

| Metric | Projection/Data | Source |

| U.S. Hotel Guest Spending | $805 Billion | AHLA |

| Global International Arrivals | 1.55 Billion | UN Tourism |

| Luxury Hotel Market Growth | $154B to $369B (by 2032) | Skift |

| Total U.S. Hotel Jobs | 2.2 Million | Oxford Economics |

| SBA 7(a) Max Loan Amount | $5 Million | SBA Guidelines |

| April 2026 Prime Rate | 6.75% | WSJ |

Major global events are also serving as catalysts for growth. Oxford Economics highlights that the 2026 World Cup and the upcoming 2028 Olympics are set to boost consumer spending and attract millions of visitors to major U.S. metropolitan areas. In fact, the World Cup alone is expected to boost U.S. Revenue Per Available Room (RevPAR) by nearly 2%, primarily through Average Daily Rate (ADR) growth in host cities such as Dallas, Kansas City, and New York.

Is the Traditional Bank Really Your Best Friend for Hotel Financing?

For decades, the local bank was the first stop for any real estate deal. However, in 2026, many traditional institutions are struggling with a $936 billion “debt wall” of maturing commercial mortgages. These banks are often more focused on managing their existing portfolios than on originating new, high-risk hospitality loans.

When you ask how to get a loan to buy a hotel, the answer often lies with a “super broker” or a correspondent lender. HotelLoans.Net operates in this space, acting as a bridge between your vision and private capital. Unlike a bank that might have one or two products, our platform offers 75 different loan types. Private lenders generally move faster than traditional banks, using automation to streamline the process while focusing on the asset’s performance rather than the borrower’s personal balance sheet.

| Feature | Traditional Bank | HotelLoans.Net (Private Network) |

| Loan Options | 1–3 Programs | 75+ Specialized Options |

| Speed of Funding | 90–180 Days | As fast as 30–60 Days |

| Underwriting Focus | Borrower Credit/History | Asset Performance & Future Potential |

| Flexibility | Rigid/Standardized | High/Customized |

| LTV Ratios | Often capped at 65% | Up to 80–90% (SBA/USDA) |

Master the SBA: The Gold Standard for Hotel Acquisitions

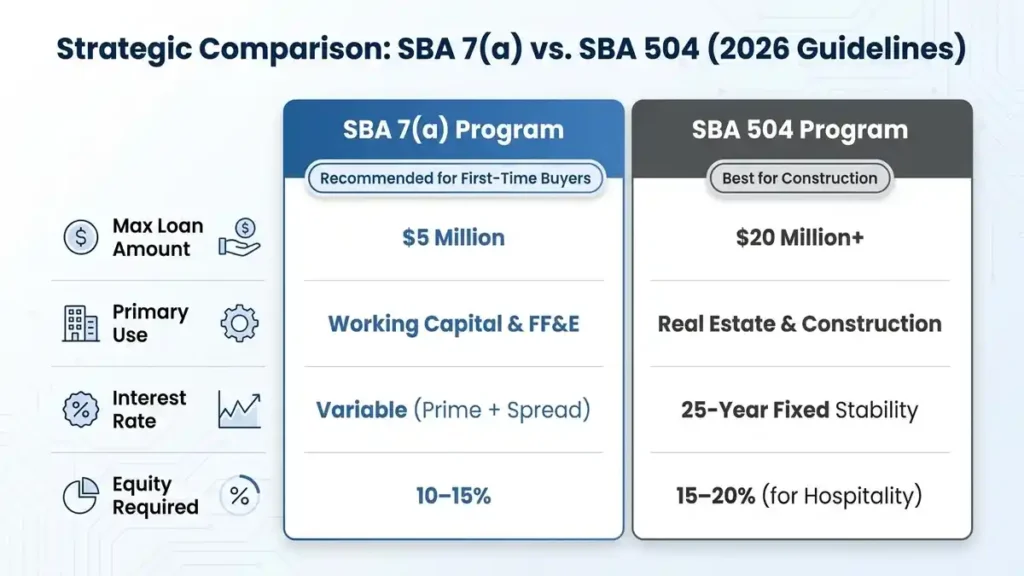

The Small Business Administration (SBA) remains the most powerful tool for investors asking how to get a loan to buy a hotel for the first time. In 2026, the SBA 7(a) and 504 programs have been refined to support the growing demand for hospitality assets.

SBA 7(a) Loans for Hotel Purchase

The SBA 7(a) program is the most popular choice for acquisitions up to $5 million. Its primary advantage is flexibility; it can cover the real estate, furniture, fixtures, equipment (FF&E), and even initial working capital. This makes it a preferred vehicle for how to finance a boutique hotel acquisition, where the business’s operational needs are just as critical as the property itself.

As of April 2026, with the Wall Street Journal Prime Rate at 6.75%, maximum variable rates for 7(a) loans typically range from 9.75% to 13.25%. While these rates reflect a higher benchmark environment, the 25-year amortization period ensures that your debt service remains manageable compared to shorter-term conventional products.

SBA 504 Loans: The Path to Long-Term Stability

For larger projects—specifically those ranging from $7 million to over $20 million—the SBA 504 loan is the superior option. This program is designed for “hard assets,” such as land purchases and major construction projects. The structure typically involves a bank providing 50% of the loan, a Certified Development Company (CDC) providing 40% (backed by the SBA), and the borrower contributing 10–20% equity.

The standout feature of the 504 loan in 2026 is the 25-year fixed interest rate on the CDC portion. This serves as a critical hedge against inflation. For “special purpose” properties like hotels, lenders often require 15% equity, which is still significantly lower than the 30% or 40% equity conventional lenders often demand.

Understanding the “Underwriting Language” of 2026

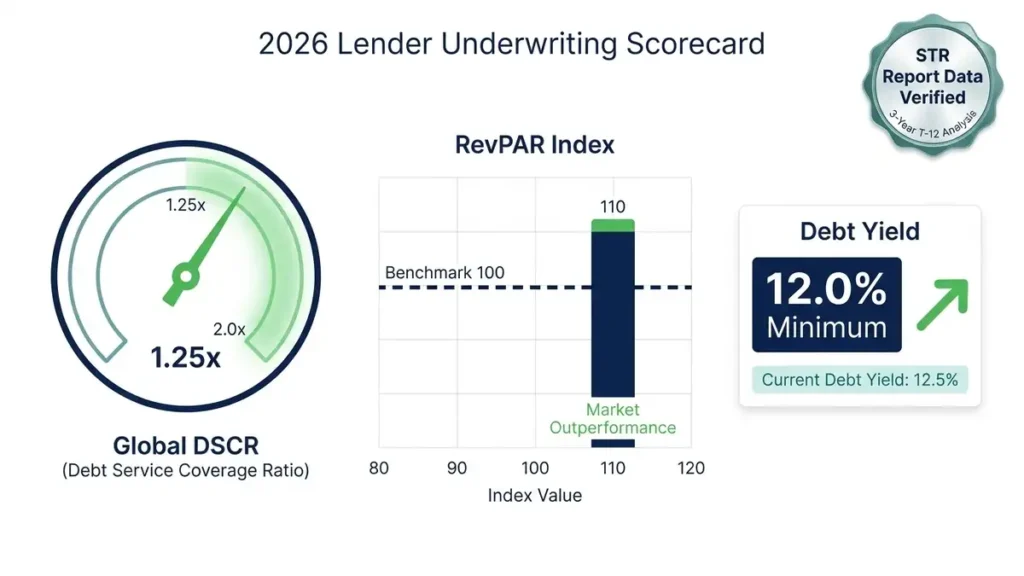

To qualify for a hotel mortgage, you must speak the language of the underwriter. In 2026, lenders aren’t just looking at your tax returns; they are looking at the property’s “heartbeat” through the STR Report.

- RevPAR Index: The “gold standard.” An index of 100 means the hotel is getting its fair share of the market. Lenders look for a 100+ index to ensure the property is competitive.

- Global DSCR: Most lenders require a Global Debt Service Coverage Ratio of 1.25x or greater. This means your net operating income (NOI) must be at least 125% of your annual debt obligations.

- Debt Yield: A newer metric gaining traction is the “Debt Yield,” which is the NOI divided by the loan amount. A 12% debt yield is often the minimum threshold for the best lenders for hotel financing.

Can You Actually Qualify for a Hotel Mortgage Without a Perfect Credit Score?

A common myth is that you need a 750+ credit score even to enter the hospitality game. While a strong score helps, it isn’t always the deal-breaker you might think. Many SBA lenders require a personal credit score of 680 or higher. Still, some programs can consider scores as low as 640 if the hotel demonstrates a high DSCR (1.35x+) and the borrower has significant liquidity.

At HotelLoans.Net, we also facilitate “no-doc” and “lite-doc” loans for experienced investors. These programs focus almost exclusively on the property’s income-producing potential and the borrower’s industry experience rather than on extensive personal financial documentation. If you are wondering what credit score do I need for a hotel loan, the answer is: the better the property performs, the more flexible the credit requirements become.

Specialized Strategies: From Boutique Acquisitions to “Fix and Flip”

The hospitality sector in 2026 is not a monolith. Different asset classes require different financial blueprints.

How to Finance a Boutique Hotel Acquisition

Boutique hotels are the darlings of the current “K-shaped” economy. Travelers are increasingly seeking “authentic” and “wellness-oriented” experiences. Financing these assets requires a lender who understands “lifestyle” value. Often, a combination of an SBA 7(a) loan for operational “soft costs” and a conventional bridge loan for the initial purchase is the winning strategy.

Bridge Loans for Hotel Acquisition: Speed as a Competitive Advantage

In a market where properties are moving fast, speed is your greatest asset. Bridge loans for hotel acquisition are short-term (6–36 months) solutions designed to “bridge” the gap between a quick close and permanent refinancing. These are essential for:

- Fix-and-Flip: Buying a distressed asset, renovating it, and selling it within 24 months.

- Stabilization: Buying a hotel with low occupancy, improving operations, and then refinancing into a lower-interest SBA loan once the RevPAR Index hits 100.

Advanced Loan Types for Diverse Portfolios: How to Get a Loan to Buy a Hotel

Beyond the standard SBA and bridge options, HotelLoans.Net offers a variety of specialized financing vehicles tailored to specific property types and locations.

- USDA B&I Loans: Ideal for hotels in rural areas (towns under 50,000 people). These offer high LTVs and long terms, helping revitalize rural economies.

- CMBS (Conduit) Loans: These are non-recourse loans in which the property itself is the sole collateral. They are perfect for stabilized, high-value assets in major cities.

- FHA Commercial & HUD Loans: These are typically used for long-term, permanent financing of assets that also serve a residential or community purpose, such as extended-stay hotels or hospitality adjacent to healthcare.

- DSCR Loans: These loans are “stated income” products in which lenders qualify the loan solely on the property’s cash flow, making them ideal for vacation rentals and smaller motel investments.

Is Hotel Owner Financing Just a Debt Trap in Disguise?

When looking at how to get a loan to buy a hotel, you may encounter “owner financing.” This is where the seller acts as the lender. While it can be a way to circumvent strict bank underwriting, it comes with the pros and cons of hotel owner financing.

- The Pros: Faster closing, lower down payment requirements, and no strict credit checks.

- The Cons: Often carries much higher interest rates, shorter “balloon” payments, and the risk of losing the property quickly if a payment is missed. For the strategic investor, owner financing should only be used as a “bridge” to a more permanent, stable financial product from a reputable lender.

The Financial Package: Preparing Your “Winning” Pitch

Regardless of the loan type, your success depends on the quality of your submission. Our 30 years of underwriting experience have shown us that a “clean” package moves through the system 3x faster. Your guide to hotel development loans or acquisition loans must include:

- A Robust Business Plan: Not just a vision, but a detailed analysis of your “comp set” (competitors) and your strategy for outperforming them.

- The STR Report: Showing at least 3 years of historical data for the subject property.

- Feasibility Study: Especially for new construction or major renovations, proving the market can support the new inventory.

- A Resume of Experience: Lenders want to know who is running the show. If you are new, you must identify a third-party management team with a proven track record.

The Strategic Partnership: Referrals and Consultancy

HotelLoans.Net is not just a lender; we are a financial consultancy. We recognize that the hospitality ecosystem relies on real estate brokers’ expertise. That is why we offer both exclusive and non-exclusive referral programs. Whether you are an experienced hospitality broker or new to the sector, our platform provides the leverage you need to close more deals.

We offer financial advice for those purchasing land for hospitality property, managing construction-to-permanent transitions, or executing “fix and hold” strategies. Our goal is to ensure a single bank’s rigid criteria never limit you. With 200+ lenders at your fingertips, you have the power to shop for the best lenders for hotel financing across the entire nation.

Final Thoughts: Securing Your Future in Hospitality

The year 2026 is a “readiness” year for the hospitality investor. With international tourist arrivals projected to exceed 1.55 billion and domestic travel remaining the primary engine of growth, the opportunities are vast. However, the days of easy credit are gone.

How to get a loan to buy a hotel now requires a sophisticated approach that balances the “K-shaped” market reality with the right financial vehicle. Whether it’s an SBA 504 loan for a high-value resort or a bridge loan for a quick motel flip, the right partner makes the difference.

Are you ready to move beyond the limitations of your local bank? At HotelLoans.Net, we don’t just find you a loan; we build your capital stack for long-term success. Let us put our 30 years of underwriting and our network of 200+ lenders to work for you. The first step to owning your next hotel starts with the right financial foundation.

FAQs

Does a manager’s resume affect my loan approval?

Yes. Lenders in 2026 will vet your general manager’s resume as strictly as your financial statements. Proven expertise in maintaining high profit margins and executing improvement plans significantly reduces risk, making operational depth essential for securing competitive hospitality financing.

Is the 2026 World Cup impacting hotel financing?

Yes. The 2026 World Cup is a major demand driver influencing underwriters. Lenders are more aggressive in host cities like Dallas and New York, projecting significant RevPAR growth. This global event makes specialized acquisition loans easier to justify for investors.

Can passive investors qualify for SBA hotel loans?

No. SBA hotel loans require the borrowing entity to be an owner-operator who actively manages the business. Passive real estate investment structures do not qualify for these programs, as government backing is specifically intended to support active small business operations.

Do unpermitted renovations block hotel loan funding?

Yes. Unpermitted changes can cause severe legal issues during due diligence, potentially halting your funding. Lenders require all previous alterations to be properly authorized to ensure the property is compliant with local building codes and eligible for necessary accommodation licenses.

Does using a virtual credit card improve loan eligibility?

Yes. Adopting automated virtual credit card management improves your hotel’s financial transparency and reconciliation accuracy. Lenders view this digital readiness favorably, as it enhances cash flow visibility and demonstrates a strategic focus on protecting margins against rising operational costs.