The hospitality sector in 2026 is no longer a game for the timid. As we navigate a domestic market valued at a staggering $1.08 trillion, the stakes have never been higher for developers and investors. We are currently staring down a “maturity wall” where approximately $936 billion in commercial real estate loans are scheduled to mature this year alone. This massive wave of refinancing pressure means that finding the Right Lender for Hotel Projects is no longer just a checkbox on a to-do list—it is the difference between asset appreciation and a forced sale.

At HotelLoans.Net, we have 30 years of underwriting experience. We have seen cycles come and go, but the 2026 paradigm is unique. With a platform that connects you to 200 private lenders, investors, and 75 different loan options, we know that “settling” for a suboptimal term sheet can cost you millions over the life of an asset. Whether you are looking for the best hotel construction lenders 2026 or trying to secure financing for boutique hotel projects, the following seven steps will ensure you partner with capital that understands your vision.

Step 1: Is Your Property Type Secretly a Lender’s Red Flag?

In the current market, not all keys are created equal. Lenders in 2026 have shifted from a “flight to value” to a “flight to quality”. Before you even pick up the phone, you must understand how a potential financier classifies your asset.

The Dominance of Select-Service and Extended-Stay

The “darling” of the 2026 lending world remains the select-service and extended-stay models. These properties, such as Hampton Inn or Residence Inn, are favored because they operate with lean staffing models—a critical advantage given that the sector remains short by approximately 190,000 positions. Lenders view these as “recession-resilient” because they maintain higher profit margins even when RevPAR growth is modest, which Hotel Investment Today projects will hover between 0.5% and 1.0% this year.

Interestingly, financing tips for luxury hotel projects often point toward “lifestyle” hotels in university markets. Research from the Yale School of Management highlights that campus-adjacent housing and hospitality remain high-demand sectors despite broader economic headwinds. Assets like “Study Hotels” thrive by tapping into the cyclical, recession-proof demand of academic calendars, making them a top choice for commercial real estate lenders specializing in hospitality.

Asset Class

Lender Appetite (2026)

Primary Driver

Select-Service

Very High

Predictable cash flow, 35–40% EBITDA margins

Extended-Stay

Very High

Demand from remote workers and relocations

Boutique/Lifestyle

High

Authentic experiences, commanded ADR premiums

Independent

Moderate

Requires high-quality “soft brand” affiliation

Step 2: Are Your Debt Yields Low Enough to Kill Your Deal?

Understanding the math of 2026 is vital. Lenders are no longer moved by “pro forma” dreams; they want hard data. If you don’t know your debt service coverage ratio for hotel loans, you aren’t ready for the boardroom.

The New Benchmark for Underwriting

While the global hospitality market has grown to $5.12 trillion, the cost of debt has also risen. Construction debt currently sits between 10% and 12%, forcing lenders to be more selective. The “Gold Standard” for performance is the RevPAR Index, where an index of 100 signifies you are capturing your “fair share” of the market.

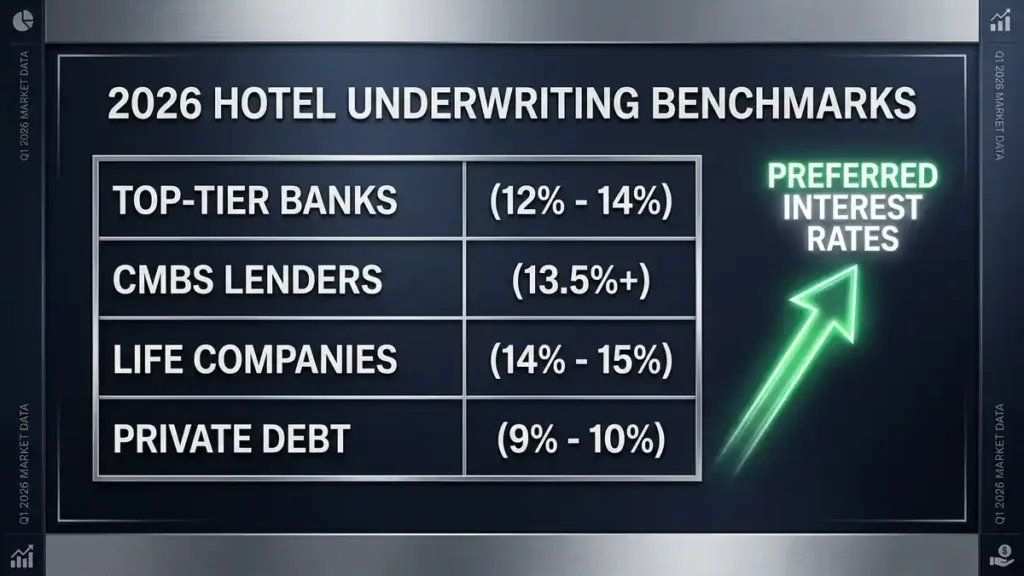

However, lenders are prioritizing “Debt Yield” above all else. A debt yield of 12% to 14.5% is currently required to secure the most competitive interest rates (often in the 6% to 7% range). If your debt yield falls below 10.5%, you may be pushed toward “rescue capital” or bridge loans with rates above 10%.

The Global Cash Flow Mandate

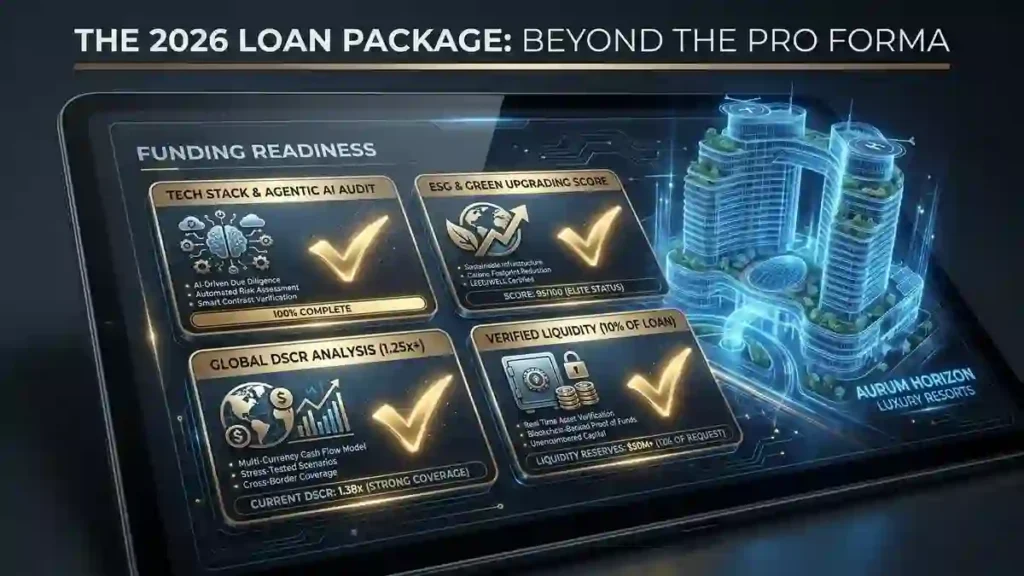

A significant trend noted by Investopedia and Forbes is the shift toward “Global Cash Flow” analysis. Lenders are no longer just looking at the subject property; they are auditing your entire financial ecosystem. If your other business ventures are struggling, even a high-performing hotel might decline. Most lenders now require a Global DSCR of at least 1.25x to provide a 25% “cushion” against market volatility.

Step 3: Comparing Hotel Financing Options: Conventional vs. Private

One of the biggest challenges finding capital for new hotel projects is choosing the right source. In 2026, the gap between traditional banks and private debt funds widened.

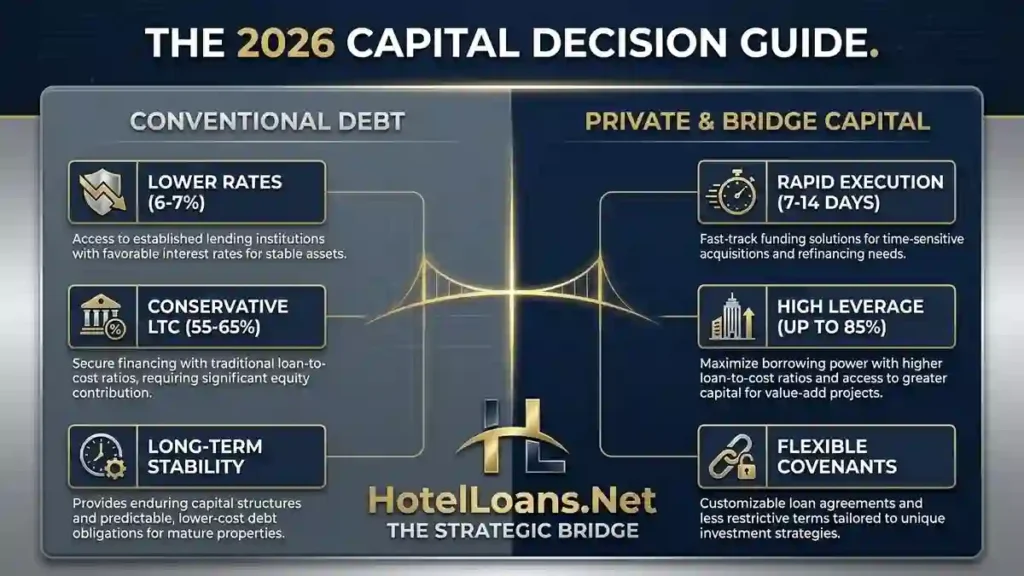

Conventional Bank and Life Company Debt

Traditional players like Bank OZK and M&T Bank are active but remain focused on “top-tier” borrowers with a proven track record. Life insurance companies, such as New York Life and MetLife, are preferred for permanent financing of stabilized assets, typically offering 55% to 65% leverage.

The Rise of Private Lenders for Hotel Acquisition Loans

For transitional assets or hotel renovation loan lenders experience, private debt funds and “super brokers” like HotelLoans.Net are essential. Private lenders are often able to move faster than traditional banks—a major advantage in a year where “speed is a competitive advantage”. While private capital is pricier (often SOFR + 350 to 600 basis points), it offers higher leverage, sometimes up to 85% for the right project.

Step 4: Mastering the SBA Hotel Loan Requirements and Process

For many mid-scale developers, the SBA and USDA programs are the most powerful tools in the shed. These government-backed options offer longer terms and lower down payments than conventional debt.

The 2026 SBA 504 and 7(a) Updates

If you are finding the Right Lender for Hotel Projects, you must be aware of the 2026 regulatory shift. As of 1 March 2026, the SBA now requires that 100% of the applicant business be owned by U.S. Citizens or Nationals. Furthermore, for 7(a) small loans, a DSCR of at least 1.1:1 is now mandatory.

The SBA 504 program remains the best path to secure financing for boutique hotel construction, as it offers a 25-year fixed rate on the 40% CDC portion of the loan. This serves as a vital hedge against inflation in an environment where The Economist warns of renewed inflationary pressures due to global energy volatility.

USDA B&I: The Rural Opportunity

For projects in areas with populations under 50,000, the USDA B&I program has increased its guarantee to 85% for loans under $5 million in 2026. This is a massive win for recreation investment property and vacation investment property owners in secondary markets, particularly in states like Florida, which is seeing a 6.03% CAGR in the hospitality sector.

Step 5: Is Your General Contractor Secretly Costing You the Loan?

A common pitfall in what to look for in a hotel construction loan agreement is the lack of “hard” documentation. Lenders in 2026 have zero tolerance for “back-of-the-napkin” math.

The Construction Loan Checklist

To satisfy best hotel construction lenders 2026, your loan package must include:

Firm Fixed-Price Contracts: Estimates will lead to an immediate decline.

Contractor Vetting: Lenders require your general contractor’s license, resume, and references.

Feasibility Studies: A third-party validation of your market demand and competitive set is non-negotiable.

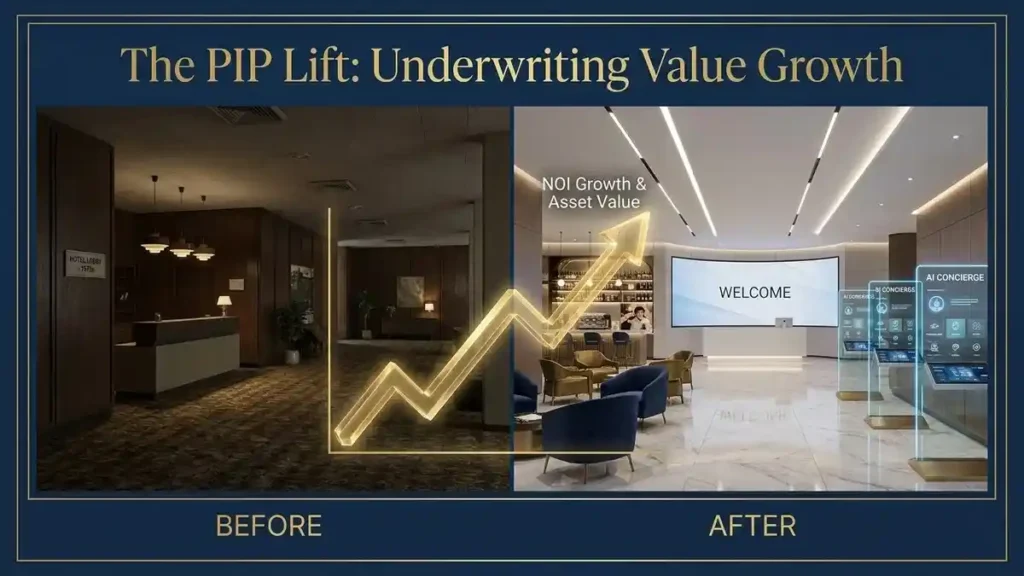

PIP documentation: If you are acquiring a flagged property, the lender will analyze the “PIP Lift”—the ROI generated by mandated renovations.

Step 6: Specialized Strategies for Luxury and Boutique Assets

As travelers become “harder to impress,” the luxury and boutique segments are pivoting toward personalized experiences. Forbes reports that 65% of travelers now choose destinations based on unique experiences rather than brand name alone.

Financing Luxury Hotel Projects Tips

When securing financing for boutique hotel or luxury assets, your “story” is your most valuable asset. Lenders want to see how you are using “agentic AI” to reduce friction in the guest journey—from predictive personalization to real-time translation systems. Harvard Business Review notes that in the modern market, “integration is where deals live or die”. You must prove that your operational model can handle the high per-key costs of luxury, which HVS notes can range from $350K to over $500K per key for new builds.

A guide to hotel financing for first-time developers often misses the importance of “Special Purpose” classification. Hotels are unique because they are businesses tied to real estate. This means your management track record is just as important as the building’s location. Lenders are targeting “proven operators” and will often require post-closing liquidity of at least 10% of the loan amount.

Step 7: How to Prepare a Loan Package for Hotel Investors

The final step in finding the Right Lender for Hotel Projects is executing the pitch. At HotelLoans.Net, we serve as your “super broker,” refining your assumptions and stress-testing your business plan before it ever reaches a lender’s desk.

The Digital Underwriting Edge

In 2026, lenders will use AI-driven technology to shop deals and verify data points. To stand out, your package must be “institutional-grade.” This means having a clear “tech stack” that includes modern property management systems and pricing tools that automatically adjust rates.

The Importance of Execution Certainty

With 30% of all hotel mortgages maturing this year, “execution certainty” is the most valuable currency in the market. You need a partner who won’t change terms at the 11th hour. Our platform provides that certainty by connecting you to 200 vetted private lenders who understand the nuances of hospitality and hotel investment properties.

Conclusion: Take Command of Your Capital Stack

The “maturity wall” of 2026 is either a threat or an opportunity, depending on your preparation. By following these seven steps, you move from being a “seeker” of capital to a “selector” of partners.

Whether you are looking to secure financing for boutique hotel acquisitions, need help with SBA hotel loan requirements and process, or are searching for criteria for choosing a hotel development lender, HotelLoans.Net is here to provide the 30 years of underwriting experience you need. We specialize exclusively in real estate investment properties—we don’t run your business, we fund your growth.

Don’t settle for the first rate you are offered. Explore over 75 loan options and find the perfect fit for your next motel investment property, restaurant investment property, or construction for hospitality property. In a market defined by a “flight to quality,” make sure your capital is as high-quality as your asset.

FAQs

How long does hotel loan closing take?

Yes, most hotel loans now close within 60 to 90 days if third-party reports are completed promptly. Experienced lenders use modern digital platforms to accelerate traditionally slow, manual workflows, thereby improving current efficiency benchmarks.

Can SBA loans cover hotel renovation costs?

Yes, the SBA 7(a) program specifically allows for 100% financing of brand-mandated Property Improvement Plans. This includes guestroom updates and lobby modernization, helping owners improve their RevPAR index without depleting their current operational liquidity reserves.

Is a 25% down payment possible for hotels?

Yes, government-backed programs like the SBA 7(a) often require only a 10% equity injection for experienced operators. While conventional lenders typically demand 35% to 40%, specialized options help developers preserve capital for technology-driven operational enhancements.

Do SBA loans require full U.S. citizenship?

Yes, as of March 2026, the SBA mandates that 100% of the applicant business must be owned by U.S. Citizens or Nationals. This shift excludes permanent residents, making ownership structure verification a critical step for all potential borrowers.

Can I finance hotel technology upgrades separately?

Yes, most hospitality owners utilize commercial and industrial loans or business term loans for technology projects. These funds cover modern property management systems and mobile apps, which are now essential for maintaining competitive daily rates and operational margins.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.