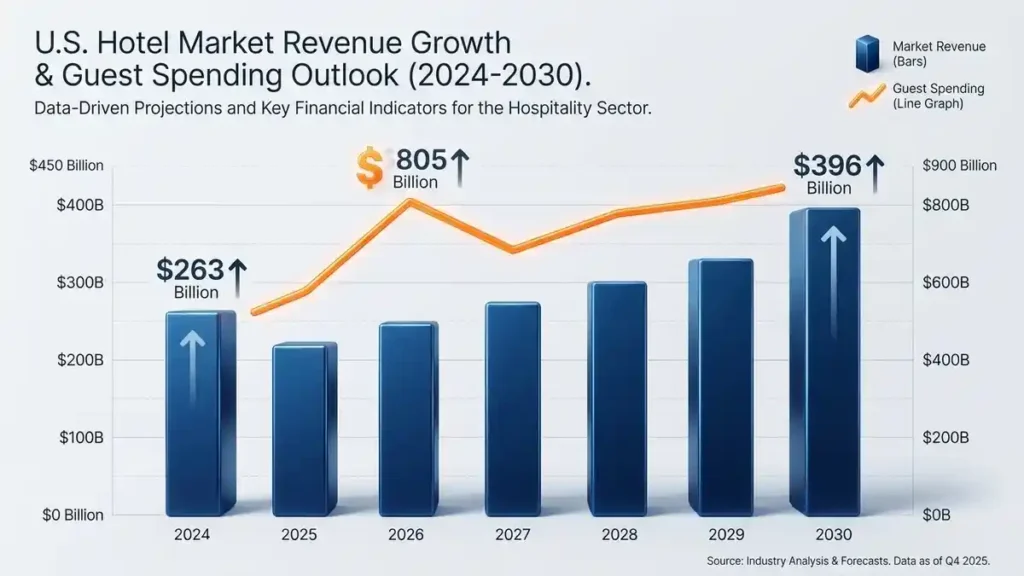

The hospitality market is changing fast. Experts expect total guest spending in the United States to reach nearly $805 billion this year. In fact, hotel market revenue could reach $396 billion by 2030. This growth creates a significant opportunity for both new and experienced investors. Buying a motel is a big step. Many people consider SBA loans for motel purchases their first option.

HotelLoans.Net understands this sector deeply. They bring 30 years of underwriting skills to the table. As a correspondent and table lender, they act as a super broker. They connect you to 75 different loan options. They focus only on the real estate side. They help you buy, build, or fix the property. They do not run the business for you. This guide shows you how to use their expertise to get the funding you need.

Step 1: Can you meet the eligibility requirements for SBA loans to buy a motel?

Before you look for a property, you must look at your own finances. Lenders want to know if you can pay the money back. They use specific rules to decide this. One major part is your net worth. To qualify for most programs, your business must have a tangible net worth of less than $15 million or $20 million. Your average net income for the last two years should also be under $5 million or $6.5 million after taxes.

What credit score is required for an SBA motel loan approval?

Your personal credit score is the first thing a lender checks. Many people ask, ” What is the minimum credit score for an SBA motel loan? Most lenders require a score of 680 or higher. Some might go as low as 640 if you have a lot of cash in the bank. They also look at your business credit score. A good PAYDEX score is between 80 and 100. If your score is under 50, it could be a red flag for the bank.

Experience matters as much as money. Lenders like to see that you have managed a hotel or motel before. Usually, they want at least two years of management experience. If you are new to the industry, do not worry. You can hire a professional management company. This helps the lender feel safe. HotelLoans.Net can advise you on how to structure your team to meet the eligibility requirements for SBA loans to buy motels.

Eligibility Factor

General Requirement

Personal Credit Score

680+ preferred

Business Net Worth

Under $15M – $20M

Management Experience

2+ years or professional manager

Post-Closing Cash

10% of loan amount

Step 2: SBA loans for motel purchase: Which program fits your vision?

There is no single “best” loan. It depends on what you need. You might want cash for daily costs. Or you might want a fixed rate for 25 years. This is where you pick the best SBA loan programs for hotel purchase.

SBA 7a loan requirements for motel investment

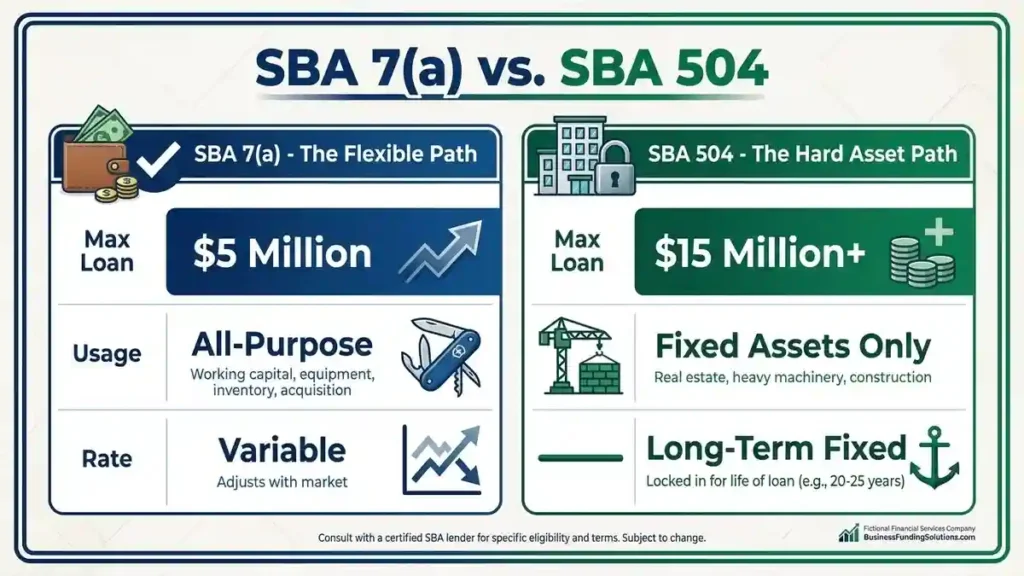

The SBA 7(a) is the most flexible choice. It is great for deals under $5 million. You can use the money for almost anything. This includes buying the land, fixing rooms, or paying staff. One of the main SBA 7 (a) loan requirements for motel investment is that the business must be for-profit and located in the U.S. This program often covers the “full stack” of costs in a single loan.

SBA 504 loan for existing motel purchase

The SBA 504 is better for buying large assets. If you are doing an SBA 504 loan for the purchase of an existing motel, the structure is unique. A private bank covers 50% of the cost. A non-profit company (CDC) covers 40%. You only put down 10%. This program gives you a fixed interest rate for up to 25 years. This protects you if interest rates go up later. However, you cannot use this money for working capital or inventory.

Step 3: Is it worth comparing SBA loans to conventional motel financing?

Many buyers wonder if they should get a regular bank loan. When comparing SBA loans to conventional motel financing, the difference usually comes down to the down payment. Regular commercial loans often ask for 20% to 25% down. They also have shorter repayment times, like 10 or 15 years.

Pros and cons of using an SBA loan for a motel

There are clear pros and cons of using an SBA loan for motel acquisition.

The Pros:

You put less money down (as low as 10%).

You have more time to pay it back (up to 25 years).

Interest rates are often lower than those for hard money loans.

HotelLoans.Net helps you weigh these factors. They review your specific project to see whether a conventional loan might be faster or better for your situation.

Step 4: What are the SBA loan interest rates for buying a motel today?

Money costs money. You need to know how much your monthly payment will be. Currently, SBA loan interest rates for motel purchases are tied to the Prime Rate. The Prime Rate is currently around 6.75%. For a 7(a) loan over $350,000, the bank cannot charge more than Prime + 3.0%.

Financing a motel with an SBA loan down payment

Getting the cash for a down payment is often the hardest part. When financing a motel with an SBA loan, you typically need a down payment of 10% to 15% of the total cost. If you are an experienced owner, some lenders might let you go lower. If you are a first-time buyer or buying an independent motel, you might need a 20% down payment.

SBA loan limits for motel property acquisition

How much can you borrow? The SBA loan limits for motel property acquisition vary by program.

SBA 7(a): Maximum is $5 million.

SBA 504: The CDC part is $5 million (or $5.5 million for green energy).

Total Project: With a 504 loan, the total project can be over $15 million because the bank portion has no cap.

If you use the “Green” 504 program, you can borrow up to $16.5 million over the life of your business. This is perfect for investors with multiple properties.

Loan Program

Max Loan Amount

Interest Rate Type

SBA 7(a)

$5 Million

Variable (usually)

SBA 504

$5.5 Million (CDC part)

Fixed

Conventional

Varies by lender

Fixed or Variable

Step 5: Do you have the SBA loan approval guide for motel buyers?

Getting approved is about more than just credit. It is about the property’s performance. A good guide to SBA loan approval for motel buyers must mention the Debt Service Coverage Ratio (DSCR). Lenders want to see a DSCR of at least 1.25x. This means the motel makes 25% more profit than it needs to pay the mortgage.

Lenders use STR reports to check the motel’s health. They look at:

Occupancy: Is the motel at least 60% full?.

ADR (Average Daily Rate): How much do guests pay per night?.

RevPAR (Revenue Per Available Room): The gold standard metric.

RevPAR Index: Does the motel do better than the competition nearby?.

RevPAR = ADR \times Occupancy Percentage

If you have these numbers ready, your application will move much faster. HotelLoans.Net uses its underwriting background to help you clean up these numbers before the bank sees them.

Step 6: How to apply for an SBA loan for motel acquisition without stress?

Paperwork is the biggest hurdle. Knowing how to apply for an SBA loan for a motel acquisition starts with a solid plan. You need a business plan that shows income for the next 3 to 5 years. You also need to show how you will handle a Property Improvement Plan (PIP). Brand-name hotels often require you to fix the lobby or rooms when you buy. Lenders want to see a clear budget for this.

You will need many files. Here are the most important documents needed for the SBA loan motel purchase:

Tax returns for the last three years (personal and business).

Profit and Loss (P&L) statements.

A debt schedule for the business.

Personal financial statements.

The purchase agreement for the motel.

A resume showing your hospitality experience.

STR reports or internal occupancy data for the last 12 months.

Having these organized in a digital folder can save you weeks. Banks hate waiting for missing papers.

Step 7: Will the challenges of getting an SBA loan for a motel stop you?

It is not always easy. There are many challenges to getting an SBA loan for a motel today. For example, motels have a high default rate of about 15.4%. Because of this, banks are very careful. They might ask for a Phase I Environmental report to make sure the land is clean. They might also worry about the local market if a new hotel is being built down the street.

Success stories: SBA loans for motel owners

Despite the hurdles, motel owners share many success stories about SBA loans. One experienced hotelier bought an unbranded motel in Billings, Montana, for $1.5 million. She used an SBA 7(a) loan to cover the purchase and the renovations. By fixing up the rooms and marketing to tourists, she turned it into a high-profit property. Another owner used the 504 Debt Refi program to switch from a high variable rate to a low fixed rate. This saved them thousands of dollars every month.

Final Thoughts on Motel Financing

The hospitality world offers great rewards for those who prepare. Working with a consultant like HotelLoans.Net gives you access to a massive network of 75 loan options. Their 30 years of underwriting experience ensure your application is strong from day one. Whether you need a bridge loan to close fast or a 25-year fixed rate to grow slow, they have the tools.

Securing SBA loans for motel purchase requires a good plan, clean credit, and the right team. If you are ready to enter the hospitality sector or expand your portfolio, start by gathering your financial records. The market is waiting, and with guest spending rising every year, the timing is perfect. Reach out to a specialist today to find the 75 loan options that fit your next investment.

FAQs

Do I need life insurance for an SBA loan?

Yes. Lenders use life insurance as collateral to protect their investment. If a borrower passes away, the policy pays off the debt. This keeps the business running. It also stops the financial burden from falling on your family members.

Can green card holders get SBA motel loans?

No. A new rule started on 1 March 2026. Now, all owners must be U.S. citizens or nationals. This applies to the 7(a) and 504 programs. The goal is to prioritize American citizens who are building new local businesses.

Can I use 401 (k) funds for down payments?

Yes. You can use a program called ROBS to invest your retirement funds. This lets you access your money without paying tax penalties. It increases your buying power. It also helps you avoid taking on extra debt for your purchase.

Can I switch my 7a loan to a fixed rate?

Yes. A new SBA rule allows you to refinance a floating-rate 7(a) loan into a fixed-rate 504 loan. This move locks in your interest rate. It protects you from future market changes. It also helps lower your monthly payments.

Does an SBA 7a loan have early fees?

Yes. For loans lasting 15 years or more, fees apply if you pay early. You pay 5% in the first year and 3% in the second. By the third year, it drops to 1%. After that, you can pay as you please.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.