The hotel building market in 2026 is moving fast. Experts call this time a “jobless boom.” The U.S. economy is growing at a rate of 2.0% to 2.8% right now. Travel is growing even faster. The World Travel & Tourism Council says this sector will grow 1.5 times faster than the rest of the economy over the next ten years. This is good news for you. But building a hotel is not simple. You need a solid plan to find the right money. This guide shows you how to get hotel construction loans in today’s tricky market.

Lenders are back in the game at full speed. This comes after a quiet 2025. Many loans are hitting their due dates soon. We call this the $936 billion “debt wall”. Banks have to move this money around. They want to lend, but they are very picky. They don’t just look at the building anymore. They look at you. They look at your team. They look at how your project handles high costs.

Material prices for building have jumped 42% since 2030. Labor costs are up 24% as well. You must show a lender that your project can survive these price hikes. At HotelLoans.Net, we have seen these cycles for 30 years. We act as a correspondent and table lender. We offer 75 different loan options. We know what underwriters want to see before they say yes.

How to get hotel construction loans in a shifting market

Success starts with knowing your numbers. You cannot guess. You need a “lender-ready” package. This includes a clear budget. It needs a real timeline. You also need a brand approval letter if you want a big name like Hilton or Marriott. Lenders want to see that the market actually needs your hotel. They will look at STR reports. These reports show how nearby hotels are doing. They track occupancy and room rates.

What credit score is needed for hotel construction loan?

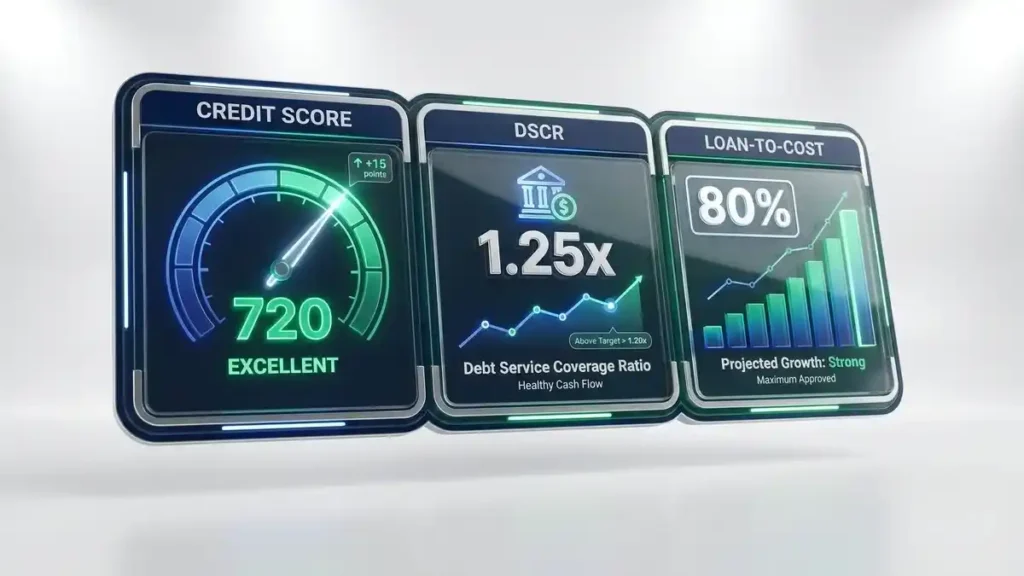

This is the first question most people ask. Your personal history matters a lot. Most lenders require a score of 680 or higher. A high score shows you handle debt well. If your score is lower, you might still get a loan. But you will need a bigger down payment for hotel construction loan to make up for it.

Some private lenders are more flexible. They may consider a score of 640 if the hotel project is very strong. However, the best hotel construction loan interest rates are currently reserved for people with top-tier credit. In May 2026, bank rates are sitting between 7.57% and 8.57%. If your credit is perfect, you get the lower end of that range.

Performance Benchmarks for 2026

Metric

Target Level

Why It Matters

Credit Score

680+

Proves financial trust.

DSCR

1.25x

Shows the hotel can pay its own debt.

LTC (Loan to Cost)

65-80%

Shows how much the bank will cover.

Equity Injection

20-35%

Your “skin in the game.”

Hotel construction loan requirements for new build

Building from the ground up is high risk for a bank. They need to know the building will actually get finished. You must have a fixed-price construction contract. This is also called a Guaranteed Maximum Price (GMP) contract. It stops the builder from asking for more money if prices go up.

You also need a feasibility study. This is a deep dive into the local area. It proves that guests will show up once you open the doors. Lenders also require a contingency reserve. This is extra cash held in the bank, usually 5% to 10% of the build cost. It pays for surprises underground or weather delays.

Government-backed hotel construction loans

Government programs are a great path for many. They often allow for lower down payments. The Small Business Administration (SBA) and the USDA offer these deals. They will become much more efficient in 2026. The SBA guaranteed $45 billion in loans in 2025 alone.

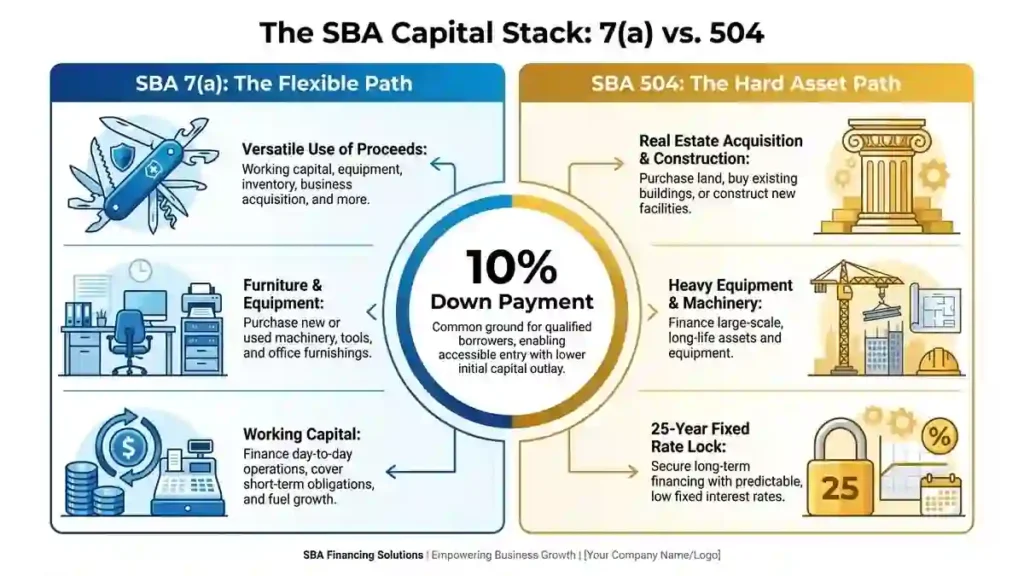

SBA 7a loan for hotel construction

The 7a program is very flexible. It is the most popular choice for hotels. You can use it to buy land, build the structure, and even buy furniture. The maximum loan is $5 million. One big plus is the long repayment time. You get up to 25 years to pay it back for real estate. This keeps your monthly payments lower.

SBA 504: The Fixed-Rate Path

The 504 loan is for big, long-term assets. It has two parts. A bank covers 50%. A Certified Development Company (CDC) covers 40%. You put down 10%. The 40% part has a fixed rate for 25 years. In May 2026, that rate is around 5.61%. This protects you if interest rates go up later.

If you are building in a small town, look at the USDA Business & Industry (B&I) program. It is for towns with fewer than 50,000 people. For 2026, the USDA guarantees 85% of loans under $5 million. This makes banks feel safe lending in rural markets.

How to qualify for boutique hotel construction financing?

Boutique hotels are very popular in 2026. Travelers want unique stays, not the same old rooms. But banks see these as higher risk. They don’t have a big brand to help them. To get this money, you need to prove you have a “management muscle.”

Lenders will review your General Manager’s resume as closely as they will yours. You must show a marketing plan that works. Since you don’t have a big brand website, you must prove you can find guests online. You will likely need a higher down payment for an independent project. Expect to put down 25% to 35%.

Financing a small independent hotel construction project

Small projects face unique hurdles. Big banks often ignore small loans. You should look at small local banks or credit unions. A recent report found that small banks approve 57% of their loan applications. That is higher than big national banks.

Another option is a “lite-doc” loan. These are great if you don’t have years of tax returns. You might only need to show 12 to 24 months of bank statements. The rates are a bit higher, but the process is much faster.

How to get a hotel construction loan with no experience?

Can you build a hotel if you have never done it before? Yes, but you can’t do it alone. Lenders want to see experience on the team. You can hire a professional hotel management company. This “borrows” their 30 years of experience for your loan application.

You can also find a partner who has built hotels before. Lenders love seeing a seasoned pro on the paperwork. If you have a strong background in other real estate, like apartments, that helps too. You must show that you understand how to manage people and big budgets.

Guide to hotel construction loan application process

Getting a loan is a long process. Most government loans take 60 to 90 days. Private loans can close in just a few weeks. Here are the steps:

Pre-Qualification: Talk to a lender like HotelLoans.Net. We check your credit and the basics of your project.

Branding: If you want a flag, get your brand approval letter now.

The Package: Collect your STR reports, feasibility studies, and GMP contract.

Underwriting: The bank checks every detail. They look at your “Global Cash Flow.” This means they check all your businesses, not just the hotel.

Closing: You sign the papers and pay the fees.

Draws: You don’t get all the money at once. The bank pays in stages as you finish parts of the building.

Many investors are choosing hotel renovation construction loans vs new build strategies in 2026. Building new is expensive. Renovating an old hotel is often faster. You can get a loan for a Property Improvement Plan (PIP). This is a list of changes required by a brand.

Renovations are easier to finance because the building is already there. You have a history of guest stays. This makes the bank feel safer. You can use an SBA 7a loan to cover the costs of new paint, furniture, and tech upgrades.

Regional Costs and Realities

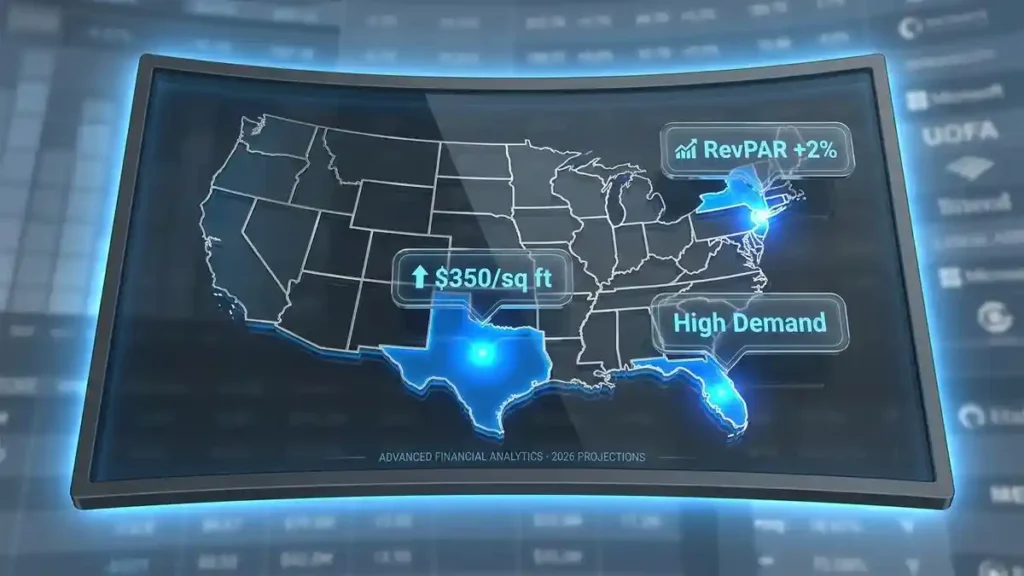

Where you build matters; the South is seeing significant growth. Florida and Georgia are hot markets. Costs are lower there than in New York or California. In big cities, new laws like the “Safe Hotels Act” are making labor more expensive.

Region

Build Cost ($/sq ft)

Growth Drivers

Sun Belt

$375 – $600

Population growth and tourism.

Texas

$350 – $550

New tech jobs and events.

Northeast

$500 – $850

High demand but high union costs.

Why work with a Super Broker?

The hotel world is too complex for a general bank. You need a specialist. HotelLoans.Net acts as a “super broker.” We don’t just send your file to one bank. We use our 30 years of underwriting knowledge to match you with the best of our 75 loan options.

We also offer referral programs for brokers. If you are a real estate broker, you can send your clients to us. We handle the hard financial work. You get to offer your clients more choices. This helps everyone win in a fast market.

Conclusion: How to get hotel construction loans for long-term success

Building a hotel is a big dream. It requires the right partners and the right money. The market in 2026 is full of opportunities. But you must be ready. You need a 680 credit score and a strong team. You need to choose between the flexibility of an SBA 7 (a) loan and the stability of a 504 loan.

At the end of the day, your project succeeds when the math works. Use real data from places like Forbes or the SBA. Partner with experts who know the hospitality sector inside and out. With a clear playbook and the right financing, your new hotel can become a staple of the American landscape. If you are ready to start, let’s look at your options today.

FAQs

Can C-PACE help finance green hotels?

Yes. This program helps you build energy-efficient hotels. You can use it as equity for USDA loans. It covers green costs, such as HVAC and lighting. It often has lower interest rates than traditional construction loans.

Does my hotel meet SBA eligibility rules?

Yes, if most guests stay for less than 30 days. Your property must get over half its revenue from short-term travelers. Lenders call this the transient occupancy rule. It ensures your hotel is a business and not an apartment.

Is my debt-to-income ratio too high?

No, if it stays below forty-five percent. This ratio compares your monthly debt to your gross income. Lenders use this to see if you have enough cash for new payments. Lower ratios help you get approved faster.

Can I buy out my hotel partner?

Yes. New 2025 guidelines allow SBA 7(a) loans for partner buyouts. You can also fund an employee buy-in. This gives you more control over your business. You must show that the project remains stable after the ownership change.

Are there extra fees for USDA loans?

Yes. You must pay a three percent initial guarantee fee. There is also a small annual fee on the loan balance. These costs help the government back your loan. Some projects qualify for a lower one percent fee.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.