Hotel renovation loan programs are financing products designed to fund your hotel’s upgrade, whether that means a full structural overhaul, a brand-mandated Property Improvement Plan (PIP), or a simple room refresh. The five programs every hotel owner must know in 2026 are the SBA 504 loan, bridge loans, DSCR loans, USDA Business & Industry (B&I) loans, and CMBS loans.

Why 2026 Is the Best Year to Finance Your Hotel Renovation

Interest rates are coming down. The American Hotel and Lodging Association said lower rates will “bring down the cost of capital and encourage new investment.” U.S. hotel transaction volume already climbed 3.9% year-over-year to $9.7 billion in the first half of 2025.

That trend is accelerating.

At the same time, a $48 billion wave of CMBS hotel loans is maturing in 2025 and 2026. Hotels that are run-down or stalled on renovations are struggling to refinance. Hotels that have upgraded are walking into lenders with strong numbers and getting deals done.

Guests are pickier than ever. Economy hotels posted 5.2% RevPAR growth in mid-2025 because budget travelers showed up expecting clean, modern rooms. Luxury hotels posted 3% growth for the same reason. Tired properties in the middle lost ground.

The 2026 FIFA World Cup is bringing an international crowd to the United States. That wave of demand is already priced in. Owners who renovate now will catch it. Owners who wait will watch someone else cash in.

2026 Hotel Renovation Market Snapshot

| Indicator | 2025 Figure | 2026 Outlook | Source |

| Global renovation market | $653.86 billion | $720.33 billion | Research & Markets |

| U.S. hotel transaction volume (H1 2025) | $9.7 billion (+3.9% YoY) | Continued growth | JLL Report |

| U.S. hotel construction market | Declining CAGR | $23.8 billion | IBISWorld |

| U.S. hotel RevPAR growth | -0.3% (2025) | +0.6% projected | CoStar / Tourism Economics |

| CMBS hotel delinquency rate | 7.29% (Aug 2025) | Stabilizing | Matthews 2026 Report |

The 5 Must-Know Hotel Renovation Loan Programs for 2026

No single loan works for every hotel. Your property size, ownership structure, cash flow, and renovation scope all matter. These five programs cover the full range of hotel renovation financing options for small businesses and large operators alike.

1. SBA 504 Loan for Hotel Renovation

What Is It?

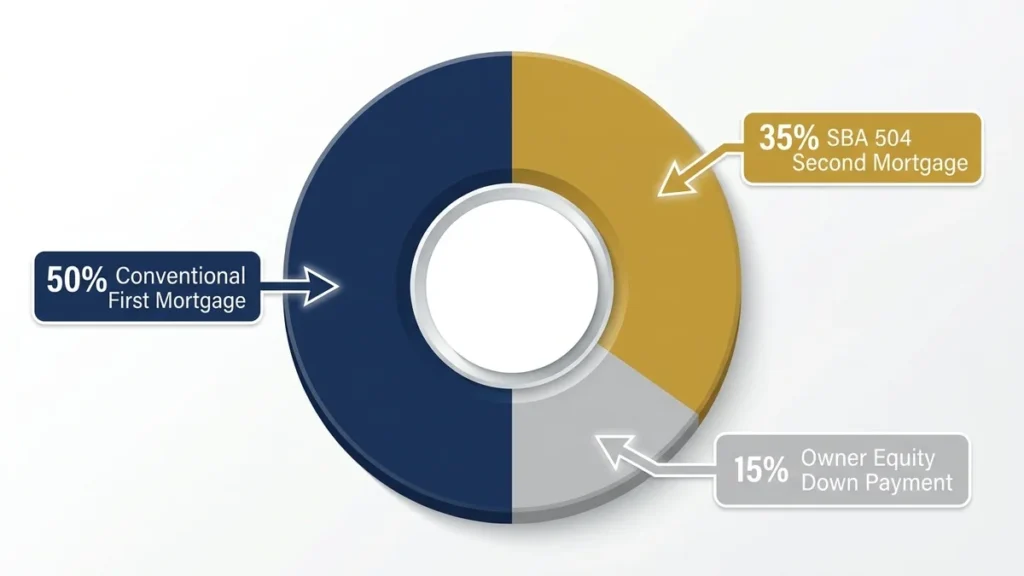

The SBA 504 loan is a government-backed program that splits your financing three ways. A conventional lender provides the first loan. A Certified Development Company (CDC) issues a second loan backed 100% by the SBA. You bring equity, often as little as 15%.

The SBA portion carries a fixed rate tied to the 10-year U.S. Treasury rate. In 2026, the blended rate on a 504 loan ranges from 5.5% to 7% for the CDC portion. That fixed, long-term rate is the whole point.

What Can You Use It For?

The SBA 504 loan for hotel renovation covers the big structural work. Think roofs, HVAC systems, facades, major build-outs, energy-efficiency upgrades, and ADA-compliance projects. It also covers furniture and fixtures when they are part of a larger real estate transaction.

The SBA Green Program allows you to use 504 financing for up to 3 energy-efficiency projects per company, with higher loan limits. HVAC upgrades, LED lighting, building envelope improvements — all eligible.

The SBA 504 has no maximum project cost. The SBA-backed portion caps at $5.5 million, but the total project size can go far beyond that by pairing it with the conventional first loan.

Is This Loan the Right Fit for You?

| Eligibility Factor | What You Need |

| Business type | For-profit, owner-operated hotel |

| Net worth | No more than $15 million |

| Average net income (past 2 years) | No more than $5 million after taxes |

| Ownership structure | Active owner-operator, no passive investors |

| Franchise status | Franchised or independent, both qualify |

| Renovation scope | Structural, long-life improvements only |

| Typical loan range | $5 million to $20 million |

Best-fit scenarios for SBA 504 hotel financing include full structural overhauls, brand-mandated PIP compliance work, HVAC and roof replacements, franchise hotel renovation financing, and energy-efficiency improvements. If you plan to own the property long-term and want a fixed payment you can budget around, this is the program to start with.

2. Bridge Loans for Hotel Renovation Projects

What Is a Bridge Loan and Why Does It Work for Hotels in Renovation?

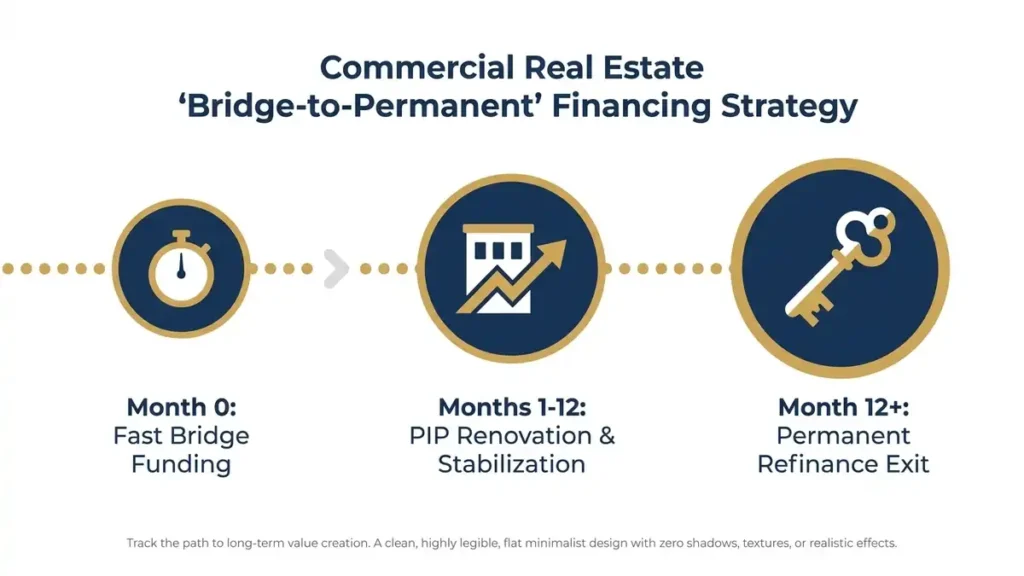

A bridge loan is short-term financing, usually 6 to 36 months. It funds the gap between today and permanent financing. For hotel owners in the middle of a renovation, it is often the only tool that fits.

Here is why. Banks and permanent lenders look at your current income. A mid-renovation hotel has no current income. Rooms are down. Revenue is low. A conventional lender sees a problem. A bridge lender sees the plan.

Bridge lenders underwrite on your future stabilized cash flow, not today’s numbers. They want to know what the hotel will earn once the work is done. That forward-looking underwriting is what makes bridge loans for hotel renovation projects so powerful.

What Do Bridge Loans Cost in 2026?

Bridge loan rates are expected to range between 8% and 15% in 2026, indexed to SOFR or Treasury benchmarks. They are not cheap. But they are fast. You can close a bridge loan in two to four weeks. That speed matters when a franchise deadline is three months away.

Loan-to-value goes up to 75% to 80% on bridge deals. Most bridge lenders do not require a minimum DSCR at closing. They evaluate whether your projected stabilized income will support permanent financing once the renovation ends.

Bridge Loan vs. SBA 504: Which One Should You Choose?

| Feature | Bridge Loan | SBA 504 Loan |

| Best use case | Active renovation, transitional property | Long-term structural upgrade |

| Loan term | 6 to 36 months | 10 to 25 years |

| LTV | Up to 75% to 80% | Up to 90% total project cost |

| DSCR required at closing | Often none | Typically 1.25x and above |

| Interest rate type | Variable (SOFR-based) | Fixed (CDC portion) |

| Time to close | 2 to 4 weeks | 60 to 120 days |

| Best for | First-time buyer, value-add play | Experienced owner, long-term hold |

The Bridge-to-Permanent Exit Strategy

The smartest operators use bridge loans as a launch pad. They fund the renovation with bridge financing, stabilize the property, then refinance into a permanent loan once cash flow is healthy. Private lenders for hotel renovation financing often structure this path from the start.

To make the exit work, you need 6 to 12 months of stabilized income, a DSCR of at least 1.25x, and a post-renovation appraisal that supports a loan-to-value at 75% or below. Hit those three marks, and the refi door opens.

3. DSCR Loans for Hotel Renovation

Why Are DSCR Loans Changing the Game for Hotel Investors?

A DSCR loan qualifies you based on one thing: the property’s income. Not yours. No W-2s. No tax returns. No personal income documentation at all.

That makes DSCR loans a standout among hotel renovation financing options for small businesses where the owner takes income in non-traditional ways. Self-employed operators, portfolio investors, and foreign nationals who would never qualify on paper for a bank loan often sail through DSCR underwriting.

The math is simple. Your Debt Service Coverage Ratio compares the property’s net operating income to its annual debt payment. A 1.25x DSCR means the hotel earns $1.25 for every $1.00 it owes. Most lenders in 2026 require a minimum of 1.25x to 1.30x, calculated on post-renovation stabilized income.

What Do Lenders Actually Look At in 2026?

Hotel lenders pull 12 months of actual operating performance. They cap occupancy assumptions at 75%-80%, even if your property runs higher. That conservative approach protects the lender and keeps borrowers from overextending on inflated projections.

CoStar and Tourism Economics project U.S. hotel RevPAR growth of just 0.6% in 2026. Lenders know this. They push back hard on aggressive proformas. Anchor your numbers to your competitive set data, and you will have a much smoother approval.

DSCR Loan Quick Facts for Hotel Owners in 2026

⦁ Minimum DSCR: 1.25x to 1.30x based on stabilized NOI

⦁ LTV: up to 75% to 80%

⦁ Income verification: property cash flow only

⦁ No W-2s or personal tax returns required

⦁ Best pairing: bridge loan entry, DSCR permanent financing as exit

⦁ C-PACE energy financing can improve your effective DSCR

4. USDA Business and Industry Loan for Historic Hotel Renovation

The Underused Program That Most Hotel Owners Have Never Heard Of

The USDA Business and Industry loan program covers hotel projects in rural areas. Acquisition, renovation, new construction, refinancing — it handles all of it. Loan amounts go up to $25 million per project. Terms stretch to 30 years. Rates are competitive because the government backs the loan.

The key requirement is location. Your hotel must sit in a USDA-designated rural area, generally defined as a community with a population under 50,000. The loan must also create or retain local jobs.

Loans for historic hotel restoration are where this program really shines. Old properties in small towns and coastal villages often qualify. The government grant and loan backing make projects viable that traditional lenders would never touch.

Real Deals That Closed With USDA Financing in 2025

In July 2025, Thomas Financial Group closed a $19.975 million USDA B&I loan for the refinance and full renovation of the Mendocino Hotel and Garden Suites and Hill House Inn in California. The project restored guest rooms, relaunched a restaurant, reopened the largest indoor event space on California’s North Coast, and created more than 50 new jobs.

That same year, Peachtree Group used a $12 million bridge loan paired with $6 million in C-PACE financing to acquire and renovate the Byways Hotel Portfolio in Alpine and Fort Davis, Texas. The USDA B&I program provided the long-term takeout financing once renovations were complete.

These are not outliers. The USDA B&I program has financed Marriott-branded hotels, boutique coastal inns, and independent rural properties across the country.

| USDA B&I Loan Factor | What You Need to Know |

| Location requirement | USDA-eligible rural area (population under 50,000) |

| Maximum loan amount | Up to $25 million per hotel project |

| Maximum repayment term | Up to 30 years |

| Job requirement | Must create or retain jobs in rural community |

| Eligible uses | Acquisition, renovation, refinancing, new construction |

| Government backing | USDA guarantee reduces lender risk and your rate |

| Best property types | Historic hotels, boutique inns, rural resort properties |

This is the boutique hotel renovation financing guide entry that most owners never read. If your property sits in a smaller market, run the USDA eligibility check before you do anything else.

5. CMBS Loans for Larger Hotel Renovation Projects

What Makes a CMBS Loan Different?

CMBS stands for Commercial Mortgage-Backed Securities. Lenders bundle these loans into bonds sold to investors. The structure creates one major advantage for borrowers: the loan is non-recourse.

Non-recourse means the lender can only come after the property if you default. Your personal assets stay protected. For larger hotel deals above $10 million, that protection is often worth the trade-offs.

CMBS rates in 2026 run fixed at 7% to 10.5% for hotel assets, priced at a spread above the 10-year Treasury. Larger branded hotels with strong franchise flags get tighter spreads. Independent limited-service hotels pay more. LTV typically lands between 55% and 65%.

The Bridge-to-CMBS Strategy That Smart Operators Are Using

Savvy operators in 2026 are combining programs. They finance the renovation with a bridge loan, stabilize operations, and then refinance into CMBS at the new, higher property value. The bridge funds the transition. CMBS locks in long-term non-recourse fixed debt.

This matters because the $48 billion CMBS maturity wave hitting 2025 and 2026 is squeezing owners who borrowed at 3% to 4.5% rates and now face 6.25% to 7% costs. That is a 40% jump in debt service. Owners who renovated and stabilized before this wave are refinancing from a position of strength. Those who waited are selling.

| CMBS Loan Feature | Advantage | Watch Out For |

| Non-recourse structure | Personal assets protected | Full recourse on some carve-outs |

| Fixed interest rate | Predictable payments for full term | Rate range 7% to 10.5% in 2026 |

| Loan size | Works well for $10 million and above | Not practical for small properties |

| Prepayment | Long fixed term works for hold strategy | Defeasance or yield maintenance penalty |

| Income verification | Property-based underwriting | Requires stabilized cash flow at closing |

| Closing timeline | 60 to 90 days | Slower than bridge financing |

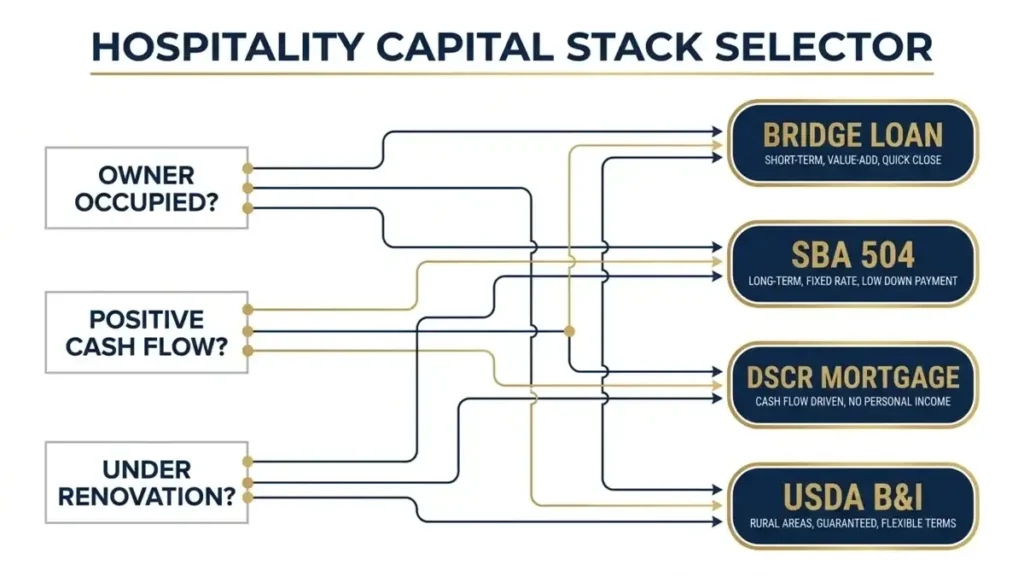

How Do You Pick the Right Hotel Renovation Loan for Your Property?

Start with three questions. First, do you actively operate the hotel or do you hold it as an investment? Owner-operators open the door to SBA programs. Passive investors tend to favor DSCR and CMBS. Second, does your hotel have positive cash flow right now? A mid-renovation with low revenue needs bridge financing. A stabilized property qualifies for permanent loans. Third, what is your total renovation budget, and how long is your timeline?

The table below maps your situation to the right program.

| Your Situation | Best Program | Why It Fits |

| First-time owner, small hotel, owner-occupied | SBA 7(a) | Highest leverage, flexible terms, lower barrier to entry |

| Experienced owner, $5M or more, structural work | SBA 504 | Fixed rate, 25-year term, low blended cost |

| Hotel mid-renovation, no current cash flow | Bridge Loan | No DSCR required at closing, closes fast |

| Investor-owned hotel, no tax returns available | DSCR Loan | Qualifies on property income only |

| Rural or historic hotel property | USDA B&I | Up to $25M, 30-year term, government-backed |

| Large stabilized hotel, non-recourse priority | CMBS | Fixed rate, non-recourse, ideal for $10M and above |

| Energy or HVAC upgrades within any project | C-PACE | Off-balance sheet, 15 to 30-year repayment |

Many deals in 2026 layer more than one program. Bridge plus USDA B&I. Bridge plus C-PACE. SBA 504 plus C-PACE for energy upgrades. The best hotel refurbishment loans 2026 often combine two tools to lower the overall cost of capital. That is where a lender with deep underwriting experience, not just one product to sell, makes a real difference.

How to Apply for a Hotel Upgrade Loan: A Step-by-Step Guide

The process does not have to be complicated. Break it into six steps.

1. Define your renovation scope. Know what you are building before you talk to a lender. Get contractor bids. Identify whether the work is PIP-mandated or voluntary. Lenders want specifics.

2. Pull your trailing 12-month financials. Gather your profit and loss statement, STR report, occupancy data, and trailing 12-month net operating income. This is called your T-12 package, and every serious lender will ask for it.

3. Calculate your DSCR and current LTV. Most programs require a DSCR of 1.25x or better and a loan-to-value ratio below 80%. Know your numbers before a lender tells you.

4. Match your situation to the right program. Use the table above or call a specialist who works across multiple programs. Applying for the wrong loan wastes months.

5. Prepare your full loan package. See the document checklist below.

6. Submit, compare, and negotiate. Never accept the first term sheet. Compare offers across lenders. Rate, fees, prepayment terms, and personal recourse all affect the real cost of the loan.

Document Checklist: What Lenders Need Across Each Program

| Document | SBA 504 | Bridge | DSCR | USDA B&I | CMBS |

| Last 3 years of tax returns | Required | Optional | Not needed | Required | Required |

| Trailing 12-month P&L | Required | Optional | Required | Required | Required |

| STR or franchise performance report | Required | Optional | Required | Required | Required |

| Renovation scope and contractor bids | Required | Optional | Optional | Required | Required |

| Personal financial statement | Required | Optional | Not needed | Required | Not needed |

| As-is and as-complete appraisal | Required | Optional | Required | Required | Required |

| Environmental report | Required | Optional | Optional | Required | Required |

| Business plan and proforma | Required | Optional | Optional | Required | Optional |

Compare hotel renovation financing rates across at least three lenders before you commit. The difference between a 6.5% and a 7.5% rate on a $5 million loan is $50,000 per year. Over 20 years, that is $1 million. Shopping matters.

What Does a Hotel Renovation Actually Do to Your Bottom Line?

Let the data speak. Hotels that renovate consistently see average daily rate increases of 8% to 15% once the work is complete. That lift flows directly into RevPAR and net operating income.

Economy hotels led all U.S. segments in mid-2025 with 5.2% RevPAR growth. Luxury hotels came in at 3%. Both segments outperformed middle-tier properties that deferred capital investment. The pattern repeats every cycle: spend on the property, earn it back in rates and occupancy.

Deferred maintenance compounds the problem. Harvard Business School research on capital allocation confirms that properties skipping upgrades lose competitive positioning within 18 to 24 months. Guests move on. Review scores drop. Brands issue PIP notices. The cost of not renovating keeps growing every quarter you wait.

By the Numbers: 2026 Hotel Renovation Financing

⦁$720.33 billion: global lodging renovation market size in 2026

⦁2,118: record U.S. hotel renovations and brand conversions at close of Q4 2025

⦁$25 million: maximum USDA B&I loan per rural hotel project

⦁5.5% to 7%: SBA 504 blended debenture rate range in 2026

⦁1.25x: minimum DSCR required by most hotel renovation lenders

⦁30 years: maximum repayment term on USDA B&I loans

⦁8% to 15%: typical post-renovation ADR increase for upgraded hotels

Ready to Fund Your Hotel Renovation? Here Is Your Next Move.

You now know the five programs. You know which one fits your situation. The next step is not research. The next step is a conversation.

HotelLoans.Net has spent 30 years underwriting hospitality real estate. The team works as a correspondent and table lender with access to 75 loan programs spanning SBA 504, bridge loans, DSCR, USDA B&I, CMBS, hard money, construction-to-permanent, Fannie Mae, Freddie Mac, and more. When a deal needs a super-broker approach, HotelLoans.Net taps a network of private lenders and investors built over three decades.

The team works with first-time hotel buyers and experienced portfolio operators. Whether experienced or new, franchised or independent, a rural inn or an urban tower, the right hotel renovation loan programs exist for your deal. The goal is to find them fast and structure them right.

Tell us about your property. We will tell you which programs you qualify for and what your path looks like.

What HotelLoans.Net Brings to Your Deal

⦁75 loan programs covering every hospitality real estate scenario

⦁30 years of underwriting experience across SBA, CMBS, bridge, DSCR, and USDA B&I

⦁Access to private lenders and investors is not available through traditional bank channels

⦁Expert guidance for new and experienced hospitality real estate investors

⦁Exclusive and non-exclusive referral programs for hospitality brokers

This is how to apply for a hotel upgrade loan the right way: match the program to the property, prepare a clean package, and work with a specialist who has closed these deals before. That combination is what gets renovations funded and properties back on the market performing.

FAQs

What credit score do I need for a hotel renovation loan?

SBA programs generally require a minimum personal credit score of 680. Bridge and DSCR lenders may approve deals at 640 and above if the property’s cash flow is strong. CMBS lenders focus almost entirely on property DSCR and debt yield, not your personal credit score. Hotel renovation loan eligibility criteria vary by program, but strong cash flow can offset a lot.

Can small hotel loans for motel renovation use these same programs?

Yes. SBA 504, SBA 7(a), bridge loans, DSCR loans, and USDA B&I loans all apply to motels, independent hotels, and boutique properties. You do not need a franchise flag to qualify. Brand affiliation helps with some lenders, but it is not a requirement across most programs. Small hotel loans for motel renovation work the same way as loans for larger branded properties.

How long does it take to get funded?

Bridge loans close in 2 to 4 weeks. SBA 7(a) loans typically close in 30 to 60 days. SBA 504 takes 60 to 120 days. CMBS loans run 60 to 90 days. USDA B&I loans can take 60 to 120 days, or longer, depending on the state office’s volume. If you are racing a franchise PIP deadline, bridge financing is the fastest path.

What is a PIP, and how do I finance it?

A Property Improvement Plan is a renovation requirement that your franchisor (Hilton, Marriott, IHG, and others) sends you. It comes with a deadline, a scope, and a cost estimate. Franchise hotel renovation financing solutions for PIP work typically involve bridge loans, SBA 504, or construction-to-permanent loans. Missing a PIP deadline can cost you the franchise flag. That loss of the flag kills the property’s value overnight.

Are there hotel renovation loans with no income verification?

DSCR loans qualify on property income alone. No W-2s. No personal tax returns. No-doc and lite-doc loan programs are available through private lenders to hospitality real estate investors for hotel renovation financing. Stated-income loans are another option for operators who keep income within business entities. Requirements for hotel improvement loans in these categories are lighter on personal documentation but heavier on property performance data.