Investors are snatching up the best hospitality real estate deals at a record pace. If you wait, you will miss out. Data from JLL Hotels & Hospitality Group shows U.S. hotel transaction volume climbed 17.5% in 2025 to reach a massive $24 billion. This momentum rolled right into early 2026, with first-quarter deal volumes jumping another 14.4% year-over-year to $5.6 billion. Private equity funds are on the attack, armed with deep cash reserves and ready to deploy capital. To lock in your share of this lucrative market, you must act fast.

But you cannot close a deal without the right backing. For your next hotel loan, choose the best lender who understands the unique pulse of the hospitality market. The right funding partner can make or break your purchase.

That is where HotelLoans.Net steps in. We act as a professional financial consulting firm, a correspondent lender, a table lender, and a super broker. We have 30 years of underwriting experience. We offer 75 distinct loan options. We only assist with your real estate investment property. We do not run your daily hospitality business. Instead, we provide the financial roadmap you need to purchase land, build a property, or execute a rehab. Whether you want to fix-and-flip, fix-and-hold, or fix-and-rent, we guide you to the finish line.

When you search for commercial debt, you must know what to look for in a hotel loan lender. Hospitality properties do not operate like typical office buildings. Office tenants sign long-term leases that guarantee steady rent. Hotels do not have that luxury. Instead, a hotel rents its rooms night by night. This means its income changes every single day.

Because of this daily shift, underwriters look at two main areas. They look at the physical real estate, which they call the “hardware.” They also look at the daily business operations, which they call the “software”. You need a funding partner who can analyze both.

Your lender must understand daily lodging metrics. They will check your Revenue Per Available Room. You calculate this using a simple formula:

RevPAR = {ADR} *{Occupancy Rate}

Lenders also evaluate your RevPAR Index. This index shows if your property captures its fair share of the local market. The calculation compares your hotel to your direct competitors:

RevPAR Index = {{Subject Property RevPAR}\{Competitive Set Average RevPAR}} *100

An index score of 100 means you are on par with your competitors. If your score drops to 80, you are underperforming by 20%. A smart lender will notice this drop and ask why.

Underwriters also focus on your Global Debt Service Coverage Ratio. This metric evaluates your entire financial ecosystem. Lenders look at all the properties you own, not just the target asset. They want to see a Global DSCR of 1.25x or higher. This ratio ensures you have a 25% cash cushion to cover seasonal revenue declines.

Finally, ask about capital reserve requirements. Standard credit providers require a dedicated escrow account for Furniture, Fixtures, and Equipment. This is your FF&E reserve. Lenders typically require you to fund this account with 4% to 5% of your gross monthly revenues. This reserve keeps your property competitive and prevents a loss of value.

How Do You Evaluate Hotel Loan Lender Experience?

Many traditional banks treat hotels like basic commercial spaces. They fail to understand seasonal cash flow swings and brand standards. When they get nervous, they reject your request. You must learn how to evaluate a hotel loan lender’s experience before signing an application.

Start by asking about their past hospitality transactions. Have they closed loans with major national hotel brands? Do they know how to read a Smith Travel Research report? An experienced underwriter relies on STR data to track market demand and local occupancy trends. They do not just look at a generic regional appraisal.

Research from Oxford University and Harvard Business School highlights why hospitality operations are so complex. Oxford scholars point out that commercial real estate has shifted to an operational, customer-centric model. This shift means that online review sites like TripAdvisor directly drive guest demand and room rates. A seasoned lodging lender knows this reality. They will review your management team’s online reputation and operational history, not just your personal tax returns.

Your funding partner must also have a deep understanding of your brand’s specific rules. Major hotel companies enforce strict Property Improvement Plans. These plans mandate regular upgrades to maintain the brand flag. If your lender does not understand these PIP rules, your project will stall.

At HotelLoans.Net, we bring 30 years of underwriting expertise to your deal. We know how to package your transaction so credit committees say yes. We analyze your STR reports, check your RevPAR Index, and assess your global cash flow upfront. This preparation prevents unexpected delays and gets you funded on time.

What Are Your Main Criteria for Choosing a Hospitality Loan Provider?

You must establish clear criteria for choosing a hospitality loan provider. This step prevents you from wasting weeks with the wrong financial partner. A bad match can cause you to miss your purchase deadline and lose your earnest money deposit.

First, check the lender’s flexibility with property types. Some banks only fund standard select-service hotels. But you might want to buy a motel, a restaurant, a recreation center, or a vacation rental. You might need capital for a raw land purchase or a ground-up build. Ensure your lender can fund your exact property type.

Second, look at their licensing and structure. Are they a direct lender, a correspondent, or a broker? HotelLoans.Net acts as both a correspondent lender and a table lender. We also serve as a super broker when a deal requires a highly specialized private capital source. This multi-path approach gives you access to 75 distinct loan options.

Third, check their credit score requirements. Government-backed programs usually require a personal credit score of 680 or higher. Conventional banks look for scores above 620. Alternative and private lenders offer much more flexibility. They can work with scores as low as 550 if your property shows strong, consistent monthly revenue.

Finally, analyze their asset-level requirements. A quality lender evaluates the strength of your management team. They want to see at least two years of direct hotel management experience on your team. This operational track record reduces their perceived risk and helps secure better loan terms.

To Secure a Hotel Loan Choose the Best Lender for Your Property

The commercial real estate market is highly competitive. To close your transaction on time, you must secure a hotel loan and choose the best lender from day one. Working with an inexperienced bank will lead to endless paperwork and missed deadlines.

Our team at HotelLoans.Net acts as a financial consultant to help you navigate this complex market. We understand that lodging assets require tailored debt solutions. That is why we provide a massive network of private lenders, institutional funds, and government programs.

We can assist you with a broad range of options, including:

Bridge loans for quick acquisitions or transitional properties.

Hard money loans for fast, asset-backed funding.

DSCR loans focus on your property’s cash flow rather than personal income.

USDA B&I loans are designed to support rural lodging developments.

SBA loans, including the SBA 7(a) and SBA 504 programs.

FHA commercial property investment loans for long-term stability.

CMBS loans for non-recourse, fixed-rate financing on stabilized assets.

Specialized no-doc, lite-doc, and state income loans for fast execution.

We do not manage your hotel’s daily staff or clean your guest rooms. We focus entirely on the debt. We make sure your capital structure is strong so you can focus on driving occupancy and growing your business.

How Do You Choose the Best Lender for a Hotel Construction Loan?

Building a hotel from the ground up is a high-risk endeavor. To succeed, you must learn how to choose the best lender for a hotel construction loan. Construction loans are complex and require careful draw management.

Typical lodging construction loans carry variable interest rates ranging from 9% to 14%. Lenders usually limit leverage to 60% to 75% of the total project cost. Because your project generates zero cash flow during the building phase, underwriters are highly cautious.

To offset this building risk, select a lender who understands the pre-stabilization phase. You need an interest reserve built directly into your loan. This reserve covers your monthly debt payments while construction is underway.

Your lender will also analyze the local lodging supply. Slower supply growth across major markets supports the performance of existing hotels. JLL reports that most major U.S. cities show construction pipelines below 2% of their existing room supply. A smart lender wants to build in these undersupplied areas. They will reject projects in saturated markets to protect their capital.

Make sure your lender requires a realistic cost contingency budget. Quality underwriters mandate a 10%-15% cost contingency. This cushion covers supply chain inflation and unexpected delay costs. It ensures you have enough capital to complete the build and secure your brand flag.

Finally, look for a lender who offers a smooth path to permanent financing. A construction-to-permanent loan automatically converts your variable-rate building debt into a fixed-rate mortgage once the hotel opens. This conversion saves you thousands in closing fees.

Why Should You Compare Hotel Loan Lenders’ Interest Rates?

To get the best deal, you must compare hotel loan lenders’ interest rates and upfront fee structures. A low nominal interest rate can be highly misleading. High origination fees, strict prepayment penalties, and short amortization periods can quickly ruin your cash flow.

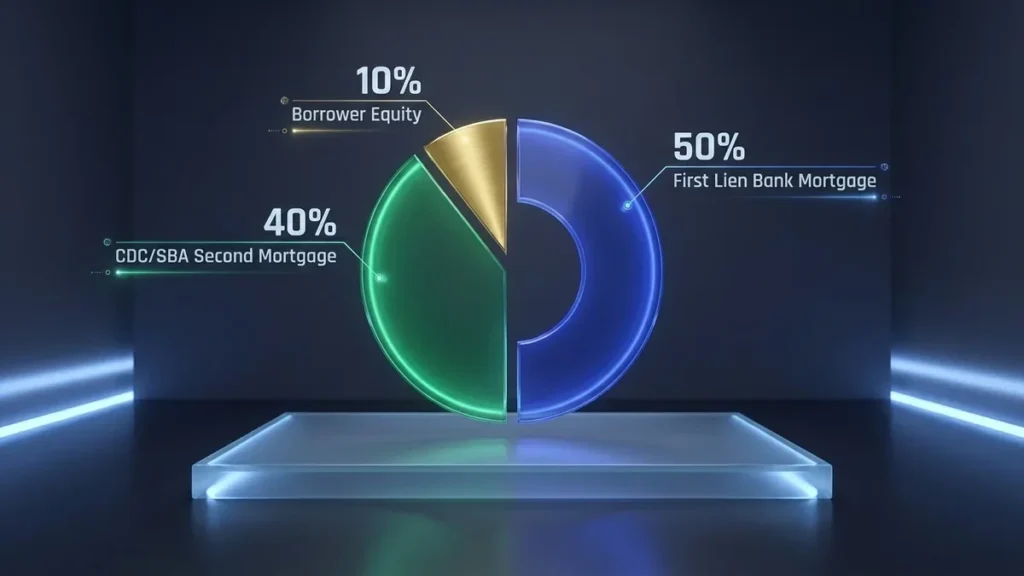

Start by looking at the SBA 504 program. This is the premier tool for major lodging projects. The SBA 504 uses a unique 50/40/10 structure. A private bank provides a first mortgage covering 50% of the project cost. A Certified Development Company provides an SBA-backed second mortgage covering up to 40% of the loan amount. You only contribute 10% to 20% as equity.

This structure offers massive benefits. The CDC second mortgage gives you a 25-year fixed interest rate. This fixed rate protects you from rising inflation and swings in the prime rate. To find the right partner, check an active SBA 504 hotel loan lender list to locate CDC groups in your state.

The federal government’s GAO reported that hotels accounted for 12% of all approved SBA 504 loans, making them the largest small-business category using the program. In Q1 2023, hotels and motels led the SBA 504 volume with $151.9 million across 54 loans, averaging $2.8 million per loan.

When planning renovations, you must compare hotel renovation and loan lenders. Compare the flexible SBA 7(a) program with the SBA 504 program. The 7(a) program is highly versatile. It can finance your entire brand-mandated property improvement plan, including soft costs like employee training and working capital. The SBA 504 program is much more restrictive. It only funds long-life structural upgrades like HVAC systems, roofs, or facade work.

But the 504 program has a major cost advantage. It features no standard SBA guarantee fee on the CDC portion. The 7(a) program charges upfront guarantee fees ranging from 3.5% to 3.75% of the guaranteed amount.

Understanding hotel loan lender fees and charges is essential before signing any term sheet. Ask for a complete breakdown of all underwriting points, processing fees, and appraisal costs.

The table below compares the major hotel loan structures:

Financing Structure

Interest Rate Range

Leverage (LTV/LTC)

Key Funding Uses

SBA 7(a)

Prime + Spread

Up to 90%

Acquisitions, full PIP rehabs, soft costs

SBA 504

5.61% – 5.94% Fixed

Up to 90%

Land purchases, builds, structural PIPs

CMBS Conduits

6.00% – 7.00% Fixed

Up to 75%

Stabilized flagged asset refinancing

Private Bridge

SOFR + 350-600 bps

Up to 80%

Transitional deals, brand conversions

How Do You Decide Between Regional Banks vs National Lenders for Hotel Loans?

Sponsors often face a tough decision when choosing a credit partner. Should you focus on regional banks vs national lenders for hotel loans? The answer depends on your property’s scale, brand status, and your own balance sheet strength.

Regional banks excel at relationship lending. They know your local market and can move quickly on unflagged properties. But they almost always require full recourse. This means you must sign a personal guarantee, putting your personal assets at risk if the deal fails. They also keep loan limits lower, often capping out at $5 million to $10 million.

National lenders and Wall Street CMBS conduits operate differently. They focus on larger, stabilized assets. They offer non-recourse debt, which protects your personal wealth. But they have rigid underwriting processes and charge high prepayment fees.

National conduits are often the best lenders for hotel acquisition loans if you are buying a stabilized, branded property. They can easily fund deals over $15 million. They analyze the asset’s direct cash flow rather than your personal tax returns.

If you are buying an independent property, look for the best hotel loan lenders for boutique hotels. Independent hotels lack the corporate reservation systems of major national flags. Traditional lenders view them as high-risk assets. Because of this risk, boutique properties often require larger down payments of 20% to 25%. Flagged select-service hotels can often secure funding with just 10% to 15% down.

To close a boutique deal, find a lender who can underwrite your local market positioning. They will check your management team’s track record and digital reviews. They must understand how your unique guest experience drives room revenues without a national brand flag.

What Are the Top Commercial Hotel Financing Lender Selection Tips?

To secure the most competitive debt financing, you must follow proven tips for selecting commercial hotel lenders. These steps will help you filter out weak banks and target the most aggressive capital providers.

First, prioritize lenders who focus on Debt Yield. This is a crucial risk metric for non-recourse debt. Debt Yield measures the pure cash return a lender would receive if they had to take over the property today. You calculate it using this formula:

In today’s market, top CMBS lenders require a minimum Debt Yield of 13.5% or higher. Private debt funds and bridge lenders are more flexible. They may accept a Debt Yield of 9.5% to 11% in exchange for slightly higher interest rates.

Second, work with an advisor to find a hotel loan lender with flexible terms. Look for step-down prepayment penalties, such as a 5-4-3-2-1 structure, rather than rigid yield-maintenance covenants. This flexibility allows you to refinance or sell the property early without paying massive exit fees.

Third, prepare a detailed list of questions to ask hotel loan lenders during your initial phone call. This step ensures you discover any structural deal-breakers before paying for expensive appraisals.

Your checklist of questions to ask hotel loan lenders should include:

What is the minimum Debt Yield required for this loan size?

Does your underwriting team require full personal recourse, or is this a non-recourse loan?

Do you require a fixed cost contingency budget for brand-mandated renovations?

What are the ongoing FF&E reserve requirements for this asset class?

Can we finance the upfront SBA guarantee fees directly within the loan proceeds?

How Do You Coordinate Your Closing and Referrals?

Closing a lodging transaction requires massive coordination. You are transferring an active, operating business, not just a physical structure. To avoid delays, you must implement hotel real estate financing best practices, including lender coordination, from day one.

Start by gathering all your property and financial documents early. Underwriters will check three years of certified profit and loss statements, corporate tax returns, and current year-to-date operating data. They will also request your latest STR reports to verify your market share.

Next, coordinate with your franchise brand. Lenders require a Franchise Comfort Letter before funding. This letter confirms that the brand agreement will remain active after the ownership change. If you delay this request, your closing will stall.

You must also coordinate environmental reviews and property condition assessments. A Phase I Environmental Site Assessment is a standard requirement for all commercial lodging debt. Commission this report as soon as you sign your purchase contract.

Finally, utilize professional referral networks. HotelLoans.Net offers highly competitive, exclusive, and non-exclusive referral programs for commercial brokers. If you are a real estate broker, we help you structure and close complex debt packages for your clients.

We provide expert financial advice for both seasoned brokers and professionals new to the lodging sector. We can help arrange financing for land purchases, hotels, motels, restaurants, recreation centers, and vacation properties. Our vast network of private capital and institutional lenders ensures your clients get the most flexible terms.

Secure Your Hospitality Investment Today

Navigating the commercial debt market is a complex challenge. The current hospitality environment shows a clear K-shaped recovery. Luxury properties are seeing strong RevPAR growth, while economy motels face rising pressure from deferred maintenance and CMBS delinquencies. To protect your capital, you must match your target asset with the perfect debt structure.

Our team at HotelLoans.Net is here to guide you. We act as your financial consultant, correspondent lender, and table lender to find the optimal financing fit. We analyze your pro forma metrics, check your submarket supply, and help you structure a winning application.

Do not let a weak bank delay your purchase or force you into bad terms. For your next hotel loan, choose the best lender in the industry. Contact our advisory team today to review our 75 loan options and secure the funding you need to grow your hospitality investment portfolio.

FAQs

Is hotel loan interest tax-deductible?

Yes. Interest paid on a hotel commercial mortgage is usually tax-deductible as a legitimate business expense. This deduction reduces your overall taxable net income, making debt financing a very cost-effective path for active real estate investors.

Can first-time buyers get hotel loans?

Yes. First-time buyers can get financing if they present a strong business plan and hire experienced managers. However, lenders often view them as high risk and require a larger down payment of twenty percent.

Can C-PACE finance energy-efficient upgrades?

Yes. C-PACE provides long-term, fixed-rate capital specifically for sustainable upgrades such as HVAC systems and roofs. This funding can cover up to 35% of your capital stack, helping lower monthly utility bills.

Do USDA loans support rural hotels?

Yes. USDA Business and Industry loans support hotel projects in rural areas. Borrowers can use these competitive funds for new construction, property acquisition, or refinancing to lower rates and improve overall monthly operational cash flows.

Can you finance hotel equipment with bad credit?

Yes. You can secure hotel equipment financing with a personal credit score as low as six hundred. Because the physical machinery itself acts as direct collateral, lenders are highly flexible even if you have active credit challenges.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.