Right now, $48 billion in hotel debt is hitting a massive wall of maturities across the United States. This is not a drill. Over 70% of hotels appraised for sale face immediate, expensive property improvement plans (PIPs). If you own a hotel or plan to buy one, the next 12 months will decide your survival. You cannot afford to guess your funding needs. If you make one wrong move, you will lose your property to the bank or drop your franchise brand. Read this guide now to secure hotel loans the right loan amount.

At HotelLoans.Net, we have 30 years of underwriting experience. We do not run your hotel business. We only fund real estate investment properties. We offer 75 different loan options through our private lender network. We act as a correspondent lender, table lender, and sometimes a super broker. We also help brokers through our exclusive and non-exclusive referral programs. Let us look at how you can get the exact funding you need.

How to Calculate Hotel Loan Amount Without Crashing Your Cash Flow?

Lenders do not view your hotel as a standard office building. Hotels have daily changing rates and occupancy. This makes them much more volatile than properties with long-term tenants. To determine your borrowing limit, lenders consider your adjusted Net Operating Income (NOI). Here is the formula they use:

Lenders take this adjusted NOI and apply a Debt Service Coverage Ratio (DSCR). This ratio tells them how much room you have to pay your mortgage. Most hotel lenders want a DSCR of 1.25x to 1.40x. If your hotel makes $1.25 million in NOI, your annual mortgage payments cannot exceed $1 million. Underwriting hotel loans for the correct amount requires getting this calculation right. If you overestimate your income, you will run out of cash fast.

What Are the Hidden Factors Affecting Hotel Loan Size?

What changes the amount of money a lender will give you? First, they look at your Revenue Per Available Room (RevPAR) Index. Your RevPAR Index compares your hotel to your local competitors. A RevPAR Index of 100 means you are getting your fair share of the market. If your index is under 80, your hotel is underperforming. Lenders will see this as a high risk and lower your loan amount.

Second, lenders look at your net worth and liquid reserves. They want you to have a net worth of at least the loan amount. They also want to see post-closing liquidity equal to 6 to 12 months of mortgage payments. This protects them if the hotel has a bad winter season.

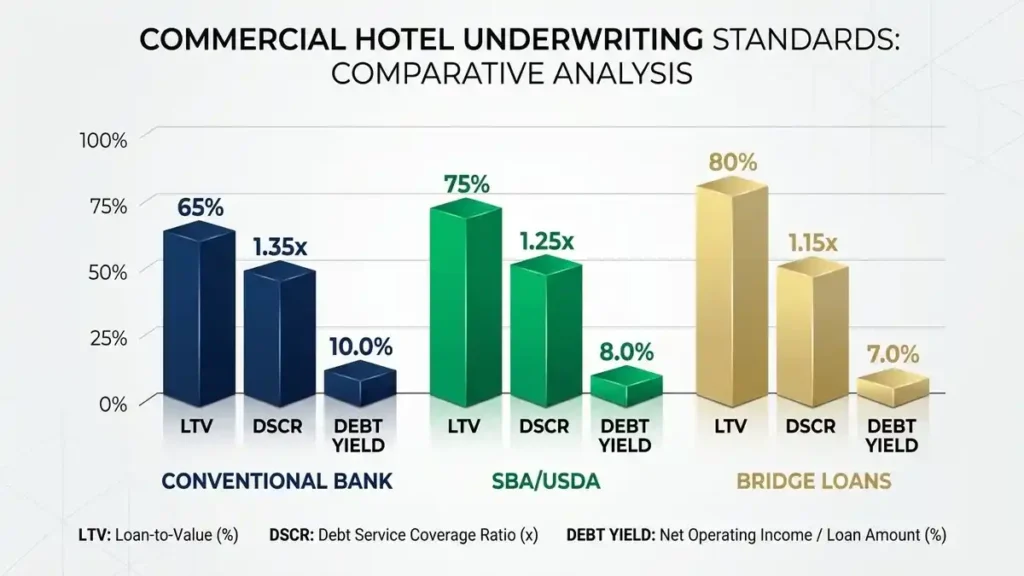

Here is a simple table showing typical underwriting guidelines:

Metric

Conventional Bank

SBA / USDA

Bridge

Typical LTV

55% to 70%

75% to 90%

65% to 80%

Min DSCR

1.25x to 1.40x

1.15x to 1.25x

1.10x or Yield

Debt Yield

10.0% to 12.0%

Not Applicable

8.0% to 10.0%

Amortization

25 to 30 Years

25 Years

Interest-Only

The Blueprint for Determining Optimal Hotel Financing Amount

How do you find the sweet spot for your loan size? You must balance high leverage against your monthly costs. If you take out an SBA 7(a) loan, you can get up to 90% leverage. But these loans have variable rates. A high variable rate can eat up your cash flow fast if interest rates spike.

If you plan to hold your hotel for 10 years, you might prefer a fixed-rate CMBS loan. These loans cap leverage at 60% to 70%. You have to bring more equity to the table, but your monthly payments are stable.

You can also combine different loans to get more money. For example, you can get a conventional first mortgage. Then, you can add a mezzanine loan or C-PACE funding. This keeps your personal equity safe while keeping your payments manageable. Determining the optimal hotel financing amount is about balancing risk and reward.

How Does the Hotel Mortgage Loan Amount Calculation Protect Your Equity?

Lenders use three main checks to size your loan. They use Loan-to-Value (LTV), DSCR, and Debt Yield. They run these three calculations and give you the lowest amount. This is the core of the hotel mortgage loan amount calculation.

Imagine your hotel appraises at $10 million with an NOI of $1 million. If a lender caps LTV at 70%, that allows a $7 million loan. If they require a 12% Debt Yield, the limit drops to $8.33 million. If the DSCR constraint limits the loan to $6.5 million, the lender will enforce that limit. This math protects you from borrowing more than your property can pay back.

What Influences Hotel Development Loan Size for Your Brand Conversion?

Building a new hotel or converting a property is a complex process. Because you have no historical data, lenders must look at projections. They rely on feasibility studies to predict your future occupancy and rates. The franchise flag you choose plays a huge role in determining the size of a hotel development loan.

Research from Cornell University’s Center for Hospitality Research shows branded hotels achieve 10% to 15% higher occupancy than independent properties. This is because brands have massive loyalty programs and global reservation networks. Lenders love this lower risk. They will reward a branded property with a larger loan size and higher loan-to-cost (LTC) limits.

Tips for Securing the Right Hotel Loan Amount on Acquisition Day

How do you get lenders to say yes to your target loan amount? You must prepare a professional underwriting package. Here are our top tips for securing the right hotel loan amount:

Gather three years of audited financials, STR reports, and a realistic 10-year pro forma.

Hire a brand-vetted property management company. Lenders feel safe when they see an operator with a strong track record of cutting costs and driving bookings.

Address physical defects early by getting a preliminary property condition report.

These steps prove to the lender that you know what you are doing.

How Much Can I Borrow for a Hotel Purchase Using Private Capital?

Your maximum borrowing limit depends on the loan program you choose. SBA programs are great for smaller acquisitions. They allow you to borrow up to 90% of the purchase price, but they cap the loan size at $5 million. Conventional banks and CMBS loans are better for larger deals. They require 25% to 40% down but can fund projects up to $150 million. Knowing how much I can borrow for a hotel purchase helps you plan your equity injection.

Here is a breakdown of the main programs:

Program

Borrowing Range

Down Payment

Recourse

Conventional Bank

$2M to $50M

25% to 40%

Full Recourse

SBA 7(a) Loan

Up to $5M

10% to 15%

Personal Guarantee

SBA 504 Structure

Up to $15M Projects

10% to 20%

Personal Guarantee

CMBS Conduit

$5M to $150M

30% to 45%

Non-Recourse

Bridge / Private

$1M to $25M

10% to 30%

Limited Recourse

Your Practical Hotel Acquisition Loan Amount Guide

When you buy a hotel, you need a smart plan for your capital stack. Most buyers use a senior mortgage to cover 60% of the purchase price. They then layer mezzanine debt or C-PACE capital to cover another 15% to 20%. This reduces the cash you need to bring to closing. This hotel acquisition loan amount guide helps you see how different pieces fit together.

This structure helps you keep your personal cash liquid. You can use that extra cash for unexpected costs or seasonal drops in occupancy.

How to Structure Your Capital Stack for Maximum Leverage?

If you want to maximize your leverage, you must combine different funding sources. A typical capital stack looks like this:

Senior Debt (60%): This is your primary mortgage from a bank or CMBS lender. It has the lowest interest rate but the strictest rules.

Mezzanine Debt / C-PACE (20%): This sits behind the senior debt. It fills the gap between your mortgage and your equity.

Sponsor Equity (20%): This is your personal cash investment.

By structuring your deal this way, you can acquire high-value assets with less of your own money on the line.

Maximizing Hotel Loan Approval Amount with Smart Mezzanine Layers

If a senior lender will not provide enough capital, mezzanine debt can bridge the gap. Mezzanine loans sit behind your first mortgage but ahead of your equity. They carry higher rates, usually between 11% and 14%. Lenders will check if your property’s cash flow can support the combined payments. We can help you analyze these costs to ensure your deal remains profitable. Maximizing hotel loan approval amount is easy when you use mezzanine layers correctly.

Underwriting Hotel Loans for the Correct Amount Under Strict Lender Rules

Lenders use the Debt Yield metric to size their exposure. The Debt Yield is calculated by dividing your adjusted NOI by the total loan balance.

Debt Yield = {{Adjusted NOI}\{Loan Principal Balance}} * 100

Most lenders want to see a Debt Yield of 10.5% to 12.0% for premium properties. If your NOI drops, they will cut your loan size. To avoid this, you can focus on increasing your property’s efficiency. Using labor-saving technology, such as automated check-in kiosks, can boost your NOI and help you secure a larger loan. Underwriting hotel loans for the correct amount requires keeping a close eye on this metric.

Getting the Best Hotel Loan Amount for Renovation and Brand Mandates

Getting funding for renovations is all about timing. Property improvement plans (PIPs) are expensive. Economy hotels average $8,000 to $15,000 per key. Midscale properties run $15,000 to $35,000 per key. Full-service hotels can exceed $80,000 per key.

If your PIP is scheduled within the first 24 months, lenders will bundle it into your acquisition bridge loan. If it is scheduled later, they will stress-test your cash flow and require larger monthly reserves. Getting the best hotel loan amount for renovation depends on how well you plan these timelines.

Meeting Commercial Hotel Loan Amount Requirements Without Stress

To meet strict commercial hotel loan amount requirements, you need a clean financial history. Lenders will ask for audited P&L statements, tax returns, and franchise agreements. If your property has deferred maintenance, lenders will reduce your loan size.

You can negotiate with your brand to phase your PIP over multiple low-occupancy seasons. This keeps your cash flow healthy and keeps lenders happy.

Small Hotel Loan Amount Advice for Independent Properties

Independent motels with fewer than 100 rooms lack the backing of a major brand. They trade at lower EBITDA multiples, usually 4x to 7x. Lenders view them as high risk because they lack global reservation systems. Conventional banks will cap your LTV at 50% to 60%.

To get more funding, you should look at government-backed programs. SBA and USDA B&I loans can provide up to 90% leverage. This small hotel loan amount advice can save your independent business.

Here is a comparison of these programs:

Metric

SBA 7(a)

SBA 504

USDA B&I

Max Loan Size

Up to $5M

Up to $5.5M

Up to $25M

Typical Amortization

25 Years

20 to 25 Years

15 to 30 Years

Best Use

Real Estate + PIP

Fixed Assets

Rural Properties

Main Advantage

High Leverage

Fixed Rates

Low Rates

How to Simplify Your Boutique Hotel Loan Amount Calculation?

Boutique hotels are unique. They often rely heavily on food and beverage (F&B) sales. Lenders separate F&B revenue from room revenue. F&B revenue is more volatile, so they apply higher cap rates to it, which can lower your property value. To maximize your loan size, you must prove your operating efficiency. Showing a strong history of high margins can convince lenders to give you better terms. This is the key to successfully calculating a boutique hotel loan amount.

How to Determine Hotel Construction Loan Amount for New Builds?

Sizing a construction loan requires a very detailed budget. Your budget must include land costs, hard costs, soft costs, FF&E, and interest reserves.

Total Construction Budget = {Land Cost} + {Hard Costs} + {Soft Costs} + {FF&E Procurement} + {Interest Reserve}

Lenders typically cap construction loans at 60% to 70% of total costs (LTC). Learning how to determine the amount of a hotel construction loan helps you avoid funding shortages during development.

Here is a look at the capital needs across a hotel’s lifecycle:

Phase

Capital Need

Typical Cost Range

Primary Loan Structure

Key Focus

Acquisition

Buy Existing Asset

$2M to $100M+

CMBS or Bank Loan

Historical T-12 NOI

Renovation

Brand PIP Upgrades

$8K to $80K per Key

Bridge or SBA 7(a)

Post-PIP RevPAR lift

Construction

Ground-Up Build

$150K to $600K per Key

Construction Loan

Cost Validation

Stabilization

Working Capital

Variable

Lines of Credit

Post-Close Liquidity

Matching Reinvestment Benchmarks by Property Age

As a hotel ages, its capital needs grow. Properties under 5 years old typically spend less than 2.5% of revenue on CapEx. Properties over 15 years old spend more than 8% of their revenue to stay competitive. You must match your financing cycles with these age benchmarks.

Here is how property age impacts capital needs:

Property Age

CapEx Need

Primary Systems Affected

Best Financing Tool

1 to 5 Years

Low: Under 2.5%

Minor Soft Goods

FF&E Reserves

5 to 10 Years

Moderate: 4.0% to 5.5%

Room Furniture

SBA 7(a) or C&I Loan

10 to 15 Years

High: 6.0% to 8.0%

Lobby, Bathrooms, Roof

Refinance + Cash-Out

15+ Years

Severe: Over 8.0%

HVAC, Elevators, Structural

CMBS + Mezzanine

Hotel Loans: The Right Loan Amount: A Strategic Conclusion

Succeeding in today’s hospitality market takes extreme precision. With billions in CMBS debt maturing and brands enforcing strict PIPs, you cannot afford to guess your funding needs. One miscalculation can drain your cash flow and put your investment at risk.

At HotelLoans.Net, we are ready to help you navigate this shifting landscape. We bring 30 years of underwriting experience to the table. We only handle real estate investment properties and help you find the perfect option from our 75 loan programs. Whether you need a bridge loan, hard money, a DSCR loan, or government-backed SBA and USDA B&I options, we have you covered.

If you are a broker, we offer exclusive and non-exclusive referral programs to help you close more deals. If you want to secure a hotel loan for the right amount, connect with us today. Let us help you maximize the value of your assets and secure your financial future.

FAQs

Is PIP insurance for hotel renovations?

No. In car insurance, PIP stands for Personal Injury Protection, which covers medical bills. In our hospitality world, it is a brand Property Improvement Plan. Stop losing sleep and call us now to fund your hotel renovation.

Can green upgrades lower your loan costs?

Yes. Installing green HVAC and lighting upgrades slashes your utility bills by up to thirty percent. This massive boost in cash profit satisfies green loan underwriters. Call our expert team right now to secure your money.

Can you borrow money for land?

Yes. We can help you secure the financing to purchase vacant land specifically for your next commercial hotel construction project. This fast action locks down prime real estate. Call us today to start your deal.

Will a low credit score stop you?

No. While traditional bank and government programs require a very high credit score, private hard-money options focus strictly on property value. Stop worrying now and call our expert team today to fund your purchase.

Do you fund daily hotel operations?

No. We specialize strictly in real estate investment property transactions. We do not provide capital or management consulting to run your daily hospitality business operations. Call our team today to secure your real estate mortgage.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.