U.S. hotel rooms under active construction jumped 7% this year to 157,000 keys. Yet, the physical supply of new rooms is growing at only 0.5%. If you are waiting on the sidelines, you are missing out on record-high room rates. Developers are racing to break ground before their competitors do. However, regional banks are pulling back hard on lending. This means you must know how to secure the best hotel construction loan rates to keep your project alive.

You need a partner who knows the system. HotelLoans.Net is a table lender, correspondent, and advisor. We have 30 years of deep underwriting experience. We do not run your hotel. We focus only on real estate investment properties. With our network of private lenders, we provide 75 different loan options. We help you buy land, build, or do a value-add project. Let us look at how math works.

We calculate your project cost using the Weighted Average Cost of Capital (WACC). This formula shows how debt and equity work together:

WACC = ({E}{V} *Re) + ({D}{V} * Rd *(1 – T))

In this formula, E is your cash equity. D is your construction debt. V is the total development cost. Re is the return your equity partners expect. Rd is your nominal interest rate. T is your tax rate. To make your project pencil out, you must keep Rd as low as possible.

Macroeconomic Shifts and Average Hotel Construction Loan Interest Rates

What are the current market rates for hotel construction financing? The Federal Reserve cut its rate to a range of 3.50% to 3.75%. This is a relief for builders. But long-term bond rates remain high. The 10-year Treasury yield is hovering at 4.59%.

Most building loans use a floating rate. These are tied to the 30-day Secured Overnight Financing Rate (SOFR), which sits at 3.64%. Lenders add a margin on top. This margin depends on your deal. This determines new hotel construction financing rates for 2026.

If you look at the average hotel construction loan interest rates, you see a wide range. Standard commercial bank loans range from 5.50% to 8.75%. Private debt funds and credit platforms charge more. Their rates can run from 9.00% to 12.00% or higher. You must know how lenders price these deals.

Factors Affecting Hotel Construction Loan Interest Rates in Daily Tenancy Asset Classes

Why do hotels face higher interest rates? Lenders look closely at daily tenancy. If you own an office building, tenants sign ten-year leases. But hotel guests leave after one night. This creates volatile cash flow.

A famous Cornell study by Peter and Stephanie Nolan of the School of Hotel Administration shows that lenders price this risk through a spread. This spread can peak at 320 basis points over the risk-free rate. This premium is a major factor affecting hotel construction loan interest rates.

When room rates drop, your income drops instantly. On top of this, your operating costs are high. You have to pay for housekeeping, utilities, and marketing. Lenders know these expenses are hard to cut. This risk directly drives up your pricing.

Let us look at current index yields:

Index / Benchmark Class

Current Yield (May 2026)

Typical Construction Spread (Basis Points)

Projected Floating-Rate Range

WSJ Prime Rate

6.75%

+125 to +300 bps

8.00% to 9.75%

SOFR (30-Day Index)

3.64%

+275 to +500 bps

6.39% to 8.64%

5-Year U.S. Treasury

4.26%

+150 to +300 bps

5.76% to 7.26%

10-Year U.S. Treasury

4.59%

+175 to +320 bps

6.34% to 7.79%

5 Ways to Guarantee You Get the Best Hotel Construction Loan Rates

To secure the lowest rate, you must lower the lender’s risk. Here are five proven strategies to achieve this.

Way 1: Optimize Leverage Profiles and Find Hotel Construction Loans with Low Down Payment

Banks used to offer 80% loan-to-cost (LTC). Today, they limit senior loans to 55% or 65% LTC. If you put more cash down, your rate drops. Lenders offer tighter spreads to borrowers who put more skin in the game.

But what if you want to keep your cash? You can search for options for hotel construction loans with low down payments. By using a second mortgage or preferred equity, you can lower your cash down to 10%.

Here is how we calculate your Loan-to-Cost ratio:

LTC = {{Total Loan Balance}/{Total Hard and Soft Development Costs}}

Lowering this ratio decreases your rate. We can estimate your spread reduction with this formula:

{Spread Reduction} approx f(Delta LTC)

A 10% drop in LTC can save you 25 to 75 basis points on your senior rate. This saves thousands of dollars in interest carried during the build.

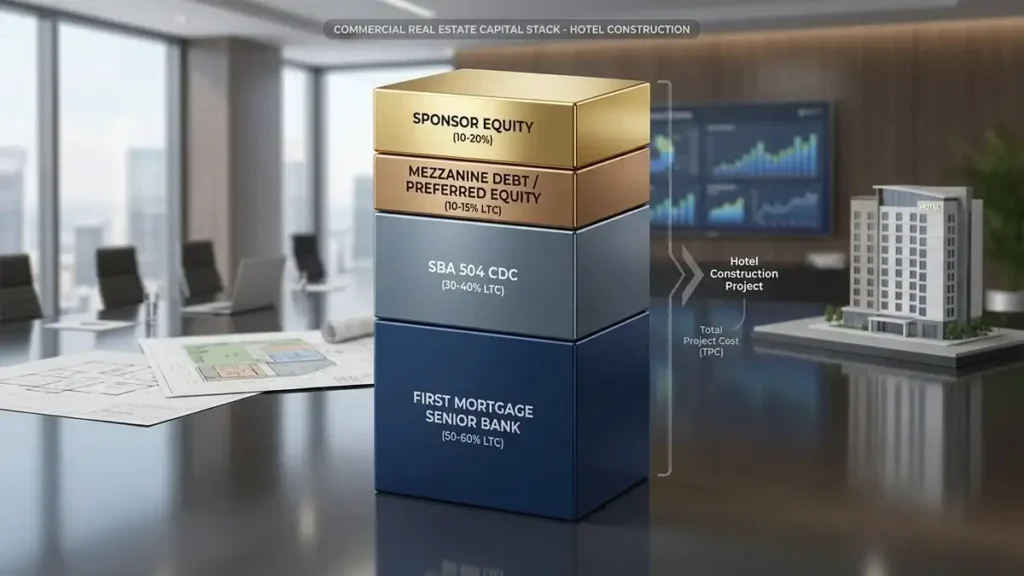

Capital Stack Layer

Typical LTC Allocation

Average Pricing Range (2026)

Recourse Requirements

First Mortgage (Senior Bank)

50% – 60%

5.50% – 7.50%

Full or Partial Recourse

Second Mortgage (SBA 504)

30% – 40%

5.85% – 5.91%

Non-Recourse to Personal Assets

Mezzanine Debt / Preferred Equity

10% – 15%

8.00% – 12.00%

Non-Recourse Carve-Outs Only

Sponsor Cash Equity

10% – 20%

Target IRR 18%+

N/A

Way 2: Implement Comprehensive Broker Audits to Compare Hotel Construction Loan Lenders’ Rates

Do not talk to just one bank. You must compare the rates offered by hotel construction loan lenders to find the sweet spot. Different lenders want different deals. A local bank might want low leverage. A debt fund might allow higher leverage but charge a higher rate.

We help you shop your deal. This forces lenders to compete for your business. We look at three main items when we compare offers:

The benchmark index used

The draw fees and inspection rules

Prepayment fees and exit terms

What are commercial bank hotel construction loan rates?

Traditional banks offer some of the lowest pricing. Today, commercial bank hotel construction loan rates range from 5.50% to 8.75%. To get these rates, you need a credit score of 680 or more. You also need to show strong liquidity. Banks typically require you to hold 12 months of interest reserves in cash.

Way 3: Utilize Government Facilities and SBA Hotel Construction Loan Rates Requirements

Government loans are an excellent tool. The Small Business Administration provides great terms. You can use the SBA 7(a) program for up to $5 million.

But you must meet the SBA hotel construction loan requirements. These include a 680 credit score and personal guarantees. The SBA 7(a) rate is variable. It is tied to the Prime rate and cannot exceed Prime plus 3.0%. Today, that means your rate would be around 7.75% to 9.50%.

The SBA 504 program is even better for large projects. It offers a 25-year fixed-rate second mortgage. This rate is pegged to the 10-year Treasury and currently ranges from 5.85% to 5.91%. This is a great hedge against rising inflation.

Underwriting Variable

SBA 7(a) Construction Loan

SBA 504 Construction Loan

Maximum Loan Amount

$5,000,000

Up to $5.5M for CDC portion (No limit on senior portion)

Typical Equity Requirement

10% – 20%

15% – 20%

Interest Rate Structure

Variable (WSJ Prime + 1.25% to 3.00%)

25-Year Fixed (CDC portion)

Minimum Sponsor Credit Score

680

680

Refinance Provisions

Eligible for debt restructuring

Eligible under 90% LTV guidelines

Way 4: Execute Cost Control Measures and Track What Are Hotel Construction Loan Closing Costs

Lenders hate surprises. You must show a clear, fixed-price contract. This protects you from labor and material inflation. You also need a budget for fees.

So, what are hotel construction loan closing costs? These fees usually range from 3% to 6% of the loan amount. They cover title search, appraisal, and lender points.

Fee Classification

Average Pricing Matrix (2026)

Operational Purpose

Origination Points

0.5% – 2.0% of the loan balance

Covers lender processing and underwriting

Third-Party Appraisals

$1,000 – $10,000 per asset

Establishes prospective as-built valuations

Environmental Report (Phase I)

$2,000 – $6,000 per project

Screens for site hazards to avoid liability

Title Search & Insurance Policy

$2,500 – $15,000

Protects lender against lien claims

Underwriting & Processing Fee

$500 – $2,500

Covers lender administrative costs

Interest Reserve Account

Calculated on projected draws

Covers interest-only carry during construction

Way 5: Optimize Niches by Analyzing Boutique Hotel Construction Loan Rates

Boutique hotels are popular. But lenders see independent properties as higher risk. They lack a national brand and reservation system. This means boutique hotel construction loan rates are often higher than those of branded hotels.

To get a better rate, you need a detailed feasibility study. Show that your property has a strong local market. You must prove your daily room rate will cover your debt.

The extra risk of an independent property adds a premium to your spread:

This premium can run from 50 to 150 basis points. You can offset this by showing a strong operating plan and lean expenses.

Can you capitalize on extended stay hotel construction loan rates?

Extended-stay models are highly efficient. They have low overhead. Lenders love them. Because of this, extended stay hotel construction loan rates are highly competitive.

Lower costs per key mean your project is safer. Lenders reward this safety with lower rates.

Strategic Feasibility Frameworks and Transition Financing

How can you make a deal work? You must plan your exit strategy. Lenders want to see how you will pay off the building loan. They look at your pro forma closely.

To secure the best hotel construction loan rates, you must present clean data. This means showing real quotes and a solid contractor. You need a clear path to stabilization.

What are small hotel construction loan options?

Smaller deals need different tools. If you are building a small hotel, look at small hotel construction loan options. These include small bank loans and SBA 7(a) options. They have simpler paperwork and faster closing times.

Compare these to other paths. You might look at hotel renovation loan interest rates vs new construction costs. Renovating an existing building lets you open sooner. It also costs less.

To compare these paths, we look at the Total Acquisition Cost:

Total Acquisition Cost = {Purchase Price} + {Property Improvement Plan (PIP) Cost}

We also calculate your Stabilized Yield on Cost:

Stabilized Yield On Cost = {Projected Stabilized Net Operating Income (NOI)}}{\text{Acquisition Price} + {Renovation/CapEx Costs}}

Renovations often show a higher yield. This makes them easier to finance.

How to get favorable hotel development loan rates?

To get the best deal, complete your preconstruction work first. Get your permits and brand approvals in place. This will show lenders your project is ready to go. This is how to get favorable hotel development loan rates.

The Intermediary Advisory Architecture of HotelLoans.Net

At HotelLoans.Net, we have 30 years of underwriting experience. We help you navigate the system. We work as a correspondent and table lender. We can guide you through 75 different loan options.

We help you purchase land, build, or do a fix-and-flip. We also offer great referral programs for brokers. We do not run your hotel. We focus only on your real estate assets.

We analyze your total debt structure using the Weighted Average Cost of Debt (WACD):

We balance your senior bank debt, SBA portions, and private equity. This keeps your total cost of capital low.

Synthesis and Nuanced Conclusions

Getting the best hotel construction loan rates takes preparation. You must study the market and present a clean package. Shop multiple lenders and use government programs.

Keep these items in mind as you plan:

Keep your leverage reasonable

Work with an expert advisor

Focus on efficient hotel models

Keep your budgets accurate

With the right strategy, you can build a successful property. Contact HotelLoans.Net today to get started.

FAQs

Do CMBS hotel loans require personal guarantees?

No, CMBS hotel loans are non-recourse. This means your personal assets are safe if you default on the payments. The lender can only seize the hotel. This structure keeps your personal balance sheet clean and protected.

Are nonprofit hotels eligible for SBA loans?

No, nonprofit hotels are not eligible for SBA loans. The Small Business Administration requires all borrowers to operate strictly as for-profit companies. You must look for non-government private financing options if you run a nonprofit entity.

Do you need perfect credit for CMBS?

No, you do not need perfect credit for a CMBS loan. Lenders focus on the hotel’s cash flow and debt service coverage ratio. They care more about property income than your personal credit score, making approval much easier.

Is there an SBA 504 net worth limit?

Yes, there is a net worth limit for SBA 504 loans. Your business must have a tangible net worth of less than $20 million to qualify. Your average net income must also be under $6.5 million.

Does HUD offer forty-year hotel construction loans?

No, HUD does not offer forty-year loans for hotels. While programs like HUD 221d4 provide forty-year construction financing, they are strictly limited to multifamily rental properties. They cannot be used to build commercial hospitality real estate.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.