Right now, 30% of all outstanding hotel and motel mortgages in the United States are coming due this year. This is a massive maturity wave. Many owners face a huge risk of losing their properties. Regional banks are pulling back from hospitality real estate real estate. This means traditional refinancing is harder to secure. If you own a hotel, you must act now. Successful operators are using proactive refinancing hotel debt strategies to protect their equity before it is too late.

We are a specialized financial consulting firm. We act as a correspondent and table lender. Sometimes we act as a super broker. We have 30 years of underwriting experience. We help clients navigate the capital markets. We do not run your hotel business. We only offer and assist with hospitality real estate investment property. We have a vast network of private lenders and investors. This network lets us offer 75 different loan options.

We also support the industry. We offer exclusive and non-exclusive referral programs for real estate brokers. We help both experienced and new brokers. We offer financial advice for those who want to buy land, build, or renovate. This includes land purchases, ground-up construction, fix-and-flip, fix-and-hold, or fix-and-rent. We cover hotels, motels, restaurants, recreation centers, and vacation rentals.

How Will the 2026 Maturity Wall Impact Your Hotel?

The hospitality real estate real estate market is facing a major shift. 17% of all outstanding hospitality real estate mortgages will mature this year. This represents $875 billion in debt. Among these loans, hotels face the tightest timeline. 30%

of all hotel and motel mortgages will mature this year. This is the highest percentage of any property type.

Many of these loans were signed during a period of low interest rates. Some were extended during the pandemic. Now, these properties must find new loans. This is happening as conventional banks enforce strict rules.

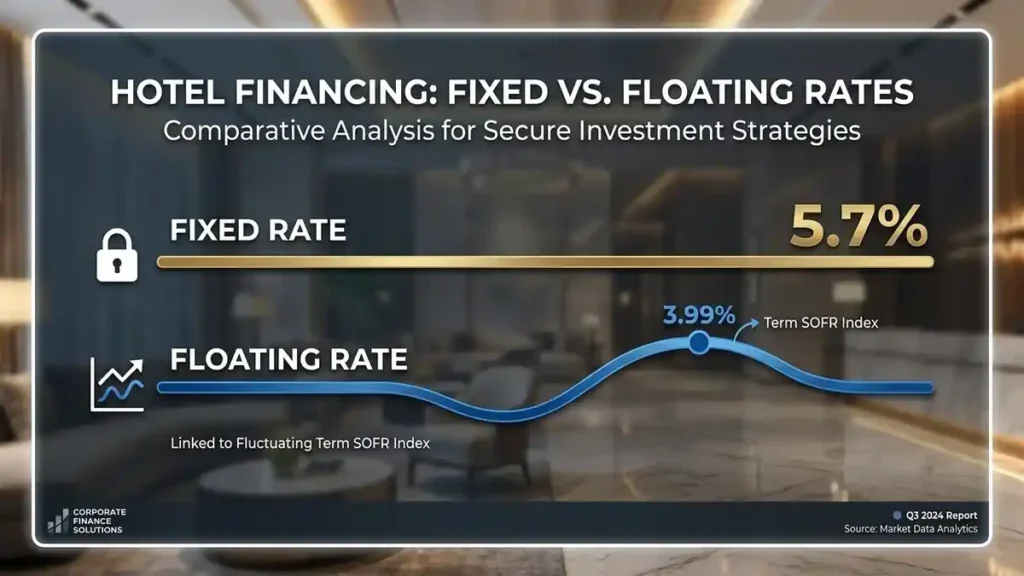

The impact of interest rates on hotel debt refinancing has been severe over the last few years. Interest rates are higher than they were five years ago. This makes refinancing expensive. The market is starting to normalize, though. The benchmark Term SOFR rate recently fell to an average of 3.99%. This is down 69 basis points from last year.

Lower benchmark rates are helping. The average interest rate on hospitality real estate mortgages recently fell to 5.7%. Average loan sizes grew by 14% year over year. Spreads for hospitality real estate loans tightened to 181 basis points for fixed-rate options with moderate leverage.

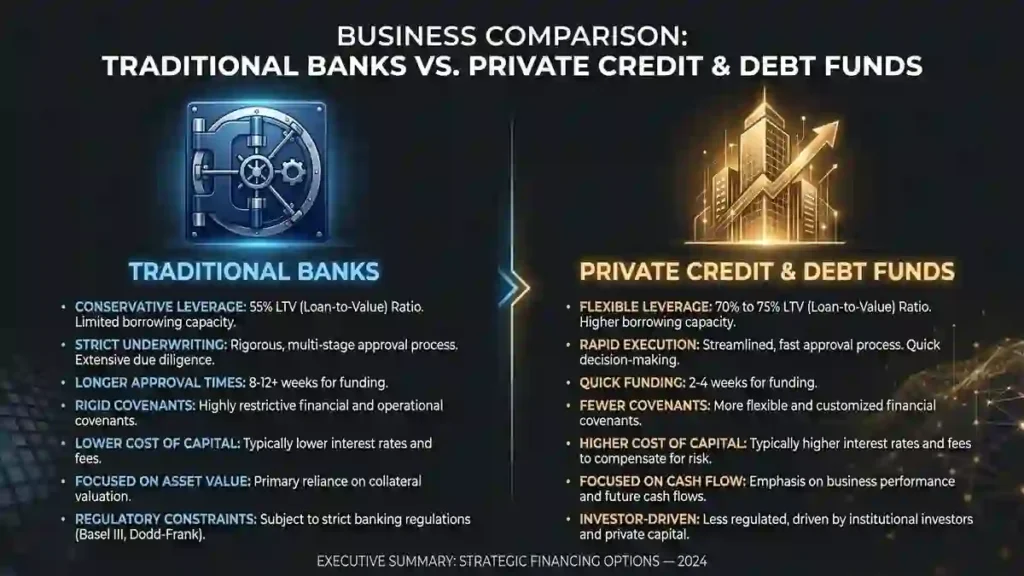

Traditional banks are still very cautious. They want to limit their exposure to hospitality real estate real estate. This pullback has opened the door for private credit. Alternative lenders recently captured 53% of all non-agency loan closings. Debt funds and mortgage REITs are taking the lead.

These shifts have triggered new distress in the lodging sector. The CMBS delinquency rate for lodging jumped to 7.31% in March 2026. This is the highest lodging delinquency rate since April 2025. Many of these delinquencies are due to matured balloons. This means the hotel is generating cash, but the owner cannot find a new loan to replace the maturing debt.

Key Macroeconomic and Lending Benchmarks

Economic Metric

Current Value

Market Impact

Maturing CRE Mortgages

$875 Billion

Creates massive refinancing pressure across all sectors

Maturing Hotel Mortgages

30% of outstanding debt

Concentration of near-term refinancing risk for owners

Average Interest Rate

5.7%

Lower borrowing costs compared to last year

Term SOFR Average

3.99%

Eases floating-rate debt costs for transitional assets

Private Credit Share

53%

Debt funds replace cautious traditional banks

Lodging Delinquency Rate

7.31%

Reflects maturity stress and tight bank lending

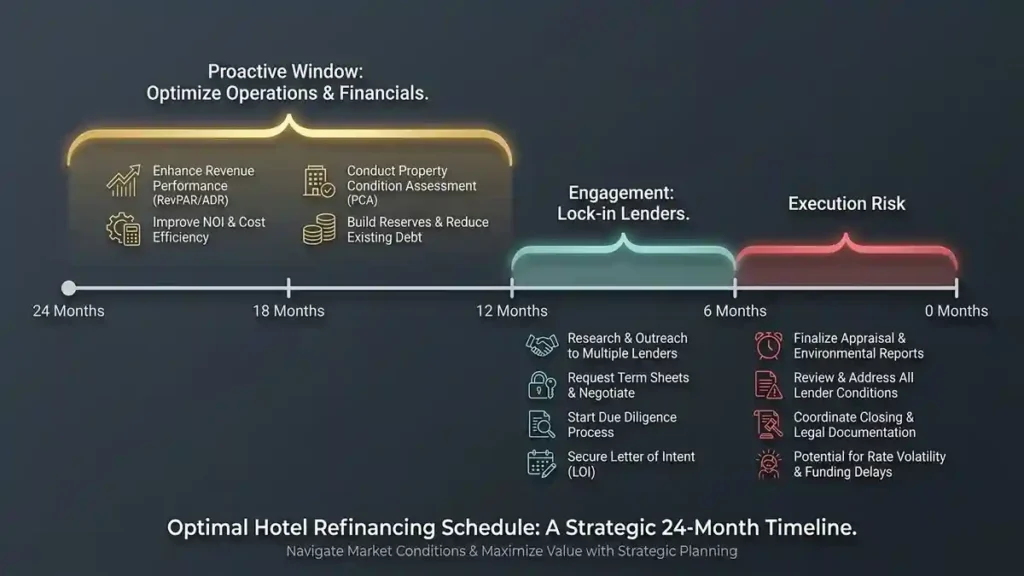

Is Now the Right Time to Refinance Your Hotel Real Estate Loans?

Timing is key, and knowing when to refinance hotel real estate loans can save you millions of dollars. Waiting until your loan matures is a dangerous plan. It leaves you with no options if the market freezes.

Start looking for a new loan 12 to 24 months before your current loan matures. This timeline gives you room to prepare. Lenders want to see stable cash flows. They analyze your Revenue Per Available Room and Average Daily Rate. They want at least two years of clean trading history.

An early start also lets you fix property issues. You can complete brand-mandated renovations. This improves your hotel’s valuation. A higher value means you need less cash to close the deal.

Refinancing Hotel Debt Strategies: What are the Best Options?

Choosing the right path requires a clear strategy. You must evaluate the best strategies for hotel debt refinancing to protect your business. Your choice affects your monthly costs and your long-term wealth.

A major decision is choosing between fixed-rate and floating-rate hotel debt refinancing. Fixed-rate loans give you long-term safety. Your payments stay the same. This is perfect if you plan to hold the hotel for many years. These loans often have high prepayment fees, though.

Floating-rate loans are different. They are tied to a benchmark, such as Term SOFR. They offer more flexibility. You can pay them off early with low fees. They are ideal for properties undergoing a fast turnaround. They expose you to interest rate changes, though. Lenders often require you to buy an interest rate cap.

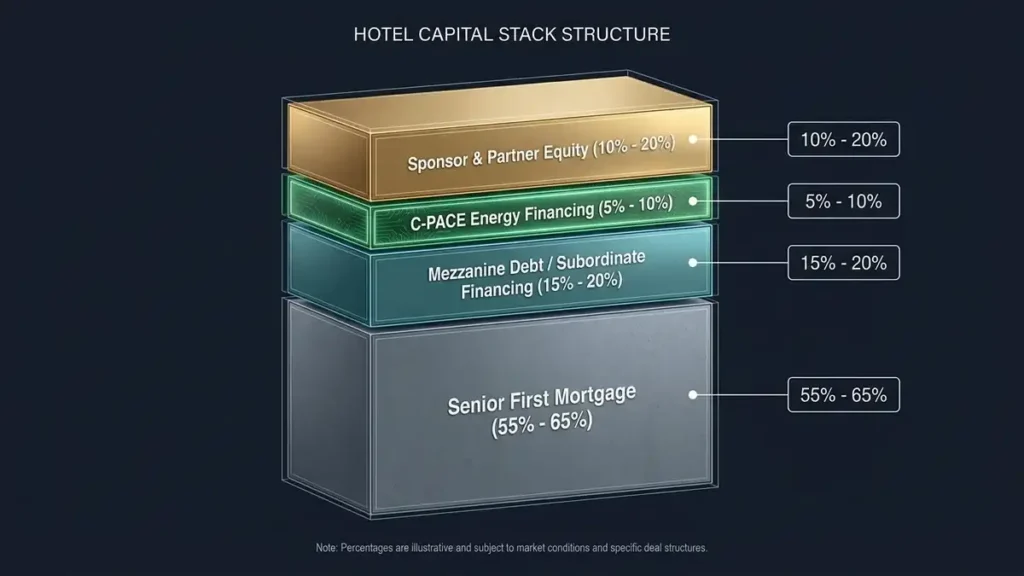

You must also understand how to refinance hotel debt in 2026. Today, the capital stack is complex. Traditional banks only fund 55% to 65% of a property’s value. You must fill the gap with other funding.

Mezzanine debt is a great tool. It sits between your main mortgage and your equity. It costs more than a senior loan, but it preserves your cash. Another option is C-PACE financing. This program funds energy-efficient upgrades. You pay it back through property taxes. This structure keeps your costs low.

The hospitality real estate market offers many credit options. This guide to hotel debt refinancing programs will help you compare them. Each loan program has unique rules and benefits.

For smaller properties, SBA loans are highly popular. The SBA 504 loan offers up to 90% financing. This means you only need a 10% down payment. It offers fixed rates and 25-year terms. The SBA 7(a) loan is another option. It provides up to $5 million for refinancing or working capital.

Lenders enforce strict rules on these SBA programs. To qualify, your property must be a special-purpose asset. You must meet the transient occupancy rule. This means more than 50% of your revenue must come from guests who stay 30 days or less.

Larger hotels often use hospitality real estate mortgage refinancing. This includes CMBS loans. CMBS lenders pool loans together and sell them to investors. They offer low rates and non-recourse terms. They are very rigid, though. CMBS lenders want to see a debt yield of 13.5% or higher. Debt yield is your net operating income divided by your loan amount.

If you are finishing a construction project, you face a different challenge. You must handle refinancing hotel construction debt. Construction loans are short-term and expensive. Takeout financing replaces these construction loans. It gives you a stable mortgage once your hotel is open and running.

Independent owners face severe refinancing challenges because they lack a brand flag. Lenders worry about demand. To win approval, you must show a strong local market plan. You must prove your management team has deep experience.

Are Hotel Loan Restructuring Options the Right Path?

Sometimes, a traditional refinance is not possible. If your property is struggling, you must look at hotel loan restructuring options. Restructuring means changing the terms of your current loan.

Lenders do not want to foreclose on your hotel. Foreclosure is costly and slow. They prefer to work with you if you have a solid plan.

You must contact your lender early. Do not wait until you miss a payment. Your lender will ask you to sign a pre-negotiation agreement. This protects both sides during talks.

You will need to provide detailed financial reports. This includes cash burn rates and short-term cash flow models. Lenders want to see that your problems are due to market changes, not poor management.

If your property is in deep trouble, you must consider distressed hotel debt refinancing options. This can include securing a short-term hard money loan. These loans have high rates, but they buy you time to stabilize the business.

Another option is a loan-to-own strategy. Under this plan, an investor buys your secured debt. They fund a structured bankruptcy or reorganization. This clears out old liabilities and protects the real estate.

Typical Loan Restructuring Modifications

Restructure Option

What It Does

What Lender Requires

Maturity Extension

Adds 1 to 3 years to loan term

Extension fees or a partial principal paydown

Amortization Holiday

Allows interest-only payments

Stricter control over cash management

A/B Note Split

Splits loan into performing and deferred notes

Fresh equity injection from the owner

Reserve Release

Uses capital reserves to make payments

Tight oversight of the operating budget

What are the Financial Rewards of Refinancing?

Replacing your old mortgage has clear benefits. You will see the benefits of refinancing hotel property loans immediately in your cash flow.

First, you can lower your monthly payments. This happens if you secure a lower interest rate or extend your loan term. Shifting from an expensive construction loan to a permanent mortgage saves a massive amount of money.

Second, you can consolidate multiple loans. Many hotels have senior debt, mezzanine loans, and equipment leases. Putting these into a single loan simplifies your business.

Third, you can access your equity. A cash-out refinance lets you pull cash out of your property. You can use this cash to fund brand renovations or buy more properties.

To get these rewards, you must find the right hotel debt refinancing lenders. The market has many capital sources. Hospitality real estate banks offer the lowest rates, but they have tight rules. CMBS lenders offer high leverage and non-recourse terms. Private debt funds move fast and fund transitional properties.

Real data shows these strategies work. We can look at case studies of successful hotel debt refinancings as proof.

One famous example is the Hotel Vertu case study from Harvard Business School. The study analyzes a boutique hotel project in Savannah, Georgia. It shows how proper deal structure and financial forecasts can help independent hotels win over lenders.

Another success story is the Hotel Perennial case study. An investment group purchased a distressed 194-room hotel in Chicago. They used a discounted cash flow model with an 8.5% cap rate. They assumed the existing debt, restructured it, and renovated the property. This strategy achieved an unlevered internal rate of return of 18.9%. The levered return reached 25.0%.

We also see this in the Songy Partners case study. During a major downturn, the firm renegotiated 12 to 15 loans that had expired. These negotiations took three to six months each. They resulted in short extensions that saved the firm from foreclosure. They used the extra time to stabilize and sell assets.

Is Your Refinancing Application Ready for Underwriting?

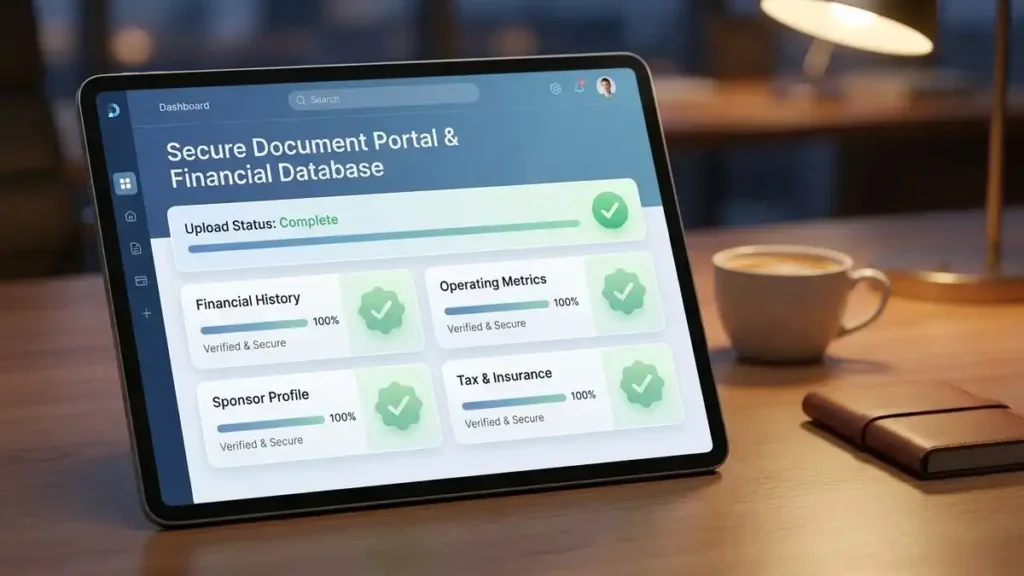

Preparing your loan package is vital. Lenders want organized information. This checklist will help you get ready.

Onboarding Checklist

Document Category

Required File

Why Lenders Need It

Financial Statements

Two years of tax returns and P&L files

To verify your historical income

Operating Reports

RevPAR, ADR, and occupancy metrics

To prove your market share and performance

Cash Projections

12-to-24-month monthly cash model

To confirm you can cover the new payments

Property Info

PIPs and renovation schedules

To show the value of your physical asset

Sponsor Profile

Personal financial statements and resumes

To check your net worth and track record

Tax & Insurance

Current property tax bills and insurance policies

To prove that senior liabilities are current

Strategic Summary for Lodging Investors

The hospitality real estate hotel market is facing a critical window this year. With a massive wave of loan maturities hitting the sector, waiting to act is a high-risk gamble. Successful owners are moving quickly to implement refinancing strategies for hotel debt. This is the best way to secure your assets and improve your cash flow.

HotelLoans.Net is here to guide you. We offer 30 years of underwriting experience. We provide financial consulting services to help you secure the capital you need. Our network of private lenders offers 75 different loan options. Whether you need an SBA, bridge, or CMBS loan, we can assist you with your investment property. Let us help you navigate this transition and build a secure financial future.

FAQs

Can you pledge personal homes as collateral?

Yes. Lenders allow you to pledge equity in your primary residence or other hospitality real estate properties. This extra collateral reduces the cash you need to put down, helping you secure a larger loan with better terms.

Is a formal property valuation always required?

Yes. Lenders instruct a chartered surveyor to complete a formal valuation before approval. This report analyzes your physical building and calculates its value as a multiple of your operating income, verifying that the asset secures the loan.

Do new hotel developers pay higher rates?

Yes. Lenders view new developers as high risks because they lack a construction history. You will face strict underwriting rules, higher interest charges, and larger equity requirements until you prove you can complete your building projects on time.

Can seller financing help with a refinance?

Yes. Seller financing helps fill equity gaps. New lenders often allow secondary notes to reduce your cash injection during a refinance, making it easier to meet strict loan limits and protect your personal liquidity when closing.

Does closing take months?

No. While many hospitality real estate transactions drag on, some lenders can close loans quickly. For example, some experienced firms can process and finalize a specialized government loan in less than thirty days if you provide complete financial files immediately.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.