The global boutique hotel market reached $28.47 billion in 2025 and is poised to reach $50.50 billion by 2033. In the US alone, this passionate sector hit a market size of $36.5 billion in 2025. If you are sitting on the sidelines, you are actively missing out on the biggest shift in modern travel history. Today’s travelers are tired of cold, cookie-cutter hotel rooms. They want unique, memorable experiences and are willing to pay a premium for them.

This massive wave of guest demand is creating an incredible opportunity for property investors. But to build or buy your dream property, you must master the ins and outs of boutique hotel financing. Finding the right capital is the difference between a thriving, cash-flowing asset and a dead deal. Let us walk through the exact steps to fund your lodging vision and secure your piece of this highly profitable market.

Finding the right money for your project is your very first step. You have several paths to choose from when looking at boutique hotel financing options. Each path has its own rules, costs, and terms.

Most hotel deals rely on a mix of different debt types. You can get long-term stable loans, or you can use quick, short-term cash to get a property up and running. Understanding how these choices compare will help you protect your bottom line.

Funding Type

Average Cost of Capital

Risk Level

Common Loan-to-Value (LTV)

Conventional Bank Loan

Low

Low

60% to 70%

SBA 7(a) Program

Moderate

Low

75% to 90%

SBA 504 Program

Low to Moderate

Low

80% to 90%

USDA B&I Loan

Low to Moderate

Medium

70% to 80%

CMBS Conduit Loan

Low to Moderate

Medium

60% to 75%

Private Bridge Debt

High

Medium

65% to 75%

Conventional bank mortgages are excellent for properties that already generate steady income. They offer low rates but have very tight rules. Government programs, such as SBA and USDA loans, lower lenders’ risk. This allows you to get high leverage with a much smaller down payment.

If you are buying a property that needs a fast turnaround, bridge loans and private debt are great options. They cost more, but they fund quickly, so you do not miss out on a hot deal.

How to Get Financing for a Boutique Hotel: Key Underwriting Benchmarks

Lenders do not view hotels the way they view typical office buildings or apartments. An apartment rents on a long-term basis, but a hotel sells its rooms night by night. This daily change makes hospitality assets a bit more volatile.

To win over a lender, you must know how to get financing for a boutique hotel by meeting strict underwriting rules. Lenders will carefully review your property’s daily performance metrics. They look at your Average Daily Rate (ADR), Occupancy Rate, and Revenue Per Available Room (RevPAR).

Lenders also want to see that your business generates enough cash to easily repay the debt. They measure this using the Debt Service Coverage Ratio (DSCR). You can calculate your DSCR using this simple formula:

DSCR = {{Net Operating Income (NOI)}/{Total Annual Debt Service}}

Most lenders require a DSCR of 1.25x or higher. This means your hotel makes $1.25 for every $1.00 you owe on your loan.

Lenders will also look at your Global DSCR. This looks at all your personal and business income and debts combined. To support your request, you must provide at least 2 years of clean tax returns, a detailed business plan, and a post-closing cash reserve of approximately 10% of the loan amount.

Academic researchers at the Cornell Nolan School of Hotel Administration note that using professional hotel valuation software is vital at this stage. It allows you to build realistic, data-backed cash flow forecasts that lenders can actually trust.

Who Are the Best Lenders for Boutique Hotel Loans?

Not all banks understand the special rhythm of the hospitality world. If you apply to a lender who only funds retail stores, they might panic when they see your seasonal booking drops.

That is why finding the best lenders for boutique hotel loans is so important. You need a partner who knows how to read hotel profit-and-loss statements.

Look for lenders who specialize in commercial real estate and hospitality. Ask them how many hotel loans they have closed in the last two years.

Regional banks and commercial credit unions are often great for stabilized assets. Private debt funds work well if you need fast cash for a turnaround.

Working with a skilled correspondent lender like HotelLoans.Net gives you a major advantage. They can instantly match your project with the perfect lender from their private network, saving you weeks of stressful applications.

Are SBA Loans for Boutique Hotels Your Best Bet?

Small Business Administration (SBA) loans are some of the most popular tools in the hotel industry. They offer fantastic terms, low rates, and long payoff times.

If you plan to own and operate your property, you should look closely at SBA loans for boutique hotels. The two main choices are the SBA 7(a) and SBA 504 loans.

The SBA 7(a) program is incredibly flexible. You can use it to buy a hotel, refinance old debt, or get working capital. These loans go up to $5 million and offer payoff terms of up to 25 years.

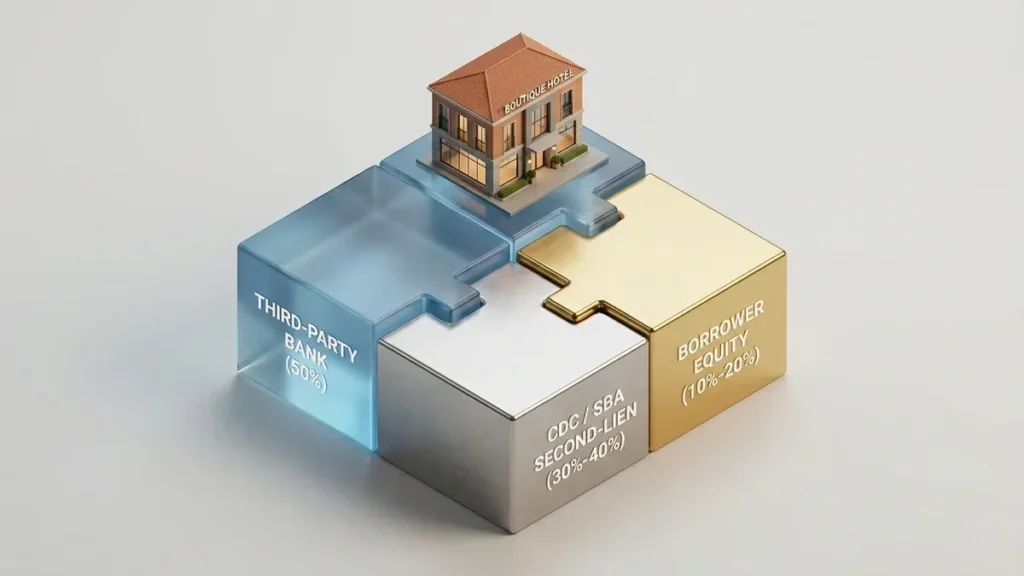

If you are building a hotel from the ground up, the SBA 504 loan is often a better fit. This program uses a unique structure in which a private bank covers 50%, a Certified Development Company covers 30% to 40%, and you only have to put down 10% to 20%. This low down payment keeps your hard-earned cash in your bank account where it belongs.

Tracking Boutique Hotel Construction Loan Rates and Market Dynamics

Building a brand-new hotel is an exciting adventure, but it is also the highest-risk project you can take on. Because your property is not yet making any money, lenders charge a premium to cover their risk.

That is why boutique hotel construction loan rates are usually higher than standard permanent mortgages. These rates typically float between 1.5% and 3.5% over the Prime index.

In today’s market, elevated construction costs and tight lending rules make these loans a bit harder to secure. Lenders will structure these as short-term loans that last 12 to 24 months.

You only pay interest during the construction phase, and the lender releases funds in stages as you hit key construction milestones. Once your hotel is built and guests start booking rooms, you can roll that short-term debt into a long-term, fixed-rate permanent mortgage.

Meeting Small Boutique Hotel Construction Loan Requirements

To secure financing for a smaller, intimate hotel, you must prove to the lender that you can bring the project across the finish line on time and under budget. Lenders are very careful about cost overruns.

First, you need a flawless feasibility study and a local market demand analysis. These documents prove to the lender that guests actually want to stay in your location.

Next, you must present a fixed-price contract with a licensed builder. This contract protects the project from sudden price spikes in building materials.

Lenders also want to see that you have a personal credit score of 680 or higher and a solid track record of running similar lodging properties. If you are new to the hotel business, you can often solve this requirement by hiring an experienced, third-party hotel management team.

Refinancing an Existing Boutique Hotel Loan: Restructuring and Optimization

The hotel industry is facing a massive wave of maturing debt over the next two years. If your current loan has a balloon payment coming up, now is the perfect time to look at refinancing an existing boutique hotel loan.

Refinancing allows you to escape high variable rates, pull out equity for upgrades, or push out your payoff date.

To qualify for a refinance, you must show a clean 12-month payment history with absolutely no late payments. Lenders will look at your property’s current value and income.

If you use government-backed programs like the USDA B&I loan to refinance, keep in mind that they do not allow cash-outs. Every dollar of the new loan must go toward paying off the old business debt, funding property upgrades, or buying out partners.

If you want to pull cash out for other business expenses, you can use the SBA 7(a) program to refinance up to 75% of your property’s appraised value.

Operational Execution: Boutique Hotel Renovation Financing Tips

Keeping your property looking fresh and modern is the only way to keep your room rates high. If your hotel looks dated, guests will leave bad online reviews, and your bookings will drop.

Whether you are updating an independent property or satisfying a franchise-mandated Property Improvement Plan (PIP), these boutique hotel renovation financing tips will help you budget smartly.

Focus your money on high-impact areas that matter most to guests. Focus on room designs, lobby upgrades, and fast, reliable Wi-Fi.

Asset Type

Average Renovation Cost Per Room

Focus Areas

Economy / Midscale

$3,500 to $7,000

New paint, basic furniture, LED lighting

Upscale / Select Service

$7,500 to $15,000

Redesigned lobbies, modern beds, tech updates

Luxury / Full Service

$16,000 to $35,000+

Custom woodwork, premium baths, smart controls

Always include a healthy debt service reserve in your renovation budget. Upgrading rooms means you will have to take them out of service, which temporarily lowers your booking income. A cash reserve ensures you can easily make your mortgage payments even when half your rooms are closed for painting.

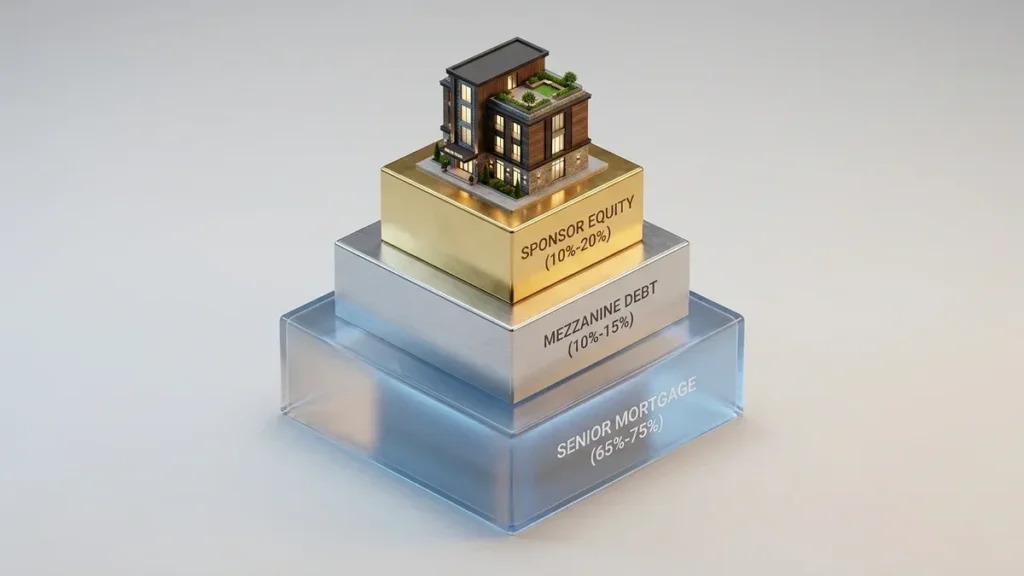

How to Structure Creative Financing Solutions for Unique Boutique Hotels?

Some of the most profitable hotels are highly unique, such as converted historic warehouses, vintage Airstream resorts, or luxury treehouses. These properties do not fit into the standard boxes that conservative local banks use.

To fund these wild concepts, you must use creative financing solutions for unique boutique hotels.

One smart option is “Jigsaw funding”. This is where you piece together multiple capital sources to cover your total costs.

You might secure a first-lien conventional bank mortgage for 50% of the deal, add a subordinate mezzanine loan for 15%, and bring in private equity partners to cover the rest. Mezzanine debt sits between your main mortgage and your equity, giving you extra cash without diluting your ownership.

You can also explore alternative options, such as crowdfunding or short-term merchant cash advances, to cover early startup costs.

Strategic Choice: Boutique Hotel Franchise vs Independent Financing

When you plan your project, you must make a major choice: do you want to build an independent hotel or a branded franchise? Lenders look at this decision very differently during underwriting.

Each path has distinct trade-offs that affect your rate, your terms, and your daily operating freedom.

Flagged Franchise Properties: Banks and CMBS lenders love recognized brands like Hilton or Marriott. Because these brands have massive global reservation systems and millions of loyal members, lenders view them as low-risk bets. This lower risk gets you lower interest rates and longer payoff terms. However, franchises come with heavy fees and rigid design rules.

Independent Boutique Properties: Independent hotels give you complete creative freedom. You can design the property exactly how you want, and you do not have to pay expensive franchise royalties. But because you lack a global brand to drive bookings, lenders view you as higher risk. They may charge higher rates, require a larger down payment, and closely examine your personal hospitality experience.

This strategic choice between a boutique hotel franchise and independent financing shapes your entire capital search. If you go independent, you must present a rock-solid local marketing plan to prove you can fill rooms without a major brand’s help.

The Expert Guide to Securing Financing for a Luxury Boutique Hotel

Luxury hotels are performing incredibly well right now. High-end travelers are willing to spend substantial sums on exclusive, low-density resorts with personalized service.

To fund these premium assets, our guide to securing financing for a luxury boutique hotel focuses on high-net-worth investors.

Because luxury projects require massive amounts of capital, traditional bank limits can sometimes block your progress. High-net-worth individuals, family offices, and private equity funds are highly active in this space.

They can provide the flexible equity you need to bridge the gap. To win over these investors, you must demonstrate a clear path to high average daily rates, strong food-and-beverage profits, and high-margin wellness packages.

Maximizing Leverage with Boutique Hotel Acquisition Financing Strategies

Buying a hotel that is already open and making money is much easier to fund than starting a brand-new build. Because the property has a historical track record of bookings, lenders can easily verify the cash flow.

To get the most out of your deal, you should use smart boutique hotel acquisition financing strategies.

One of the best strategies is layering different debt options to keep your out-of-pocket cash as low as possible. For example, you can use the SBA 7(a) program to cover up to 90% of the purchase price.

You can also use seller financing. This is where the current owner agrees to hold a second-position note for a portion of the down payment, lowering your upfront cash requirement. Keeping extra cash in your bank account is vital for handling seasonal booking drops during your first year of ownership.

Can You Secure Government Grants for Boutique Hotels?

Many investors search for free money to build their lodging businesses. While direct government grants for boutique hotels are almost impossible to find, you can access highly subsidized government loan programs that offer similar benefits.

The absolute best government-backed program for rural properties is the USDA Business & Industry (B&I) Guaranteed Loan Program.

The USDA B&I program is designed to create jobs in rural areas, defined as any town or city with a population under 50,000. This program offers loans up to $25 million with repayment terms stretching out to 30 years.

Unlike SBA loans, the USDA program allows for passive investment. This means you do not have to run the hotel yourself; you can hire a management team to handle daily operations. The USDA backs up to 80% of the loan, allowing lenders to offer highly competitive interest rates tied to the Prime index.

Weighing the Pros and Cons of Boutique Hotel Debt Financing

Using debt to fund your hotel is a powerful way to scale your portfolio. But before you sign a personal guarantee, you must weigh the pros and cons of boutique hotel debt financing.

The Pros: The biggest benefit is ownership retention. Lenders only earn interest; they do not get a say in how you design your lobby, and they do not take a share of your monthly booking profits. Also, the interest payments on your business mortgage are usually tax-deductible, which lowers your net taxable income.

The Cons: Debt is rigid. You must make your monthly mortgage payments on time, whether it is your busy summer season or a slow winter month. If your bookings fall and you miss payments, the lender can foreclose on the property and seize your assets. Many commercial hotel loans also require personal guarantees, which puts your personal wealth and home at risk.

Partnering with HotelLoans.Net for Hospitality Success

Navigating the commercial debt market is incredibly complex, but you do not have to do it alone. HotelLoans.Net is a premier financial consulting and advisory firm that specializes exclusively in hospitality real estate investment properties.

They have 30 years of deep underwriting experience. They act as a correspondent and table lender, and they sometimes serve as a “super broker” to bring private capital to your deal.

HotelLoans.Net does not manage your hotel operations or help run your daily hospitality business. Instead, they focus entirely on what they do best: structuring and securing the perfect financing package for your real estate.

Through their vast, exclusive network of private lenders and institutional investors, they offer access to 75 different loan options.

They offer both exclusive and non-exclusive referral programs for hospitality real estate brokers, helping both experienced professionals and newcomers close deals faster.

They also provide expert financial advice and consulting for investors across the entire hospitality spectrum. Whether you are buying land, launching ground-up construction, or executing a fix-and-flip, fix-and-hold, or fix-and-rent strategy, they can help you structure your debt.

Their funding expertise covers a wide range of property types, including:

Hotels and boutique resorts

Motels and classic roadside lodgings

Restaurants and bars

Recreation centers and entertainment spots

Vacation rentals and luxury cabins

To ensure you get the absolute best terms, HotelLoans.Net assists with a massive menu of specialized loan products, including:

Bridge Loans & Hard Money: Fast, short-term cash to seize time-sensitive opportunities.

DSCR & Term Loans: Traditional, long-term financing based on property income.

SBA 7(a) & 504 Programs: High-leverage, government-backed small business financing.

USDA B&I Rural Debt: Large-scale funding up to $25 million for rural lodging properties.

No-Doc & Lite-Doc Loans: Quick funding with minimal standard tax paperwork.

Construction-to-Permanent: Seamless loans that cover both building and long-term stabilization.

Navigating Boutique Hotel Financing for Long-Term Cash Flow

Mastering boutique hotel financing is the ultimate key to unlocking long-term cash flow and building lasting wealth in the hospitality sector. The lodging market is growing rapidly, and travelers are actively seeking unique, experiential properties. By matching your creative vision with a smart, highly optimized capital stack, you can build a highly profitable asset that thrives in any economic climate.

Do not let your dream property sit on the sidelines while other investors cash in. Reach out to the hospitality funding experts at HotelLoans.Net today to review your 75 loan options and structure the perfect financing package for your next project.

FAQs

Do USDA loans fund hotels with casinos?

No, USDA loans do not fund properties with casinos. The program strictly excludes hotels featuring golf courses, gambling facilities, or racetracks. Your boutique property must also sit in a qualified rural area to receive these funds.

Can SBA 504 loans pay for marketing?

No, you cannot use these funds for marketing. SBA 504 loans strictly restrict the use of proceeds. They only cover hard assets like real estate, land, and heavy equipment, completely blocking use for advertising or working capital.

Does USDA hotel lending require US citizenship?

Yes, US citizenship is a strict rule. The program requires that US citizens or permanent residents own at least 51% of the borrowing entity. Make sure your ownership structure meets this threshold before submitting your loan file.

Can passive investors get SBA hotel loans?

No, passive investors do not qualify. SBA rules require you to actively run and manage your boutique hotel as an owner-operator. If you want a completely hands-off investment, you must target USDA loans or private capital instead.

Are unsecured hotel business loans actually available?

Yes, you can secure unsecured options. These working capital loans or merchant cash advances rely entirely on your hotel’s daily revenue and credit history. Lenders do not require physical collateral, allowing you to access fast funding within days.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.