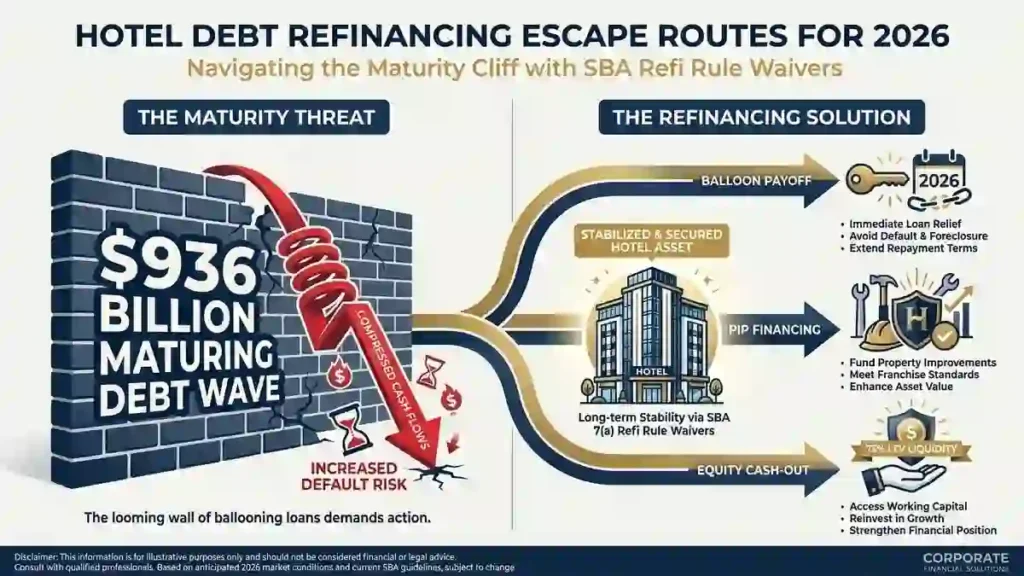

A massive $936 billion wave of commercial real estate debt matures in 2026. Right now, smart hotel owners are quietly locking up the best remaining lending partners. If you wait too long to secure your capital, you will face much higher rates and strict terms. The margin for error has disappeared. If you want to acquire, build, or refinance, you must find the right franchise hotel financing lenders today.

We do not run hotel operations. We focus strictly on real estate investment property. Our team brings 30 years of underwriting experience to your transaction. We act as a correspondent lender, table lender, and super broker. We offer 75 different loan options through our deep private lender network. We are here to guide you through the complex world of hotel debt.

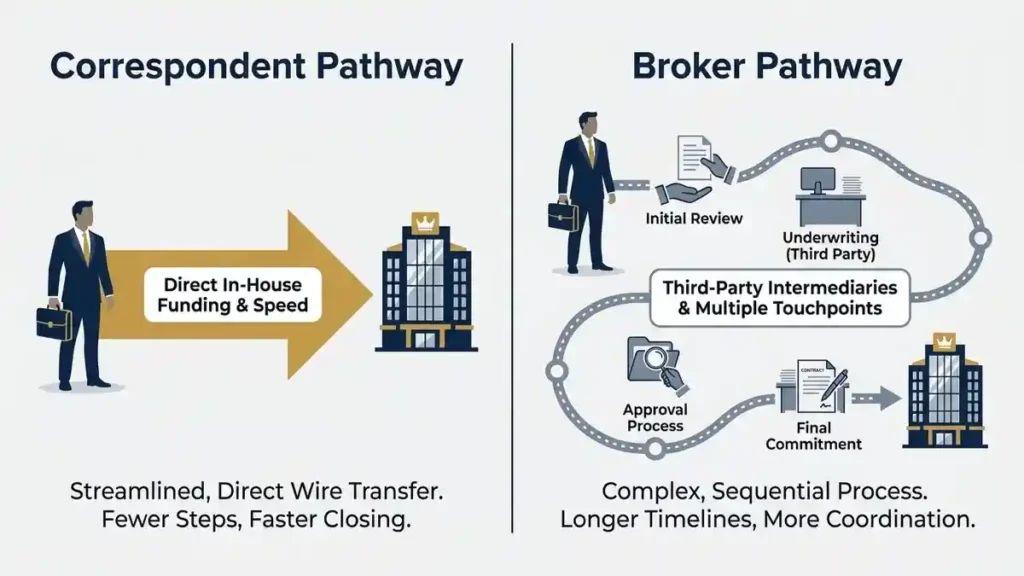

Correspondent Lenders, Table Lenders, and Brokers: Who Actually Funds Your Deal?

Understanding how your lender funds your loan is vital. It changes your closing speed and your overall terms.

A correspondent lender originates, underwrites, and funds the loan in their own name. They use a warehouse line of credit. They sell the closed loan on the secondary market to larger investors. They handle underwriting in-house. This gives you fast closings and clear communication.

A table lender closes the loan in their name. However, a wholesale investor provides the cash at the closing table. They act as the funding source.

A pure mortgage broker connects you with a wholesale lender. They do not fund the loan themselves. They cannot waive underwriting guidelines.

HotelLoans.Net acts as a correspondent and table lender. We also serve as a super broker. This dual capability gives you unmatched speed and 75 different loan structures.

Operational Attribute

Correspondent

Table Lender

Super Broker

Mortgage Broker

Funding Source

Warehouse line

Wholesale cash

Private networks

Third-party cash

Underwriting

In-house

Sponsor-driven

Combined expertise

Zero control

Name on Docs

Lender’s name

Lender’s name

Flexible

Wholesale lender

Loan Variety

Limited options

Limited options

75 options

Varies

Closing Speed

Very fast

Fast

Rapid execution

Slower

What Are the Real Challenges in Securing Hotel Franchise Loans Today?

The hospitality market faces severe headwinds. Many borrowers struggle with the unique hurdles of this sector. Identifying the major challenges in securing hotel franchise loans will help you prepare.

A $48 billion wave of hospitality CMBS debt matures during the 2025 to 2026 cycle. Much of this debt was written when rates were between 3.0% and 4.5%. Today, borrowers face interest rates of 6.25% to 7.0% or more. This rate spike increases annual carrying costs by 40%.

Rising rates compress debt service coverage ratios (DSCR). Lenders have widened mortgage spreads to 375 basis points over Treasuries. This is much higher than the spreads for multifamily or industrial real estate.

At the same time, operating margins are under pressure. Wage and insurance costs continue to rise. The average labor cost per occupied room has climbed to $48.32.

Strict brand mandates present another major hurdle. Major hotel brands enforce regular Property Improvement Plans (PIPs). These PIPs require deep upgrades. A typical PIP costs between $2 million and $8 million per asset. Lenders view unpaid PIP costs as high risks.

Your Guide to Hotel Franchise Financing Options

You must match your property type with the right loan program. This guide to hotel franchise financing options breaks down the core lending vehicles.

Loan Type

Target Property

Max LTV (up to)

Term

Key Benefit

SBA 7(a)

Limited-service

90%

25 Years

Includes working capital

SBA 504

Ground-up, large assets

85%

25 Years

Long-term fixed rate

CMBS

Stabilized hotels

65%

5-10 Years

Non-recourse structure

USDA B&I

Rural markets

80%

30 Years

High leverage, long term

Bridge

Value-add, PIP assets

75%

1-3 Years

Speed and flexibility

SBA loans offer great benefits for owner-operated hotels. CMBS loans provide non-recourse terms for large, stabilized properties. Bridge loans provide fast cash to fund renovations before you transition to permanent debt.

Who Are the Best Lenders for Hotel Franchise Financing?

Top-tier SBA lenders prioritize experienced owner-operators. They look for clean personal credit and an active management history. CMBS lenders focus strictly on actual property performance and trailing cash flows.

Specialized lending networks streamline this process. Digital marketplaces connect hotel owners with over 150 specialized lenders. They maintain direct partnerships with brands like Hilton, Wyndham, and Choice Hotels. This connectivity helps developers find pre-approved lenders, speeding up closing times.

How to Get a Hotel Loan and Lock in Your Asset

Understanding how to get a hotel loan requires a step-by-step strategy. Hotels do not have long-term tenant leases. Lenders instead evaluate daily room revenue and brand strength.

First, choose your target property and service level. Analyze the local market to understand supply and demand dynamics.

Second, check the property’s key performance metrics. You must study the Average Daily Rate (ADR) and occupancy trends. The most critical metric is the Revenue Per Available Room (RevPAR) index.

An index of 100 means the hotel performs at the same level as its competitors. An index above 100 shows excellent pricing power. Lenders offer rate discounts of 50 to 75 basis points for high-performing assets.

Third, structure your application package. Work with a correspondent lender to match your deal with the best loan program.

How to Get a Loan for a Franchise Hotel: Step by Step

Getting a loan for a franchise hotel requires meeting strict operational requirements. Government-guaranteed programs are the most accessible option for owner-operators.

First, the borrowing entity must actively operate the hotel. Passive real estate holding structures do not qualify for SBA guarantees.

Second, you must meet the small-business size standards. Your business must operate for profit within the United States.

Third, you must prove your management capability. Lenders vet your history with major hotel brands. If you lack direct hotel experience, you must hire an experienced General Manager. You can also sign a management agreement with an approved third-party operating company.

Fourth, you must inject sufficient cash equity. Franchise properties typically require a 15% to 20% down payment.

Inside the Underwriting Box: What Are the Requirements for Franchise Hotel Loans?

The underwriting process for hospitality real estate is highly detailed. Lenders look closely at the physical property and the sponsor’s overall business health. Meet these major requirements for franchise hotel loans to secure approval:

Global Cash Flow Coverage: Lenders combine the cash flow and liabilities of your entire portfolio. They require a Global Debt Service Coverage Ratio (Global DSCR) of 1.25x or higher.

Post-Closing Liquidity: You must maintain a cash cushion after closing. Lenders prefer to see 10% of the loan amount or 12 months of mortgage payments in verified liquid assets.

Credit Score Minimums: Most lenders require a personal FICO score of 680 or higher. Some accept scores as low as 640 if the hotel has strong cash flow and reserves.

Stabilized Occupancy Floor: Lenders assume a stabilized occupancy floor of 60%-65%. This ensures the hotel can cover its daily operating expenses.

Can You Leverage Small Hotel Loans for Select-Service Properties?

The select-service sector represents a stable segment of the lodging market. Many regional banks and SBA lenders offer small hotel loans of up to $5 million for these assets.

Select-service brands like Fairfield Inn, Hampton Inn, and Holiday Inn Express maintain excellent operating efficiencies. They generate strong house profit margins of 35% to 45%.

These properties do not have complex food-and-beverage programs. This limits their exposure to wage inflation. Lenders offer higher leverage on these assets. SBA 504 structures allow up to 85% LTV, far exceeding conventional limits.

What Documents Do I Need for a Franchise Hotel Loan?

A complete application package prevents delays in closing. You must gather specific files to answer the question, “What documents do I need for a franchise hotel loan?”

Document Group

Specific Records Required

Why Lenders Want It

Sponsor Files

Three years of tax returns, PFS, and detailed hospitality resume

Confirms net worth, liquidity, and experience

Hotel Performance

Trailing-12 P&L statements and active balance sheets

Calculates the property NOI and actual DSCR

Market Metrics

STAR reports from Smith Travel Research

Measures the hotel occupancy and RevPAR index

Franchise Details

Approved franchise agreement and brand comfort letter

Confirms brand safety and details the required PIP

Third-Party Reports

Real estate appraisals and Phase I environmental reviews

Verifies property valuation and environmental safety

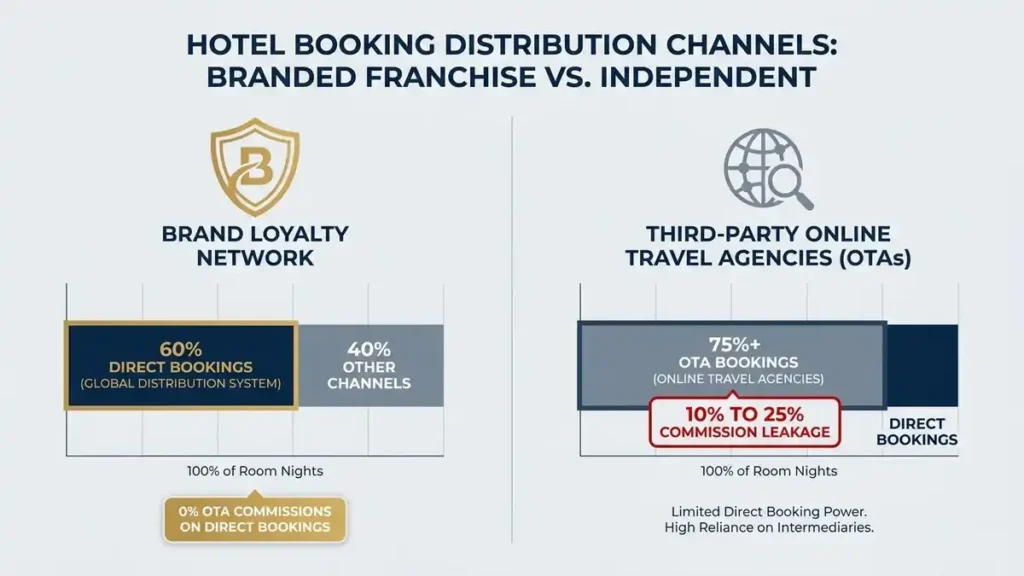

Why Are Franchise Hotel Financing Lenders So Strict About Specific Brands?

Flag systems reduce cash flow volatility. Strong brands drive customer loyalty. Their distribution networks account for up to 60% of room nights. This pricing power gives flagged properties a massive advantage over independent hotels.

How to Find Preferred Lenders for Hilton Franchise Hotels

Hilton flags like Hampton Inn and Curio Collection are highly favored by commercial underwriters. Hilton’s corporate finance programs maintain direct relationships with preferred lending networks.

You can easily locate preferred lenders for Hilton franchise hotels through specialized platforms. These lenders understand Hilton’s brand standards. This expertise helps them expedite pre-qualification and offer up to 75% LTV leverage.

What You Must Know Before Financing Marriott Franchise Hotels

Marriott International enforces strict property standards. Doing business with this brand requires careful planning.

When financing Marriott franchise hotels, you must plan for regular renovation costs. Select-service renovations cost up to $25,000 per key. Full-service upgrades can reach $60,000 per key.

Lenders mitigate this risk by requiring a mandatory monthly Furniture, Fixtures, and Equipment (FF&E) reserve deposit. This deposit typically equals 4% to 5% of gross revenues. The funds are held in a lender-controlled escrow account to pay for future upgrades.

Building and Improving: Capitalizing Your Projects

What Are the Underwriting Rules for New Construction Hotel Franchise Financing?

Ground-up development is highly complex. Underwriters require extensive documentation. You must present market feasibility studies, zoning approvals, and fixed-price construction contracts.

Securing financing for new-construction hotel franchises requires substantial equity. Conventional banks cap their leverage at 60%-65% LTC. Private debt funds offer up to 75% LTC, but their interest rates can reach 12.5%.

Lenders assume a 3-year stabilization period for new builds. Industry data shows that the average U.S. hotel takes 3.08 years to stabilize. Only 61.9% of properties achieve stabilization within this timeframe.

How to Secure Renovation Loans for Existing Hotel Franchises

Existing hotels must renovate regularly to protect their brand flags. Sponsors use bridge loans to execute brand PIP schedules.

These renovation loans for existing hotel franchises feature short-term, interest-only structures. The rates are floating and pegged to SOFR.

The bridge structure allows you to draw renovation cash directly from an escrow account. Once the PIP is complete and the hotel shows 90 days of improved operating history, you can refinance into permanent debt.

Breaking In: Hotel Franchise Financing for First-Time Owners

First-time operators often struggle to get bank approval without direct management experience. Standard lenders routinely decline applicants who lack a track record in hospitality.

Securing hotel franchise financing for first-time owners requires creative capitalization. The SBA 7(a) program provides a viable path by offering government guarantees to reduce lender risk.

First-time buyers can also utilize Rollovers as Business Startups (ROBS). This structure lets you roll retirement funds into your down payment without paying tax penalties.

Standby seller financing provides another source of equity. The SBA allows seller debt to count for up to 50% of your down payment. The seller’s note must remain in complete standby status, with no payments made, for at least two years.

HotelLoans.Net supports first-time owners by offering comprehensive financial consulting. We guide you through structuring your acquisition and selecting the best program from our 75 available options.

How to Compare Franchise Hotel Financing Rates and Costs

Comparing terms requires looking at both rates and fee structures. Interest rates vary widely across different debt programs.

Program Type

Typical Rate Range

Max Leverage (LTV/LTC)

Upfront Fee Structure

CMBS Limited-Service

5.85% – 6.85%

65% – 70% LTV

Conduit pricing spreads

CMBS Full-Service

6.50% – 7.50%

60% – 65% LTV

Legal and underwriting fees

SBA 504 (CDC)

5.50% – 6.50%

Up to 85% LTV

CDC packaging fees

SBA 7(a)

9.50% – 11.75%

Up to 90% LTV

3.5% – 3.75% guarantee fee

Hospitality Bridge

8.50% – 10.80%

Up to 75% LTV

1% – 3% origination fee

Hotel Construction

7.50% – 9.50%

60% – 75% LTC

Draw inspection fees

You must compare franchise hotel financing rates along with alternative funding tools. Commercial Property Assessed Clean Energy (C-PACE) financing can lower your blended cost of capital.

C-PACE is a property tax assessment program. It funds energy-efficient upgrades over 30 years. Stacking C-PACE with a USDA B&I loan can reduce your blended rate to 6.0%. This is much cheaper than single-source private debt.

Smart Refinancing Hotel Debt Strategies to Beat the Clock

Refinancing maturing debt before the balloon cliff is critical. Waiting until your loan expires reduces your leverage and leaves you vulnerable.

A key tool in your refinancing hotel debt strategies is the SBA’s updated refinancing rule. The SBA has waived its traditional 10% payment reduction rule for several high-priority situations:

Balloon Payment Mitigation: If your existing conventional debt has a balloon maturity within the next 12 months.

The PIP/Expansion Exception: If your refinance includes capital to fund a brand-mandated PIP or expansion.

Government Refinancing: If you are refinancing an existing SBA or USDA loan into a new SBA loan.

The SBA 504 program also allows rate and term refinancing up to 90% LTV. You can also secure cash-out refinancing up to 75% LTV to fund eligible business expenses, such as payroll and utilities.

Correspondent lenders like HotelLoans.Net use private credit networks to bypass restrictive bank balance sheets. We structure refinancing solutions that resolve maturity issues, fund outstanding PIPs, and stabilize property-level cash flows.

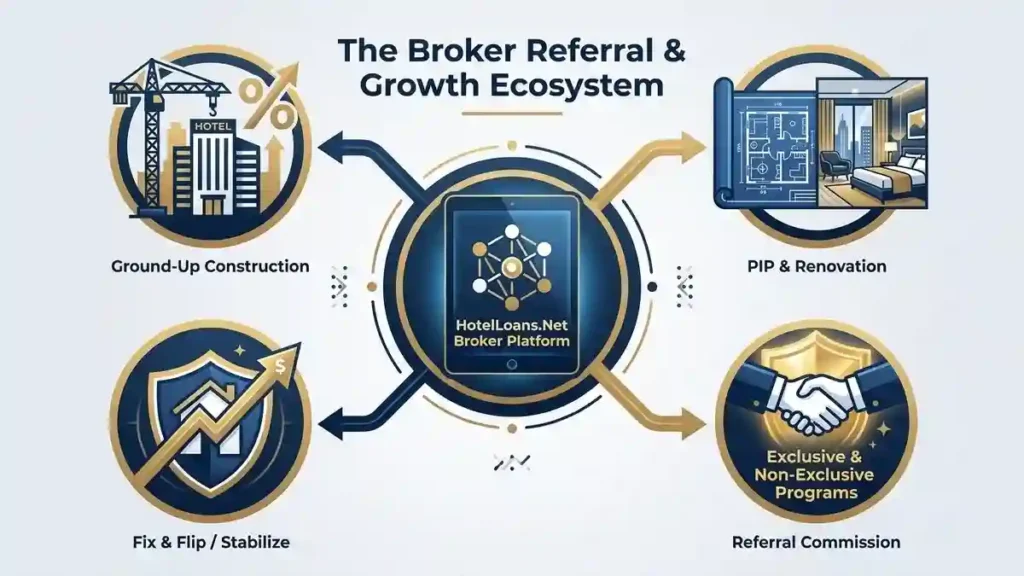

Smart Advice for Hospitality Real Estate Brokers

The commercial hospitality market is highly specialized. Real estate brokers can unlock massive transaction volumes by partnering with experienced lenders.

HotelLoans.Net offers both exclusive and non-exclusive referral programs for hospitality real estate brokers. Our programs support both experienced professionals and those new to the sector.

By partnering with us, you gain access to 30 years of underwriting experience and 75 distinct loan options. You can confidently assist your clients across multiple project types :

Land Purchases and Ground-Up Construction: Guiding developers through feasibility studies and construction-to-permanent financing.

Value-Add and PIP Renovations: Structuring bridge-to-permanent capital stacks to fund brand-mandated upgrades.

Fix-and-Flip, Fix-and-Hold, and Fix-and-Rent: Structuring short-term bridge debt to acquire, renovate, and stabilize underperforming assets.

Broad Asset Support: Advising clients on motels, restaurants, recreation centers, and vacation properties.

Brokers who transition to a correspondent alignment can close deals in their own name. This structure lets you earn undisclosed premiums on originations and advertise directly as a commercial mortgage lender. It is an excellent path to scaling your firm’s revenue.

Securing your next property requires swift, calculated action. The massive wave of maturities is shrinking the pool of available capital. Partnering with the right franchise hotel financing lenders ensures your project gets funded on time and with the best terms. HotelLoans.Net brings 30 years of underwriting expertise and 75 custom loan programs directly to your deal. Contact us today to secure your capital.

FAQs

Can FHA loans fund standard hotel properties?

No. FHA commercial programs do not cover standard hotels. They only insure residential properties with five or more units, like apartment buildings, and healthcare facilities. You cannot use them to buy or build a traditional hospitality asset.

Does SBA have guest stay length rules?

Yes. The SBA enforces the transient occupancy rule. Your hotel must generate more than half of its total revenue from guests who stay thirty days or less. Extended-stay properties with long-term tenants might not qualify for this program.

Can hotels with casino revenue get USDA loans?

Yes. You can get a USDA loan if your hotel has gambling. However, the property must derive less than fifteen percent of its annual gross revenue from gambling. Exceeding this limit will make your business ineligible.

Do new hotels require USDA feasibility studies?

Yes. The USDA requires an independent feasibility study for any B&I loan exceeding one million dollars for a new business. This study must analyze local demographics, labor markets, construction plans, and overall financial projections for the property.

Can you get ten million from SBA 7(a)?

No. The SBA 7a program caps its loans at $5 million. If your hospitality deal is larger, you must structure a pari passu loan using parallel bank and SBA notes to cover the remaining cash balance.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.