Right now, smart buyers are snapping up hotels across the United States. In fact, U.S. hotel sales recently surged to a massive $24 billion. Investors are racing to buy properties, and if you wait, you will miss out. You will let other investors buy the best properties in your city. To win this race, you must act fast before the best hotels are gone forever. But you cannot just buy any property. You need the right money behind you. Getting low hotel acquisition financing rates is the only way to protect your profits. If you pay too much for your loan, your cash flow dies.

This blog will show you how to get the best terms. We will look at what banks want. We will show you how to beat your competitors and lock in huge profits.

What Determines Your Hotel Acquisition Financing Rates?

The cost of your loan is the most important part of your deal. Lenders do not pick numbers out of a hat. They look at the national economy and your specific property.

How does the impact of Federal Reserve rates on hotel financing change your cash flow?

The Federal Reserve has a massive influence on your wallet. When the central bank changes its interest rates, your borrowing costs move immediately.

The impact of Federal Reserve rates on hotel financing dictates whether you pay a high premium or get a cheap loan.

Currently, the Fed is holding its main interest rate between 3.5% and 3.75%. This means rates are steady but still higher than they were a few years ago.

At the same time, inflation is hovering around 3.2%. As a result, the Wall Street Journal Prime Rate is 6.75%.

Lenders use these benchmark numbers to build your loan. If the Fed drops rates later, your borrowing costs will follow. If they raise them, your payments will jump.

What are the primary factors affecting hotel acquisition loan rates across different assets?

Lenders do not treat all hotels the same way. A big brand hotel in New York is very different from a small motel on a highway.

There are several factors affecting hotel acquisition loan rates that you must understand before you apply.

First, look at the property class. The hospitality market is currently split.

Luxury and high-end hotels are doing great. Their revenue per room grew by 3% recently.

On the other hand, budget and economy hotels are struggling. Their revenue fell by 4.4%.

Lenders see economy hotels as high-risk assets. Because of this, they will charge you a higher interest rate for a budget motel.

Second, look at the brand. If your hotel has a famous flag like Marriott or Hilton, banks feel safe. They will offer you lower rates. If your hotel is independent, banks will demand a bigger down payment and a higher rate.

Get the Best Terms by Comparing Lenders

You should never take the first loan option you see. You must shop around to find the best deal.

To get the cheapest money, you need to look at what different financial institutions offer. This is where comparing hotel acquisition loan rates from different lenders becomes vital to your success.

The table below shows what you can expect in today’s market:

For example, a standard bank loan might require a 30% down payment. But if you use an SBA loan, you might only need to put 10% down.

This helps you keep more cash in your pocket. These hotel-motel acquisition financing rates depend heavily on how safe the bank considers your deal to be.

How to Qualify for the Best Rates

Banks want to know you can repay them. They will look closely at your background and your numbers.

Do you meet the requirements to qualify for the best hotel acquisition rates?

To get the absolute lowest interest rate, you must prove you are a safe bet.

There are strict requirements for qualifying for the best hotel acquisition rates used by every major lender.

Your Net Worth: Lenders want your personal net worth to exceed the total loan amount. This shows you have financial strength.

Your Cash Reserves: You cannot spend every dollar you have on the down payment. Lenders want you to keep 10% to 20% of the loan amount in cash after you close. They call this post-closing liquidity.

Your Credit Score: You need a strong personal credit score. Lenders prefer a score of 680 or higher.

Your Experience: First-time buyers struggle to get good rates. Banks want to see that you have managed hotels successfully for at least 3 to 5 years.

The Debt Service Coverage Ratio (DSCR): This is a key metric. Your hotel’s net profit must be at least 1.25 to 1.40 times larger than your annual loan payments.

Fixed vs Variable Hotel Acquisition Loan Rates: Strategic Selection

You must decide how you want your interest rate to behave. This is a choice between fixed and variable rates for hotel acquisition loans.

A fixed rate stays the same for the life of your loan. It makes your monthly payments predictable. If interest rates rise in the future, you do not have to worry. Your payment is locked.

A variable rate changes over time. It usually tracks an index like the Prime Rate or SOFR.

Variable rates often start lower than fixed rates. But they are risky. If the Fed raises rates, your monthly payment will climb.

If you plan to hold the hotel for a long time, go with a fixed rate. If you plan to sell or refinance in two years, a variable rate might save you money.

The Hidden Value in Bricks-and-Mortar

Smart real estate players view hotels differently from average buyers. They see them as physical gold mines.

Academic studies from Harvard Business School show a major trend. Big hotel brands are selling their physical buildings.

For example, Accor sold 55% of its physical real estate arm for a massive $5.4 billion. Marriott currently owns or leases less than 1% of its actual hotel rooms.

These brands are moving to an “asset-light” model. They want to focus on franchises and booking technology.

But their exit creates a massive opportunity for you. You can buy the actual physical land and buildings.

The Economist points out that the stock market often fails to value hotel real estate correctly. For instance, the historic Ritz Hotel in London grew in value fourfold to $980 million. Yet, the public stock market barely noticed the appreciation.

When you buy physical hotels, you capture this hidden wealth.

Also, Harvard case studies on Centerbridge Partners show the power of CMBS debt. Centerbridge bought Great Wolf Resorts and used CMBS loans to secure long-term, non-recourse financing. This structure protected their other assets and let them expand rapidly. You can use the same corporate strategy to win.

7 Proven Strategies to Get a Lower Rate

You do not have to accept the first high rate a bank offers you. Use these seven physical strategies to force lenders to offer more favorable terms.

Strategy 1: Boost Your Cash Flow to Lower Your Risk

Lenders base their rates on risk. If your hotel has strong cash flow, you are a low-risk buyer.

This is the most powerful method for securing the best hotel acquisition financing rates.

You must prove your hotel will have a high Debt Service Coverage Ratio (DSCR). To calculate this, lenders use a simple mathematical formula:

To raise your Net Operating Income (NOI), you must manage your hotel efficiently.

Use dynamic pricing for your rooms. Do not keep your room rates static.

Change your rates daily based on local demand and seasons.

Also, cut unnecessary costs. Upgrade to energy-efficient lighting and smart thermostats. This directly lowers your utility bills.

Every dollar you save on utilities goes straight to your NOI. A higher NOI means a higher DSCR, which forces the bank to give you a lower interest rate.

Strategy 2: Prepare a Flawless Underwriting Book

Never walk into a bank empty-handed. You must negotiate with cold, hard facts.

Your path to negotiating lower rates on hotel acquisition loans starts with your underwriting package.

You need to gather these items before you talk to any lender:

Three years of certified profit and loss statements from the seller.

Your personal financial statement showing your net worth and cash reserves.

An official Smith Travel Research (STR) report. This report proves your hotel outperforms other local properties.

A detailed business plan that shows how you will increase guest bookings.

When a lender sees a professional package, they know you are an expert. They will compete for your business and offer you better terms.

Strategy 3: Target High-Demand Niche Locations

Location is everything in the lodging business. If you buy a hotel in a weak market, your interest rate will be high.

To get the lowest boutique hotel acquisition financing rates, you should buy in markets with insulated demand.

University-anchored towns are a prime example. Look at Paul McGowan, the founder of Study Hotels. He built a highly successful boutique brand by placing hotels next to Ivy League campuses.

He built “The Study at Yale” right in New Haven, Connecticut.

Also, the Cambria Hotel New Haven sits minutes from Yale University.

These university markets enjoy steady guest demand from professors, families, and sports fans. Lenders love these locations because they are recession-resistant.

Because the cash flow is so predictable, banks will offer you highly competitive rates.

Strategy 4: Partner with HotelLoans.Net

Getting a commercial loan is hard. Navigating the market on your own is a massive headache.

That is why you should partner with HotelLoans.Net.

They are a correspondent lender and a table lender. Sometimes they act as a super broker.

While they are not direct underwriters, they have 30 years of underwriting experience. They provide expert financial consulting services to people looking to buy hospitality and real estate properties.

They only help with real estate investment property. They cannot help you run your daily hotel business.

Because of their massive network of private lenders and investors, they offer 75 different loan options.

They can help you find the best current interest rates on hotel acquisition loans for your specific deal.

Whether you want to buy land, build a hotel, or execute a fix-and-flip, fix-and-hold, or fix-and-rent strategy, they have you covered.

They also offer exclusive and non-exclusive referral programs for hospitality real estate brokers.

Working with them is like having an army of finance experts in your corner. They do the shopping for you to find the lowest prices.

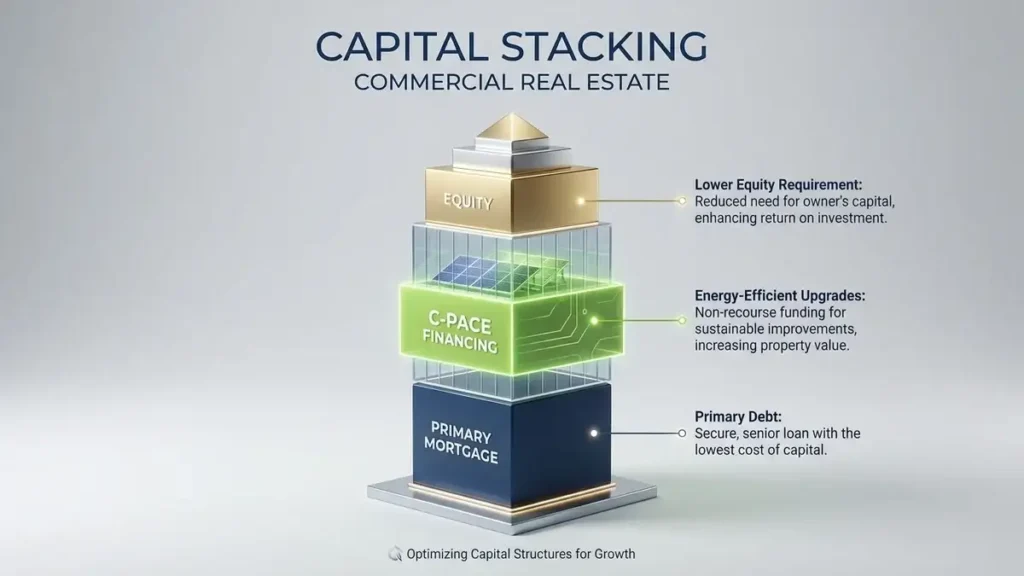

Strategy 5: Use C-PACE to Stack Your Capital

Commercial Property Assessed Clean Energy (C-PACE) is a brilliant way to access low-cost financing.

Research from the Saïd Business School at Oxford University shows that buildings account for 37% of global energy use. Because of this, green energy is a major focus for real estate investors.

C-PACE financing lets you borrow money for energy-saving upgrades. This includes new HVAC systems, solar panels, and water conservation tools.

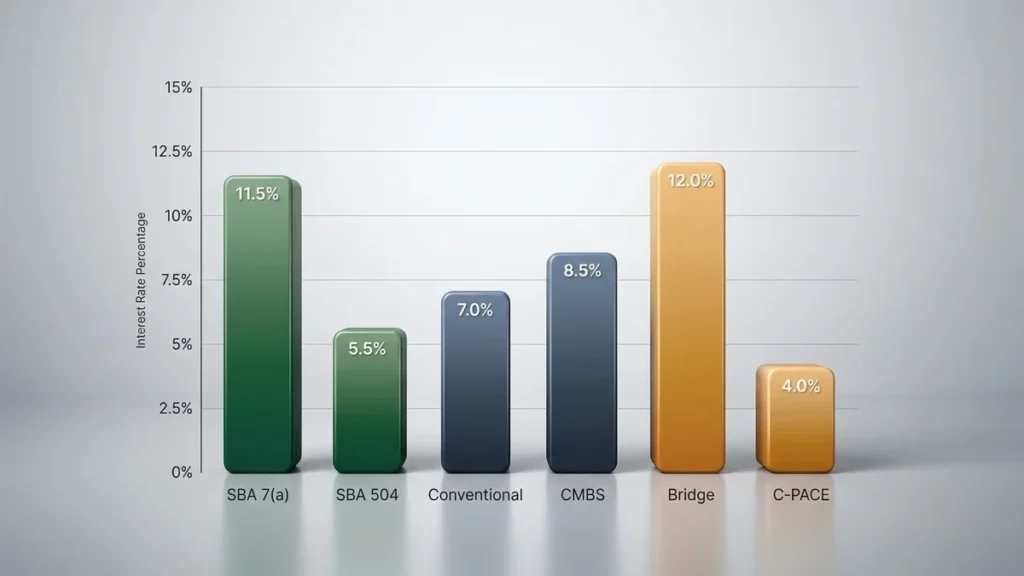

C-PACE rates are fixed and highly competitive, ranging from 5% to 7%.

On top of that, C-PACE is non-recourse. It attaches to the property, not to you personally.

By stacking C-PACE with your main bank mortgage, you reduce the amount of expensive high-rate equity you need to bring to the table.

Strategy 6: Keep a Large Safety Net of Cash

Banks hate surprises. They worry that a bad season or a sudden drop in travel will cause you to miss payments.

To ease their fears, you should keep plenty of cash in reserve after you close the deal.

Lenders look closely at your post-closing liquidity. If you show them that you have enough cash to cover six to twelve months of loan payments, they will feel safe.

This financial safety net proves you can survive a downturn. Because your risk of default is low, underwriters will reward you with a lower interest rate.

Independent hotels can be tough to finance. Lenders worry that independent properties lack the marketing power to attract guests.

You can instantly lower your interest rate by securing a franchise agreement with a major brand.

Flags like Hilton, Marriott, Holiday Inn, or Choice provide instant credibility.

These brands have global reservation systems and massive loyalty programs.

A branded hotel has highly predictable occupancy rates. Lenders love predictability.

When you present a signed franchise agreement during underwriting, banks will offer you much higher leverage and significantly lower rates.

Navigating Government Programs and Special Loans

If a conventional bank loan does not fit your deal, you have other excellent options.

How can SBA loan rates for hotel acquisition save you money?

SBA loans are the gold standard for buyers who want to preserve their cash. The government guarantees a portion of the loan, which makes banks highly comfortable.

The SBA 7(a) program is perfect for smaller properties and first-time buyers. It offers up to $5 million with repayment terms up to 25 years.

The interest rate is variable and floats at a set margin above the Prime Rate.

For larger, branded hotels, the SBA 504 program is a better match. It splits the financing into a bank loan and a fixed-rate CDC debenture.

The CDC portion locks in a low fixed rate for 25 years.

This program protects you from rising rates and keeps your monthly payments low.

Small Hotel Acquisition Financing Options and Rates

If you are buying a local motel or an independent bed-and-breakfast, you need targeted solutions.

There are specific financing options and rates for small hotel acquisitions designed for assets under $2 million.

Conventional banks offer small balance hospitality loans starting at $750,000. These loans carry amortization schedules up to 25 years.

But they usually require a personal guarantee.

To get a lower rate on a small hotel, you should ask the seller for owner financing. If the seller agrees to carry a second mortgage, you can reduce your bank loan size and secure a better interest rate.

A Complete Guide to Hotel Acquisition Bridge Loan Rates and Transitional Debt

Sometimes, a hotel is not ready for a long-term bank loan.

The property may need massive renovations, or the occupancy may be too low.

In these situations, you need transitional debt. This guide to hotel acquisition bridge loan rates will help you understand this fast-moving capital.

Bridge loans are short-term options that last 12 to 36 months.

Bridge loan rates typically range from 8.00% to 14.50%.

These loans are priced using a variable margin tied to SOFR.

While bridge money is more expensive than a standard bank loan, it closes incredibly fast—often in just two weeks.

You can use a bridge loan to quickly buy a property, complete your renovations, and then refinance into a cheap, long-term mortgage once the hotel is stabilized.

The 2026 Hospitality Market Outlook

The lodging market is entering a highly exciting phase.

Why does the hotel acquisition financing rates 2026 outlook favor prepared buyers?

The hotel acquisition financing rates 2026 outlook shows that liquidity is rushing back into the market.

A massive wave of maturing CMBS loans is forcing properties to trade hands. This means you will see many motivated sellers.

Also, base interest rates are stabilizing, making lenders highly active.

New hotel development is extremely low, with supply projected to grow by just 0.4%.

Because very few new hotels are being built, existing hotels are gaining significant pricing power.

Additionally, massive events like the 2026 FIFA World Cup will drive historic guest demand across the United States.

This combination of low supply, soaring demand, and stabilizing rates makes 2026 the perfect year to acquire a hotel.

Your Next Move to Secure Lower Hotel Acquisition Financing Rates

The wealth wave in hospitality is moving fast. If you sit back and hesitate, other buyers will take the best properties and the cheapest capital. To build a highly profitable portfolio, you must focus on your numbers today.

Optimize your hotel’s cash flow to boost your DSCR. Put together a flawless underwriting book with clean STR reports. Focus on strong locations with built-in demand and secure a well-known brand flag to reassure lenders.

You do not have to do this alone. Partner with the experts at HotelLoans.Net. With 30 years of underwriting experience and 75 different loan options, they will match you with the best lenders in the country. They will help you compare terms, structure your capital, and lock in the lowest hotel acquisition financing rates available on the market today.

Do not let this opportunity pass you by. Contact HotelLoans.Net today and secure your path to financial freedom.

FAQs

Is hotel loan interest tax-deductible?

Yes. You can usually deduct the interest you pay on your hotel loan from your business taxes. This lowers your overall taxable income. It saves you cold, hard cash. Always talk to your certified accountant to verify everything.

Can you finance franchise entry fees?

Yes. Many lenders let you roll the initial franchise fees right into your main acquisition loan. This keeps your upfront cost low. It helps you quickly open with a major brand. Ask your consultant how to structure this.

Are personal guarantees always required?

No. You do not always need a personal guarantee. Larger loans, such as CMBS or C-PACE financing, are non-recourse. This means the lender cannot take your personal assets if you default. They can only seize the physical hotel property itself.

Is hotel financing harder than other loans?

Yes. Lenders view hotels as riskier than standard buildings because room revenue varies daily. You do not have long-term tenant leases. Because of this, banks use much stricter rules to check your background and assets.

Do you need collateral for hotel loans?

Yes. You must pledge the hotel property as collateral to secure your loan. Lenders will put a lien on your land and building. If you stop making your payments, the bank can take the property to pay the debt.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.