Building a hotel takes more than just bricks and mortar. It takes a sharp financial mind and a clear map. Right now, the hospitality world is changing fast. The global market value is hitting $4.9 trillion. Experts think it will reach $7 trillion by 2029. This is a massive chance for developers. But you need to know how to fund your dream.

The market is facing a $48 billion “refinancing wall” this year. Many owners must find new money as their old loans come due. This makes the hotel construction loan more important than ever. If you want to build from the ground up, you need a partner who knows the ropes. We have 30 years of underwriting experience. We aren’t just a correspondent lender. We think like lenders.

Many people start with their local bank. That is a fine place to begin, but it often ends in a “no.” Local banks have limits. They might fear the hospitality sector. They see it as a high-risk gamble. This is where commercial hotel construction financing becomes a specialized field. You need to show you are a safe bet.

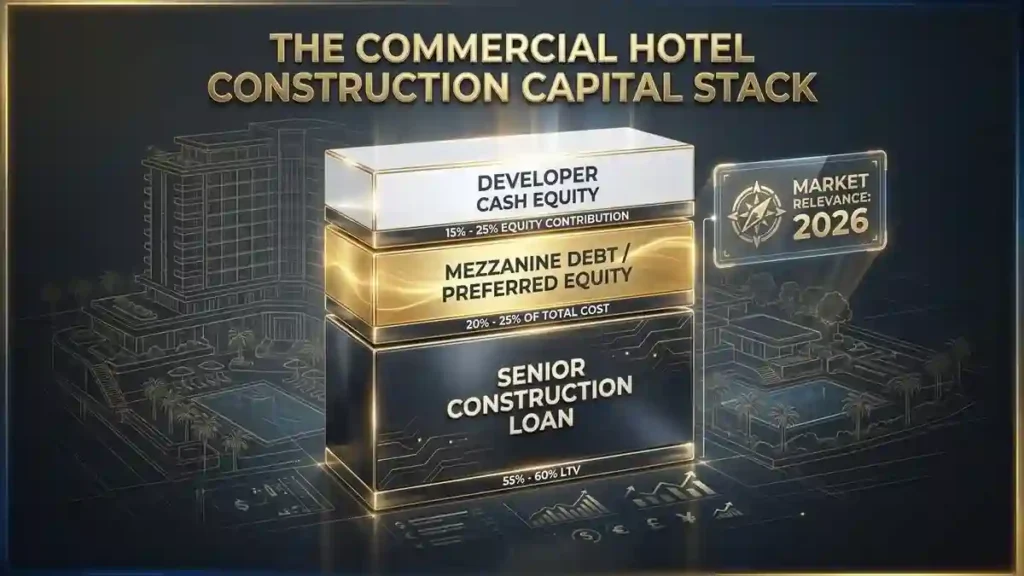

Lenders look at your “capital stack.” This is just a fancy way of saying where your money comes from. You might have your own cash. You might have a senior loan. You might even have a second, smaller loan called mezzanine debt. Most big banks like Wells Fargo are very active. They lead the pack with over $22.4 billion in construction loans. But they only want the best projects. If your plan is weak, they will pass.

The New Hotel Construction Loan Process

The new hotel construction loan process is a long road. It usually takes 60 to 120 days to close. You start with a big idea. Then you move to a formal inquiry. You have to prove the hotel will make money.

Lenders will ask for a feasibility study. This study looks at the local area. It asks: Are there enough travelers? Is there too much competition? You need to show that your hotel fills a gap. Maybe the town needs an extended-stay property. Maybe it needs a luxury boutique.

Once the lender likes the idea, the real work starts. You will need a fixed-price contract from a builder. This protects you and the lender from cost hikes. After you sign the papers, the money doesn’t come in one big check. The lender sends it in “draws”. You get money as you finish parts of the building. You finish the foundation, you get a draw. You finish the roof, you get another one.

Is Your Construction Budget Actually a Financial Time Bomb?

Costs can spiral out of control. The average cost to build a hotel room is about $323,500. If you have 100 rooms, that is over $32 million. You must have a “contingency fund.” This is extra money for when things go wrong. And things always go wrong in construction.

Lenders closely review hotel construction loan requirements. They want to see that you have enough cash to finish. If you run out of money at 80% completion, the loan is in trouble. That is why they often require an equity injection of 20% to 35%. They want you to have “skin in the game.” If you are using your own money, you are less likely to walk away.

How to Qualify for Hotel Construction Loan

You might wonder how to qualify for a hotel construction loan. It starts with you. Lenders look at your credit score first. Most want to see a score of at least 680. If your score is 720 or higher, you get the best deals.

They also look at your experience. Have you built a hotel before? If the answer is no, you should hire a team that has. Lenders love seeing a strong management team. They want to know the hotel will be run well once it opens. They also check your “Global DSCR.” This stands for Debt Service Coverage Ratio. They want to see that your total income is 1.25 times higher than your total debt. This creates a “cushion” for the bank.

Metric

Target Level

Credit Score

680+

Debt Service Coverage Ratio (DSCR)

1.25x

Equity Required

20% – 35%

Loan-to-Value (LTV)

65% – 75%

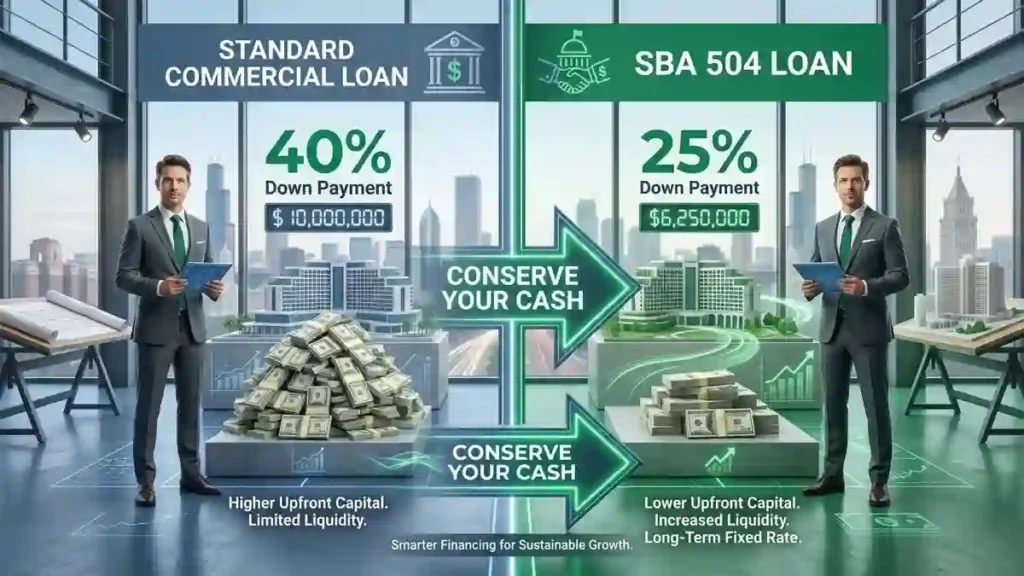

Can You Really Build a Hotel With Only 25% Down?

Yes, it is possible. This is where the SBA hotel construction loan comes in. The Small Business Administration has two main programs: the 7(a) and the 504. The 504 program is a favorite for new builds. It lets you put down as little as 25% or 35%.

The 504 loan structure is unique. A private bank covers 50% of the cost. A Certified Development Company (CDC) covers 35%. You cover the rest. This is great because the CDC portion has a fixed interest rate for 25 years. It gives you peace of mind. The 7(a) program is more flexible. It is good for smaller projects or buying furniture and equipment.

For a small hotel construction loan, these SBA options are life-savers. They help independent owners compete with the big brands. You don’t need a massive corporate balance sheet to build a great hotel. You just need a solid plan and the right government backing.

Searching for Hotel Construction Loan Lenders

Finding the right hotel construction loan lenders is a big task. Not all lenders are the same. Some only do big cities. Others like rural areas. Some only fund brands like Hilton or Marriott. Others will look at independent boutique hotels.

Life insurance companies are back in the game, too. Names like MetLife and New York Life are looking for high-quality deals. They usually want “debt yields” around 14%. This means they want the hotel to make a large profit relative to the loan amount. Debt funds and private lenders are also active. They can move faster than banks, but they might charge higher rates.

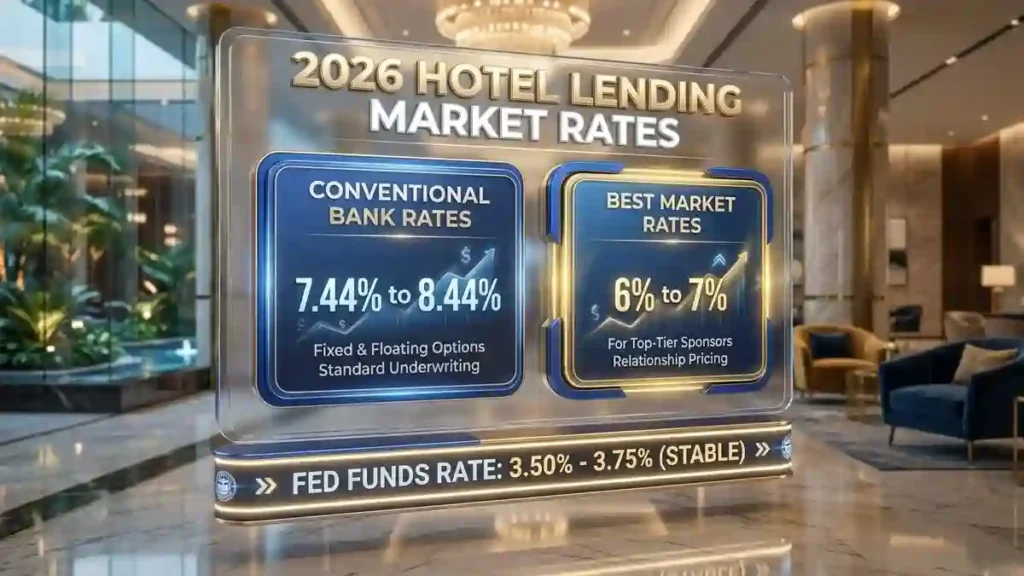

Everyone wants the best hotel construction loan rates. Right now, rates are stabilizing. The Federal Reserve has set a target range of 3.50% to 3.75%. Most construction loans will be 1% to 2% higher than a standard mortgage.

You can expect hotel construction loan interest rates today to be between 6% and 8% for strong borrowers. If your project is risky, the rate could go much higher. Average hotel construction loan terms usually last 1 to 3 years for the building phase. After that, the loan often converts into a “mini-perm” or a permanent mortgage.

Will Your Exit Strategy Fail Before You Even Break Ground?

A construction loan is a “short-term” tool. It is not a 30-year mortgage. You must have an “exit strategy.” This is your plan to pay off the construction loan. Usually, you do this by getting a permanent loan once the hotel is open and making money.

The difference between hotel construction loan and permanent loan is huge. Construction loans are interest-only. You only pay for the money you’ve used. Permanent loans are amortizing. This means you pay back the principal and the interest over 20 or 25 years. If you can’t get a permanent loan, you might get stuck with a high-interest construction loan. That is a recipe for disaster.

Boutique Hotel Construction Loan Options

If you want to build something unique, look into boutique hotel construction loan options. Travelers today want experiences. They are tired of “cookie-cutter” hotels. They want local flavor and great design.

Boutique hotels can be harder to fund because they don’t have a big brand name. Lenders see them as riskier. To win, you must show a powerful marketing plan. You need to prove you can reach guests through social media and booking sites. Mentioning names like Airbnb or unique travel apps can help. Lenders want to see that people are searching for your kind of hotel.

Hotel Renovation Loan vs Construction Loan

Sometimes, you don’t need to build from scratch. You might buy an old hotel and fix it up. In this case, you need to decide between a hotel renovation loan vs construction loan.

A renovation loan is often called a “PIP” loan. PIP stands for Property Improvement Plan. Most brands require you to do a PIP every few years. These loans are usually smaller and close faster. A full construction loan is for major work, such as adding a new wing or rebuilding from the foundation up. Renovation is often a safer bet for new investors because the building is already there.

Developer Hotel Construction Loan Tips

Here are a few developer hotel construction loan tips to keep in mind. First, be honest about your budget. Lenders will find the gaps. Second, get your permits early. Waiting for the city to approve your plans can kill a project. Third, stay in close contact with your lender. If there is a delay, tell them right away.

Also, watch the market trends. AHLA says guest spending will hit $805 billion in 2026. That is a 1.7% increase. More people are traveling, but they are also more careful with their money. Extended-stay hotels are doing great. They are growing at an 8.7% rate. These hotels are perfect for workers who need to stay for a few weeks. They have lower costs and higher profits.

The “experience economy” is the new value driver. People aren’t just paying for a bed. They are paying for a memory. This means your hotel should have great food, wellness areas, and “shareable” moments.

Harvard Business School research shows that “quality” is now measured by guest behavior. Do guests stay in the lobby? Do they use the gym? Yale School of Management studies highlight how local infrastructure helps hotels. If your hotel is near a university or a new tech hub, it is a much safer investment.

Strategic Advice for Brokers and Investors

If you are a broker, you need to know how to get hotel construction loan approval for your clients. You have to be a storyteller. You aren’t just selling a building. You are selling a vision of profit.

At HotelLoans.Net, we offer 75 different loan options. We help with everything from hard money to USDA B&I loans for rural areas. We help you navigate the “refinancing wall” and find the capital you need. Whether it is a “fix and flip” or a major resort, the right financing makes the difference.

Moving Toward the Finish Line

The hotel industry is resilient. It has survived big shifts before. Today, the focus is on efficiency and quality. If you can build a hotel that runs lean and makes guests happy, you will win.

Securing hotel construction loans is just the first step. It is the foundation of your success. With the right data and a strong partner, you can turn your blueprints into a thriving business. The world is ready to travel again. Is your hotel ready for them?

Key Statistics to Remember

Global Tourism Impact: 10.3% of global GDP comes from travel.

Tax Revenue: Hotels will generate $87 billion in taxes in 2026.

Jobs: The sector employs 371 million people worldwide.

Small Business: 59% of small businesses report being in “fair or poor” condition, so choose your lender wisely.

By following these steps, you can qualify for the money you need. You can build a property that stands the test of time. Don’t let the complex paperwork stop you. Use the tools available to you. Start planning your hotel construction loan today and get ready to break ground on a profitable future. We’ve been in this game for 30 years. We’ve seen markets rise and fall. The winners are always the ones who plan their financing before they pick up a hammer. Let’s get to work.

FAQs

Can I use land equity as a down payment?

Yes. If you already own the site, lenders often count its value toward your equity. You must provide a fresh appraisal to prove the worth. This strategy lets you keep more cash for the building phase.

Do these loans require a personal guarantee?

Yes. Most lenders want a full or partial guarantee from the owners. This means you are responsible if the project fails. It shows you believe in the deal. Lenders use this to reduce their risk on new builds.

Can I use retirement funds to secure a loan?

Yes. You can roll over a 401 (k) from a former employer into an SBA loan structure. This process is often tax-free and penalty-free. It is a great way to raise cash for a down payment without taking on new debt.

Will the loan cover my project soft costs?

Yes. These loans typically cover “soft costs” such as architectural plans, engineering, and permits. They also cover the “hard costs” of the actual building. You must list these items in your budget to ensure the lender approves the full amount.

Is an interest reserve included in the loan?

Yes. Lenders often add an interest reserve to the loan balance. This fund pays the monthly interest while you build. It helps you manage cash flow before the hotel opens. You won’t have to pay out of pocket.

Facebook Twitter Pinterest LinkedIn Right now, a massive 48 billion dollar wall of maturing hotel debt is crashing down on the hospitality industry. Think about

Facebook Twitter Pinterest LinkedIn approaching their final maturity dates. For hotel owners, that number is heavy. About 30% of hotel loans will come due in

Facebook Twitter Pinterest LinkedIn Did you know that nearly one-third of all hotel developers in the United States are halting their projects right now? A

Facebook Twitter Pinterest LinkedIn The dream was simple. You saw a market gap. You bought the land. You started the foundation. Then the world changed.

Ready to Discuss Your Hotel's Financial Strategy? Need a Commercial Loan?

Contact us today at Hotel Loans to initiate a conversation about how our financial expertise can contribute to the success of your hotel business. Our experienced team will be happy to help you.